Weather Risk Insurance Texas: Protecting Your Bottom Line

Texas businesses face unpredictable weather that can devastate operations and finances. Hail, drought, and flooding hit different regions with varying intensity, leaving many companies scrambling to recover.

Weather risk insurance in Texas isn’t optional-it’s a business necessity. We at Heaton Bennett Insurance help you build protection that matches your actual exposure and keeps your bottom line intact.

Weather-Related Business Losses in Texas

Hail and Storm Damage Statistics

Texas businesses lost billions to severe weather between 2023 and 2025, with storms becoming more frequent and costly than ever. The state experienced several billion-dollar storm losses during this period, driving premiums up 10 to 40 percent in high-risk regions as insurers tightened underwriting standards. This isn’t speculation-it’s the reality shaping insurance markets across the state right now.

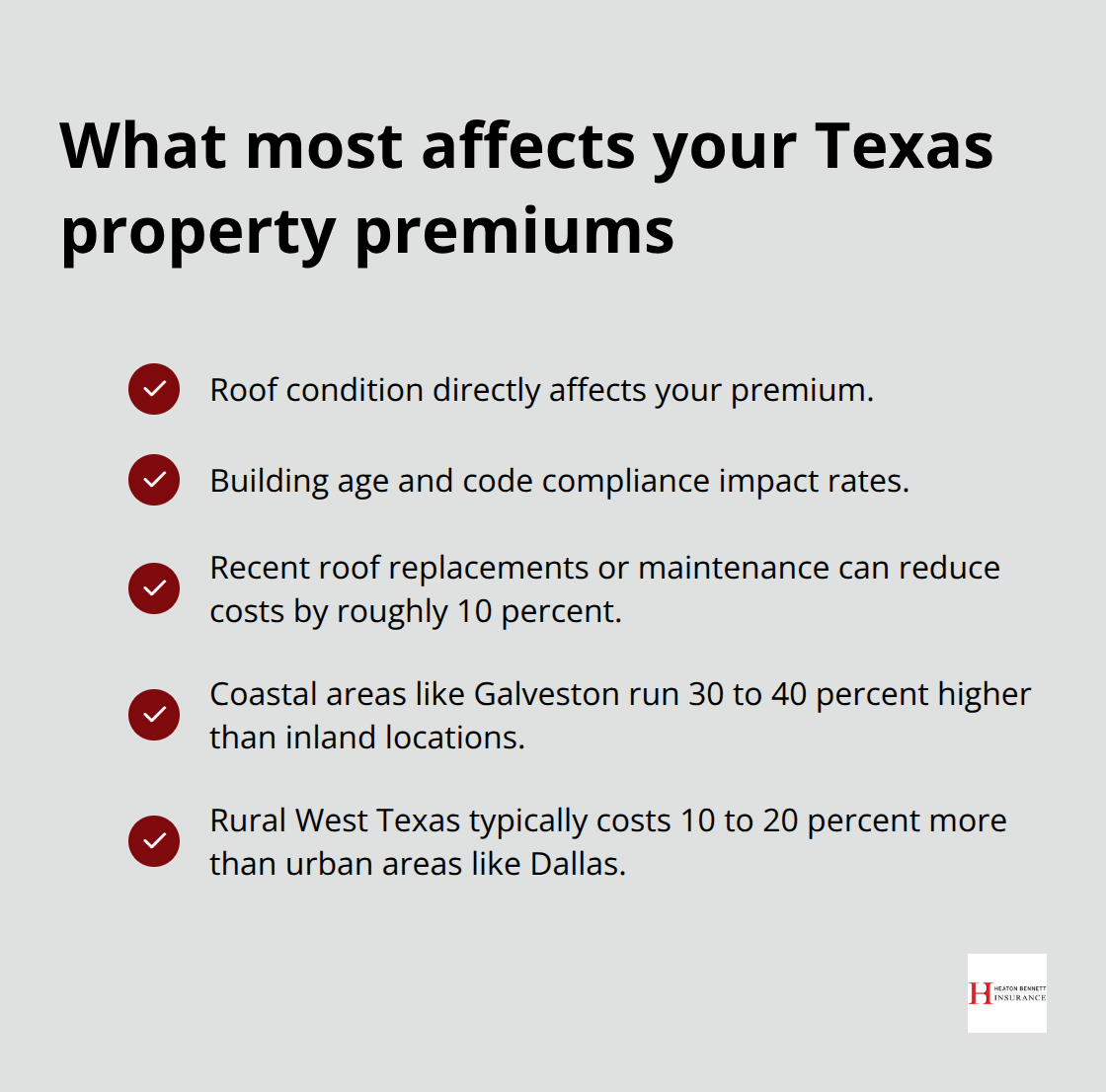

Hail causes the most consistent damage because it strikes unpredictably across regions where businesses have minimal warning. A single hailstorm can destroy roofs, shatter windows, and damage HVAC systems, leaving owners facing repair bills that often exceed $50,000 for medium-sized commercial properties. Roof condition directly affects your premium, which means a property hit by hail once becomes exponentially more expensive to insure going forward.

Flood Risk Across Texas Regions

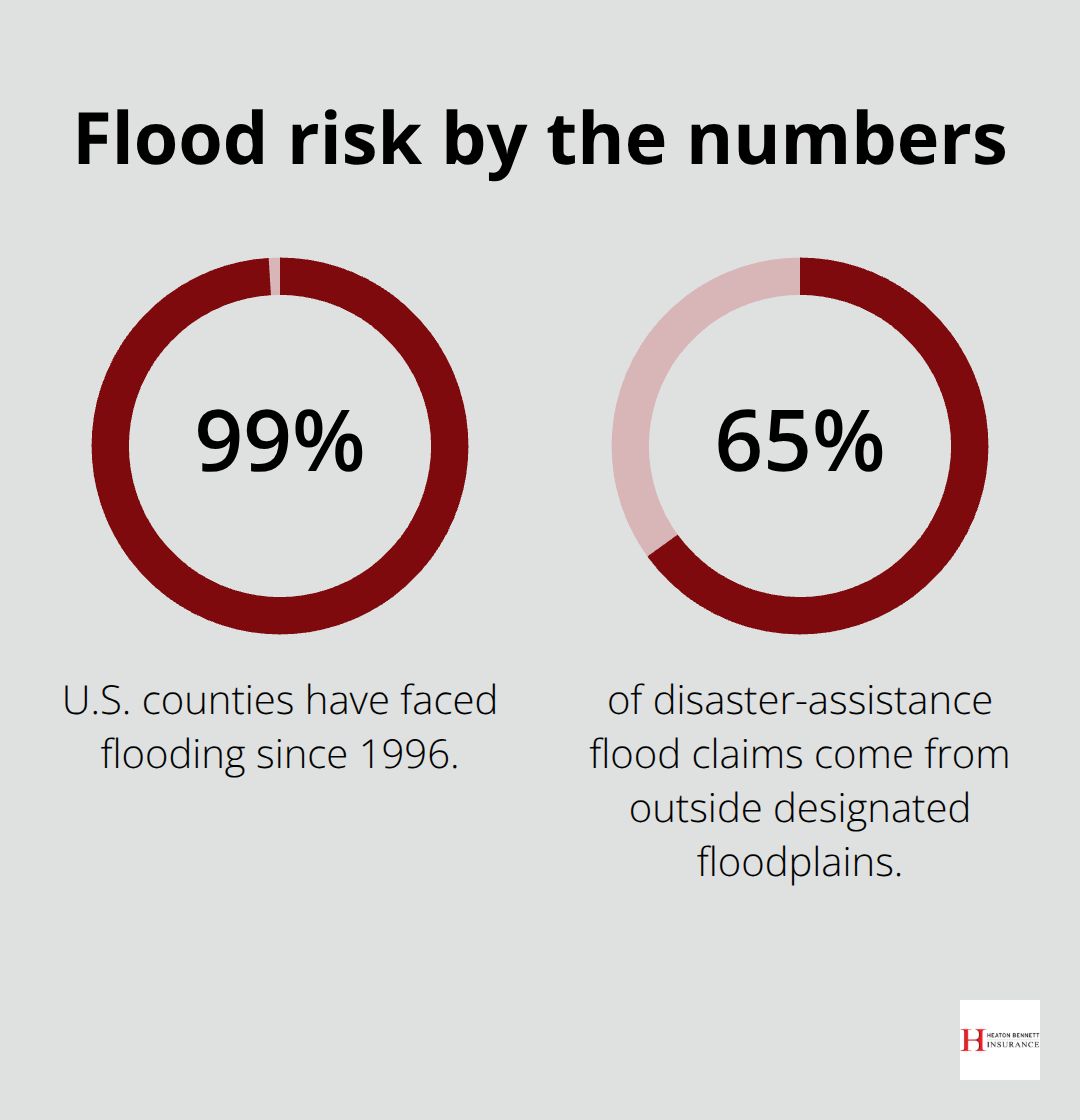

Flooding presents an even more dangerous gap because standard commercial property policies exclude water damage entirely. Since 1996, 99 percent of U.S. counties have faced flooding, yet most Texas businesses remain uninsured for this peril. Just one inch of water causes approximately $26,000 in damage according to FEMA data, and many companies don’t realize their coverage won’t touch it until the water arrives.

The 2025 Houston floods demonstrated exactly this problem-businesses with standard policies recovered nothing, while those carrying separate flood insurance through the National Flood Insurance Program or private carriers protected their operations. Your location determines your flood exposure; coastal areas face different risks than inland regions, and properties outside traditional floodplains still experience significant flood losses (about 65 percent of disaster-assistance flood claims come from outside designated floodplains).

Drought Impact on Agriculture and Operations

Drought impacts agricultural and operational costs differently but equally severely. Businesses depending on water supply face rising operational expenses when drought conditions tighten availability and increase costs. Agricultural operations see crop losses compound quickly, affecting not just the current season but financing for the next one.

Beyond agriculture, drought increases wildfire risk across Texas, particularly in rural areas and expanding development zones. You can check your property’s specific wildfire exposure through the Texas Wildfire Risk Assessment Portal, and that risk directly influences your insurance costs and availability. Regional variation matters enormously-coastal areas like Galveston run 30 to 40 percent higher than inland locations, while rural West Texas typically costs 10 to 20 percent more than urban areas like Dallas.

Understanding Your Property’s Risk Profile

A business in high-risk tornado zones faces different exposure than one in drought-prone regions, meaning coverage needs and pricing vary dramatically across the state. Loss runs from previous property owners reveal past claims and help you understand what actually happened at your location, not what you assume happened. This documentation matters because underwriters use it to assess real risk rather than theoretical exposure.

Building age and roof condition heavily influence your rates-newer code-compliant structures with recent roof replacements often receive noticeable discounts, sometimes reducing premiums by 10 percent or more through proper maintenance documentation. Understanding these factors positions you to make informed decisions about the coverage you actually need, which brings us to how weather risk insurance protects your business against these specific threats.

How Weather Risk Insurance Protects Your Business

Property Damage Coverage Tailored to Texas Threats

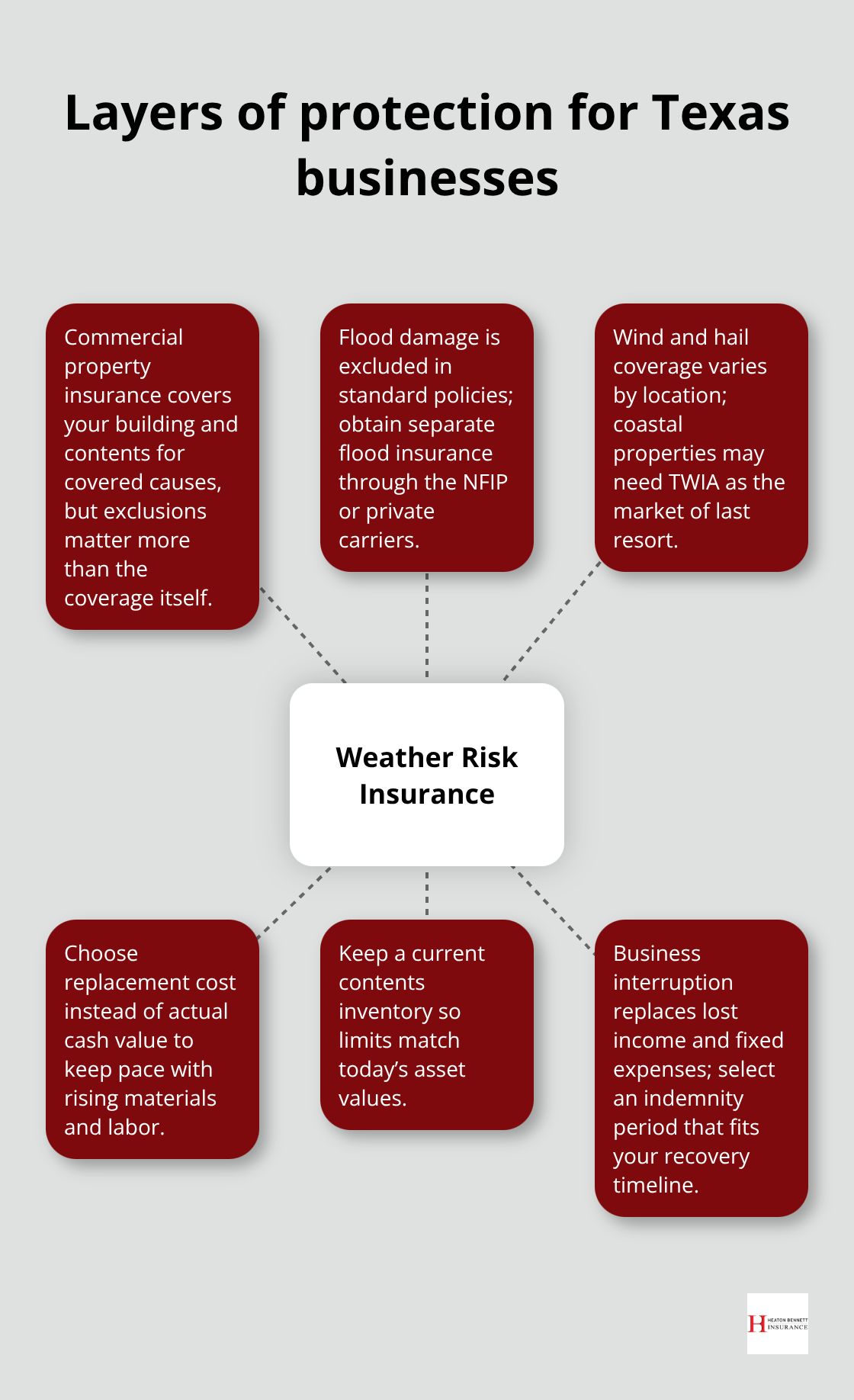

Commercial property insurance in Texas must account for the specific perils that actually threaten your business. Standard commercial property policies protect your building and contents from covered losses, but the exclusions matter more than the coverage itself. Flood damage does not exist in standard policies, which means you need separate flood insurance through the National Flood Insurance Program or private carriers to cover water damage. Wind and hail coverage varies by location; coastal properties often find wind coverage unavailable in the voluntary market and must turn to the Texas Windstorm Insurance Association, which serves as the wind and hail coverage of last resort for coastal counties with more than 237,000 policies statewide.

Building coverage should always be on replacement cost rather than actual cash value, because rising materials and labor costs mean your reconstruction expenses will exceed what you paid for the original structure. Roof condition directly impacts your wind and hail premiums, so documenting recent replacements or maintenance records can reduce costs by roughly 10 percent. Contents coverage requires regular inventory updates to match your current asset values; underinsuring this protection leaves you exposed when losses occur, and many business owners discover too late that their limits do not match what they actually own.

Business Interruption and Recovery Protection

Business interruption insurance replaces lost income and covers fixed expenses while your operation recovers after a covered weather event, making it essential in Texas where recovery timelines can stretch weeks or months. You must select an indemnity period that matches how long your business needs to resume normal operations; a restaurant might recover in two weeks while a manufacturing facility needs three months. Ordinance and law coverage pays for costs to update to current building codes after damage, which matters significantly in Texas because updated local codes often require electrical, plumbing, and structural upgrades that were not necessary in the original construction.

Bundling Coverage and Managing Deductibles

In high-risk regions where premiums rose 10 to 40 percent between 2023 and 2025, bundling multiple coverages through a Business Owners Policy often costs $1,000 to $3,000 annually and provides broader protection than purchasing coverages separately. Raising your deductible lowers monthly premiums substantially, but only if you can afford to pay that deductible out of pocket after a loss occurs; choosing a $10,000 deductible to save $200 monthly creates disaster if you cannot fund the deductible when needed. The right balance between premium savings and financial capacity determines whether a higher deductible actually works for your operation.

Understanding these protection layers positions you to make informed decisions about coverage limits and exclusions. The next step involves assessing your specific business vulnerabilities and comparing what different carriers actually offer in your region.

Securing the Right Coverage for Your Texas Business

Document Your Property’s Actual Vulnerabilities

Selecting weather risk insurance for your Texas operation means moving beyond generic quotes and understanding what actually covers your specific exposure. Start by pulling loss runs from previous owners to see what weather events have struck your location, then cross-reference that history against your current building condition and contents inventory. A property with three hail claims in five years requires different coverage than one with a clean history, and underwriters will price accordingly.

Next, identify which perils pose the greatest threat based on your region. Coastal businesses need windstorm coverage through the Texas Windstorm Insurance Association, inland operations in tornado zones require robust property protection, and any property near water needs separate flood insurance regardless of traditional floodplain maps (since 65 percent of disaster claims come from outside designated zones).

Calculate Your Recovery Timeline and Coverage Needs

Calculate your actual recovery timeline if a weather event forced shutdown. If you need four months to resume operations, your business interruption indemnity period must cover four months, not three. Many owners guess at this number and under-insure, then face income gaps when recovery takes longer than expected. Building coverage should always be on replacement cost rather than actual cash value, because rising materials and labor costs mean your reconstruction expenses will exceed what you paid for the original structure.

Contents coverage requires regular inventory updates to match your current asset values; underinsuring this protection leaves you exposed when losses occur. Roof condition directly impacts your wind and hail premiums, so documenting recent replacements or maintenance records can reduce costs by roughly 10 percent.

Compare Quotes Across Multiple Carriers

Comparing carriers across Texas requires understanding that market capacity varies dramatically by location and risk profile. In high-risk coastal areas, you may find only TWIA available for wind coverage or limited options for property insurance entirely, while inland Dallas-area businesses access multiple voluntary carriers with better rates.

Request quotes from at least three insurers using identical building specifications, contents values, and coverage limits so you can actually compare apples to apples rather than chasing the lowest number. Verify whether quotes include all necessary exclusions covered separately-flood must be added to standard policies, and wind or hail may require separate riders depending on your location (your agent can clarify these distinctions).

Work with an Independent Agent

An independent agent accesses multiple carriers rather than locking you into one company’s limited options, and they know which insurers actually write in your specific area and what coverage gaps exist in their standard forms. An independent agent understands Texas weather risks and carrier appetites across different regions, positioning you to select protection that matches your actual exposure rather than settling for whatever seems cheapest.

Final Thoughts

Weather risk insurance in Texas protects your bottom line by covering the specific threats your business actually faces. Hail, flooding, and drought create financial exposure that standard policies leave uncovered, and the regional variations across Texas mean your neighbor’s coverage won’t work for your operation. The businesses that survive weather events are those that planned ahead with proper protection rather than those scrambling after losses occur.

Tailored coverage matters because weather risk insurance Texas must account for your location, building condition, and recovery timeline. A coastal property needs windstorm coverage through TWIA that an inland Dallas business doesn’t require, and your roof condition, contents inventory, and loss history all influence what coverage you actually need and what you’ll pay for it. Generic policies from carriers unfamiliar with Texas risks leave gaps that become painfully obvious when weather strikes.

The path forward starts with documenting your property’s vulnerabilities and calculating your real recovery timeline. Pull loss runs from previous owners, check your wildfire exposure through the Texas Wildfire Risk Assessment Portal, and determine whether your location faces hurricane, tornado, hail, or flood risk. Contact Heaton Bennett Insurance today to assess your weather vulnerabilities and secure the coverage your Texas business needs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.