How to Choose Construction Home Insurance

Building a new home is an exciting journey, but it comes with its share of risks. At Heaton Bennett Insurance, we understand the importance of protecting your investment during construction.

Construction home insurance is a specialized coverage designed to safeguard your property and assets throughout the building process. This blog post will guide you through the essential factors to consider when choosing the right insurance for your construction project.

What Is Construction Home Insurance?

Defining Construction Home Insurance

Construction home insurance is a specialized policy that protects your property during the building process. This type of insurance safeguards your investment from the ground up. It covers the structure, materials, and equipment on the construction site.

Duration of Coverage

The average time to build a single-family home is about 7 months, according to the National Association of Home Builders. This represents a significant period where your property faces various risks. Construction home insurance provides protection throughout this vulnerable phase.

Comprehensive Protection

Construction home insurance typically includes protection against fire, theft, vandalism, and weather-related damages. Some policies also offer liability coverage, which is essential if someone gets injured on your property during construction. The Insurance Information Institute reports that about 1 in 20 insured homes has a claim each year (highlighting the importance of comprehensive coverage).

Benefits for Stakeholders

For homeowners, this insurance provides peace of mind. You’re protected from potential financial losses due to unforeseen events during construction. For contractors, it demonstrates professionalism and can be a deciding factor for clients choosing between different builders.

Customizing Your Policy

Every construction project is unique, and your insurance policy should reflect that. Working with multiple carriers allows insurance professionals to find the best fit for your specific needs. Whether you’re building a small addition or a large custom home, a tailored policy can address the complexities of your construction project.

Standard homeowners insurance doesn’t typically cover homes under construction. This fact underscores the importance of having a specialized policy in place before breaking ground on your project. As you consider your options, it’s essential to understand the key factors that influence your coverage choices.

What Shapes Your Construction Insurance Needs?

Project Scope and Timeline

The size and complexity of your construction project directly affect your insurance needs. A small home addition requires less coverage than building a custom home from the ground up. The National Association of Home Builders reports that the average time to build a single-family home is about 7 months. Larger or more complex projects can take significantly longer, which increases exposure to risks and potentially requires extended coverage periods.

Location Impacts

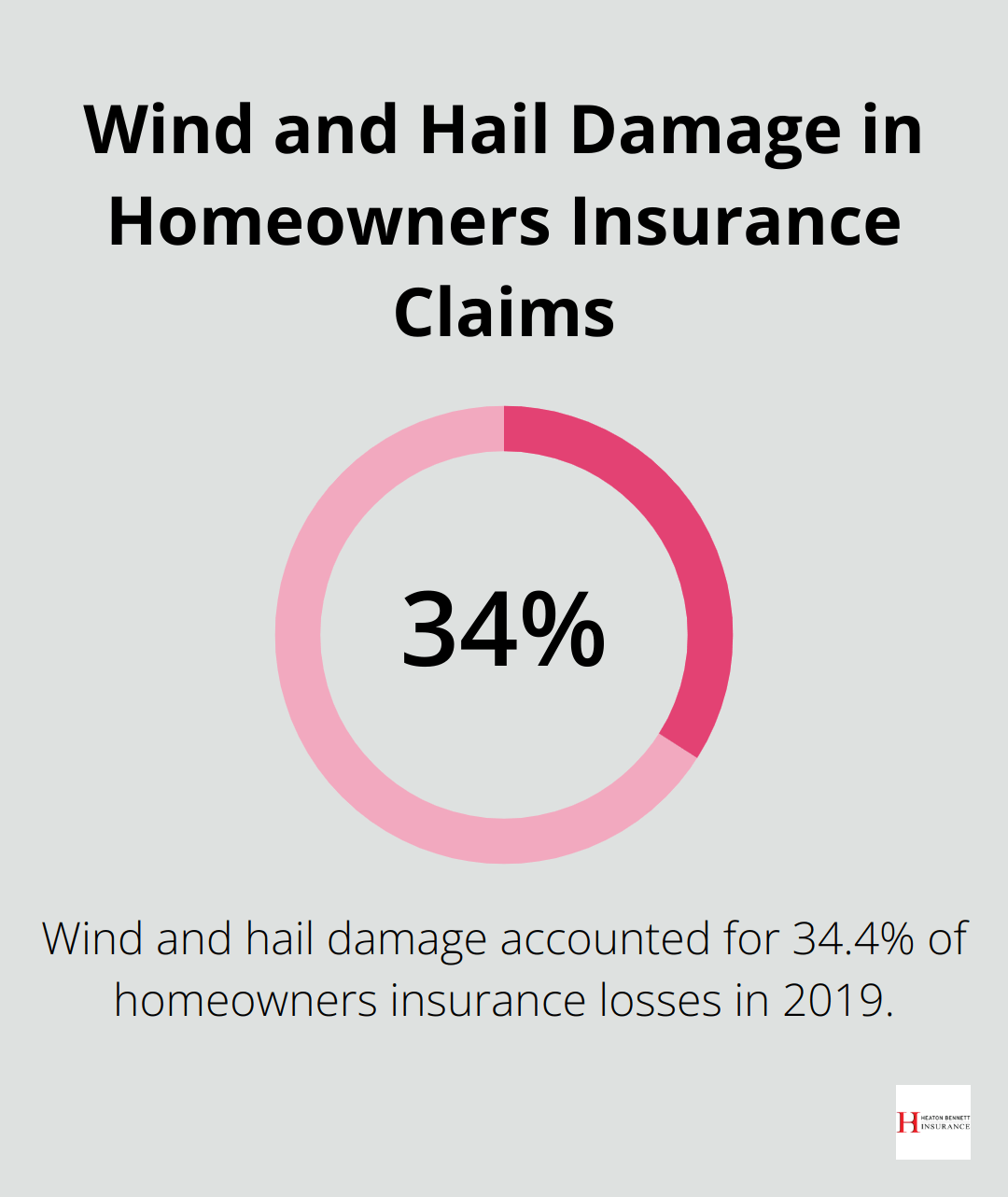

Your construction site’s location plays a crucial role in determining insurance needs. Different areas face varying environmental risks. For instance, coastal properties might need additional coverage for hurricane or flood damage. The Insurance Information Institute reports that wind and hail damage accounted for 34.4% of homeowners insurance losses in 2019 (highlighting the importance of considering regional weather patterns when choosing coverage).

Budget Considerations

It’s tempting to cut corners on insurance to save money, but this can lead to costly mistakes. The average property damage claim for homeowners insurance was $13,653 in 2019 (according to the Insurance Information Institute). This figure underscores the importance of adequate coverage, even if it means adjusting your budget. The cost of insurance is a fraction of potential out-of-pocket expenses if something goes wrong during construction.

Risk Assessment

Every construction project comes with unique risks. If your site is in a high-crime area, you might need more robust coverage for theft of materials or vandalism. Similarly, if you use specialized or expensive materials, your policy should reflect their value. A thorough risk assessment ensures your policy addresses all potential vulnerabilities specific to your project.

Regulatory Requirements

Local building codes and regulations can influence your insurance needs. Some jurisdictions require specific types or amounts of coverage for construction projects. It’s important to understand these requirements to avoid potential legal issues or project delays. Try to research local regulations or consult with a knowledgeable insurance professional to ensure compliance.

Understanding these factors will help you make informed decisions about your construction insurance. The next section will explore the essential coverage options you should consider for your project.

What Coverage Do You Need for Construction Insurance?

Construction insurance offers various coverage options. Let’s explore the essential policies you should consider for your construction project.

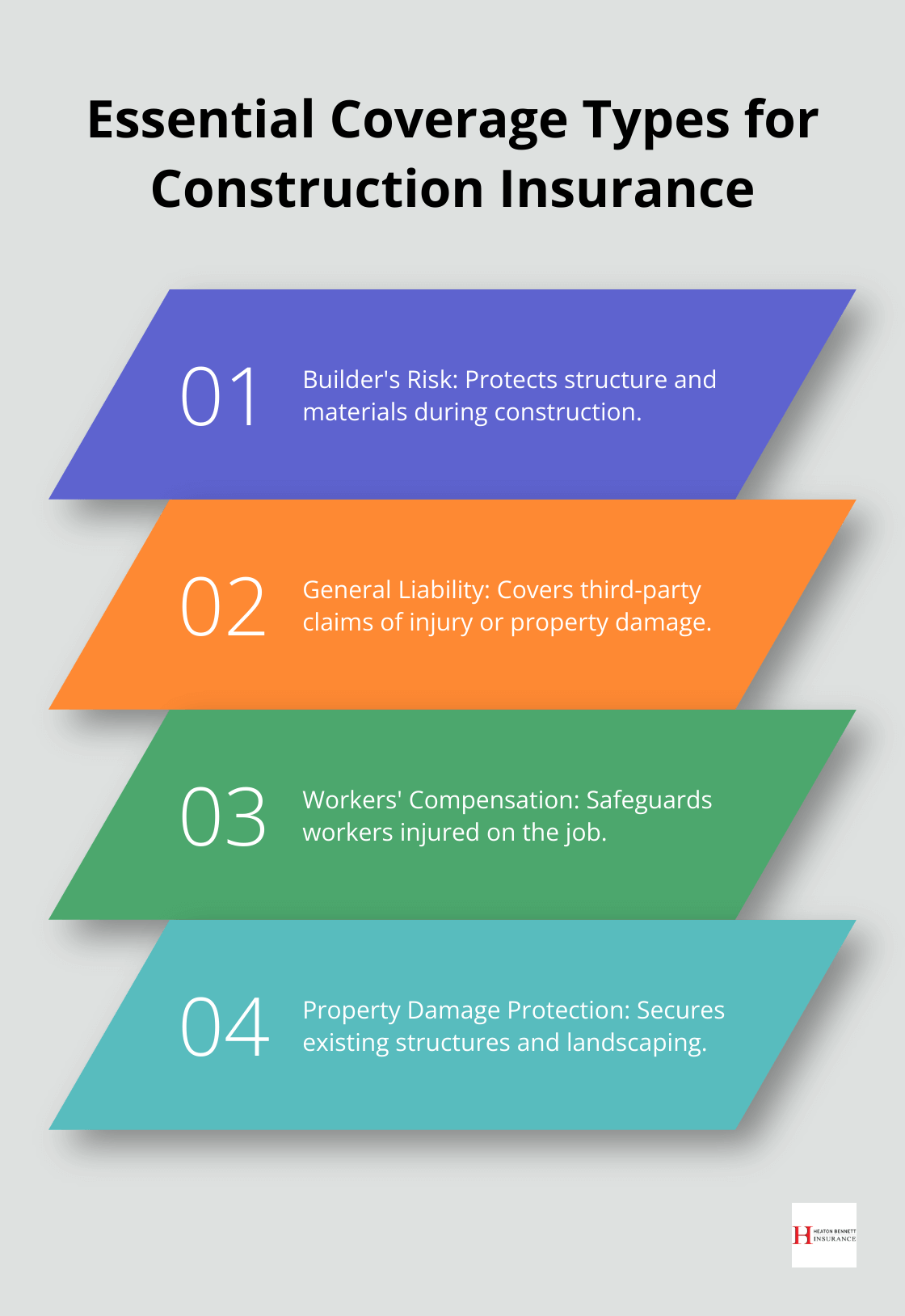

Builder’s Risk Insurance: The Foundation of Protection

Builder’s risk insurance protects the structure and materials during the building process. This policy can cover losses from fire, theft, vandalism, and weather events (potentially saving you thousands if disaster strikes). The Insurance Information Institute reports that the average property damage claim for homeowners was $13,653 in 2019.

When you select a builder’s risk policy, pay attention to the coverage limits and exclusions. Some policies might not cover certain natural disasters or theft of materials. You need to understand these details and adjust your coverage accordingly.

General Liability: Protection Against Third-Party Claims

General liability insurance protects you from third-party claims of bodily injury or property damage. If a visitor to your construction site trips and gets injured, this coverage can help with medical expenses and potential legal costs.

The Construction Industry Institute reports that construction-related injuries cost the industry billions annually. A robust general liability policy can protect you from bearing these costs out-of-pocket. When you choose coverage, consider the project’s size and location, as these factors can influence the likelihood and potential cost of claims.

Workers’ Compensation: Safeguarding Your Workforce

If you hire contractors or subcontractors, workers’ compensation insurance is essential. This coverage provides benefits to workers who are injured on the job, covering medical expenses and lost wages.

The National Safety Council reports that the average cost of a workplace injury in 2019 was $42,000. Workers’ compensation not only protects your workers but also shields you from potential lawsuits related to workplace injuries.

Property Damage Protection: Securing Your Investment

While builder’s risk covers the structure under construction, property damage protection extends to other aspects of your property. This can include existing structures, landscaping, and personal property stored on-site.

The National Association of Home Builders states that the average single-family home takes about 7 months to build. During this time, your property faces various risks. Comprehensive property damage protection ensures that all aspects of your investment are covered throughout the construction process.

Professional Guidance: Navigating Complex Choices

Construction insurance is complex. You should work with an experienced insurance professional who understands the nuances of construction insurance. They can guide you through this process and ensure you have the right mix of coverage for your specific project needs. High-risk industries like construction typically require more comprehensive coverage and may face higher premiums, making professional guidance even more valuable.

Final Thoughts

Choosing the right construction home insurance protects your investment during the building process. The risks associated with construction can lead to significant financial losses if not properly addressed. Understanding various coverage options and factors that influence your insurance needs will help you make informed decisions to safeguard your project.

Work closely with experienced insurance professionals to navigate the complex world of insurance policies. These experts provide valuable insights into specific risks associated with your project and help tailor your coverage to meet unique needs. They ensure you’re not over-insured or under-protected (a common pitfall for many property owners).

At Heaton Bennett Insurance, we offer comprehensive insurance solutions for construction projects. Our team of experts can guide you through selecting the right construction home insurance coverage. We provide access to multiple carriers, offering tailored policies that address the unique aspects of your project while providing competitive rates.