How to Insure Vacant Commercial Property

Empty commercial buildings face unique risks that standard policies often don’t cover. Property damage, vandalism, and liability claims can devastate unprepared owners.

We at Heaton Bennett Insurance see vacant commercial property insurance as essential protection during transition periods. The right coverage prevents financial disasters while your building awaits new tenants or buyers.

What Makes Vacant Property Insurance Different from Standard Coverage?

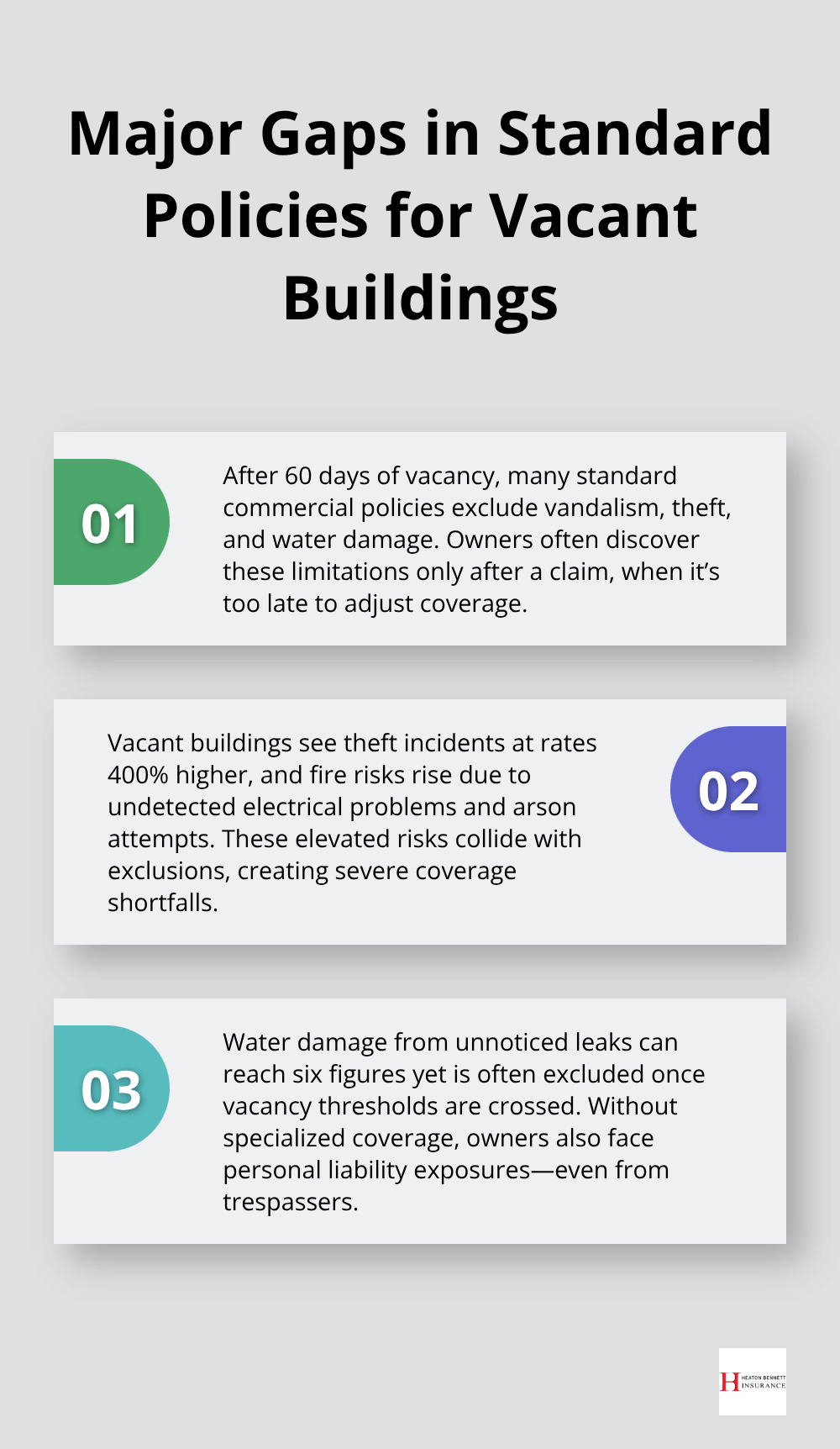

Commercial properties that sit empty for more than 60 days face insurance restrictions that catch most owners off guard. Standard commercial policies exclude or severely limit coverage once a building reaches 31% vacancy, which leaves owners exposed to significant financial losses. The Insurance Services Office defines vacant properties with this 31% threshold, and most insurers follow this guideline strictly. Office vacancy rates nationwide hit 18.2% in 2024 (a 30-year high), which means more property owners need specialized coverage than ever before.

Standard Policy Exclusions Create Major Gaps

Standard commercial insurance policies exclude vandalism, theft, and water damage coverage for vacant properties after 60 days. These exclusions exist because vacant properties experience theft incidents at rates 400% higher than occupied properties, while fire risks increase dramatically due to undetected electrical problems and arson attempts. Water damage claims from unnoticed leaks can reach six-figure amounts in vacant commercial spaces, yet standard policies won’t cover these losses.

Property owners who don’t secure specialized vacant property insurance face personal liability for injuries on their premises, even from trespassers.

Security and Maintenance Requirements Transform Coverage Terms

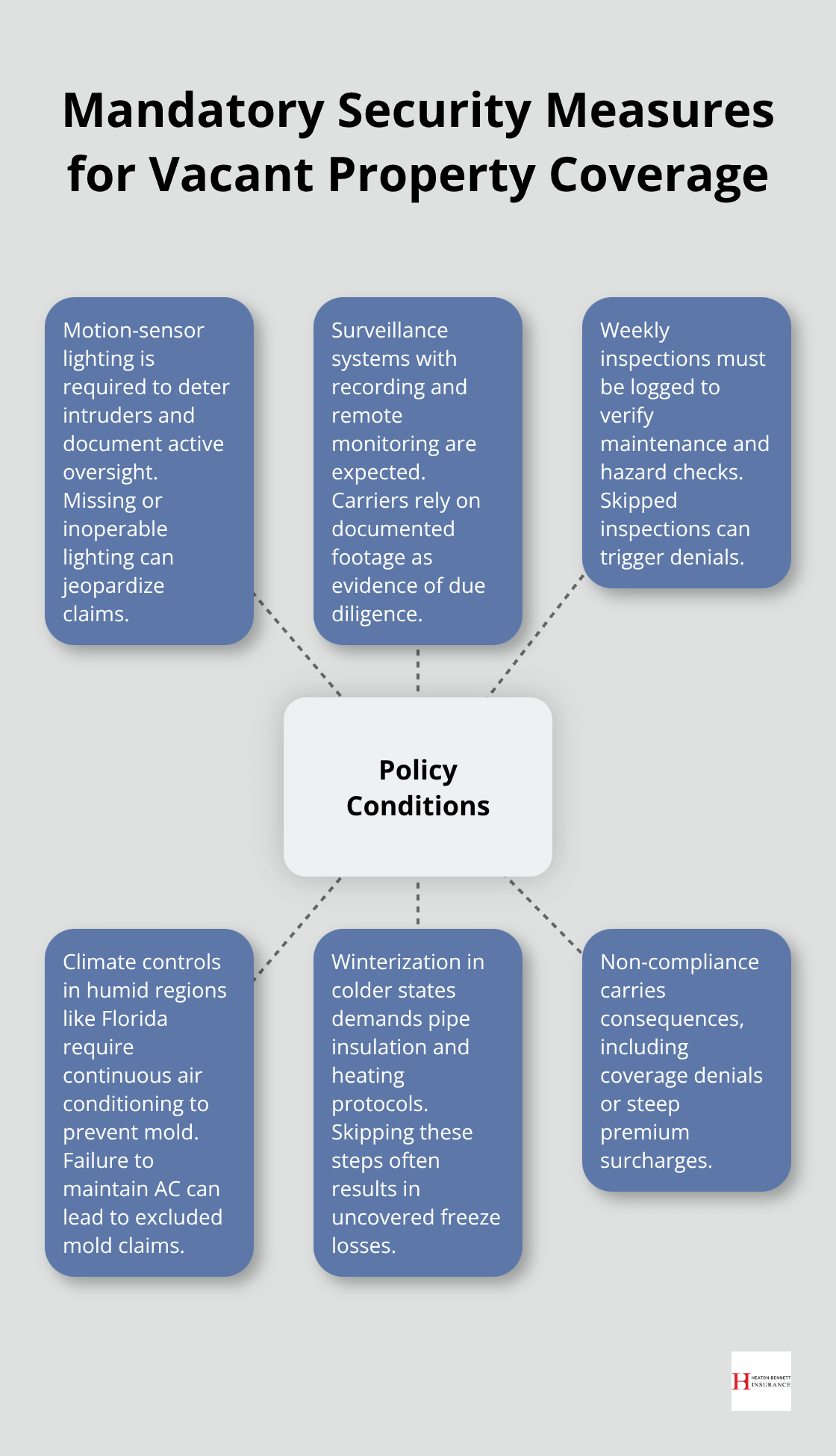

Vacant property insurers demand specific security measures that standard policies don’t require. Motion-sensor lights, surveillance systems, and weekly property inspections become mandatory rather than optional. Properties without these measures face coverage denials or premium increases of 200-300%.

Florida properties need continuous air conditioning to prevent mold growth, while northern climates require winterization protocols to prevent pipe damage. These requirements aren’t suggestions – they’re policy conditions that void coverage when ignored.

Specialized Carriers Fill the Coverage Void

Most major insurance companies won’t cover properties deemed vacant, which significantly limits available options for property owners. Specialized carriers step in to fill this gap with policies designed specifically for empty commercial properties. These carriers understand the unique risks and offer coverage that standard insurers exclude (fire, vandalism, and limited water damage protection). A business umbrella policy can provide additional catastrophic loss protection for vacant commercial properties. The next step involves understanding exactly what types of coverage these specialized policies provide and how they protect your investment.

What Coverage Options Protect Vacant Commercial Properties?

Vacant commercial property insurance operates through three core coverage areas that address the elevated risks empty buildings face. Property coverage protects the building structure and any remaining contents against fire damage, which occurs 60% more frequently in vacant buildings according to National Fire Protection Association data. This coverage typically provides limits up to $5 million for the building structure, with separate limits for contents and debris removal. Vandalism protection becomes standard rather than excluded, covers graffiti removal, broken windows, and structural damage from break-ins that cost property owners an average of $15,000 per incident based on FBI property crime statistics.

Fire Protection Addresses the Highest Risk

Fire coverage for vacant properties includes protection against arson, which accounts for 14% of all structure fires in unoccupied commercial buildings according to the National Fire Protection Association. Specialized policies cover both intentional fires and accidental blazes from electrical malfunctions that go undetected in empty buildings. Water damage from firefighting efforts receives coverage up to specified limits, while smoke damage protection extends to HVAC systems and any remaining fixtures. Properties with active sprinkler systems monitored by fire departments receive premium discounts of 15-25% (making fire protection system maintenance a smart financial decision).

Liability Coverage Protects Against Unexpected Lawsuits

General liability coverage for vacant properties protects against injuries to trespassers, delivery personnel, and prospective tenants who enter the premises. This coverage typically provides $1 million limits per occurrence, addresses slip-and-fall accidents, falls from debris, and other premises liability claims that can reach six-figure settlements. Medical payments coverage handles immediate medical expenses regardless of fault, while personal injury protection covers claims related to wrongful eviction or discrimination during the vacancy period. Properties without adequate liability coverage face personal asset exposure when lawsuits exceed available coverage limits.

Business Interruption Insurance Provides Income Protection

Business interruption insurance offers financial relief during periods when vacant properties cannot generate rental income due to covered losses. This coverage pays for lost rental income and continuing expenses like mortgage payments, property taxes, and utilities while repairs take place. The coverage period typically extends from 12 to 24 months (depending on policy terms), which gives property owners time to complete repairs and find new tenants. Properties that maintain this coverage avoid cash flow problems that force distressed sales during extended vacancy periods.

Smart property owners who understand these coverage options need effective strategies to control their insurance costs while maintaining adequate protection. Commercial property insurance providers offer specialized policies designed specifically for vacant property insurance needs.

How Can You Cut Vacant Property Insurance Costs?

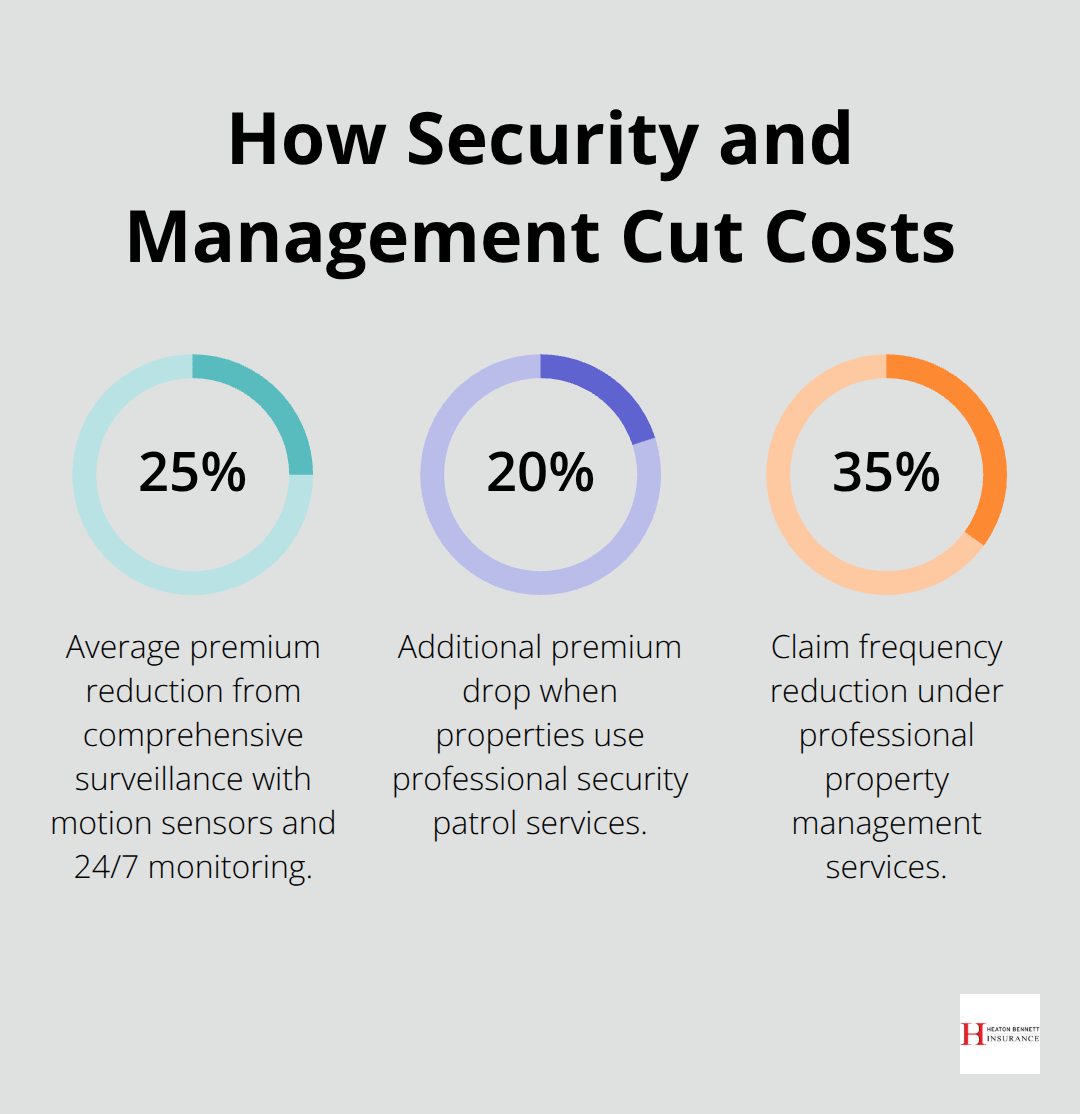

Property owners reduce vacant commercial insurance premiums by 30-50% through strategic security investments and proactive maintenance programs. Comprehensive surveillance systems with motion sensors and 24/7 monitoring cut premiums by an average of 25% according to commercial insurance data. Motion-activated exterior lights cost $2,000-5,000 to install but generate annual savings of $3,000-8,000 on insurance premiums for properties valued over $500,000. Smart alarm systems that notify local police departments immediately receive additional discounts of 10-15% from specialized carriers. Properties with professional security patrol services see premiums drop by another 20% because insurers view regular human oversight as the strongest deterrent against vandalism and theft.

Weekly Inspections Prevent Costly Claims

Regular property inspections prevent small problems from becoming expensive insurance claims that drive up future premiums. Weekly walkthroughs that document plumbing systems, electrical panels, and roof conditions catch issues before they cause water damage or fire hazards. Properties with documented inspection schedules receive premium credits of 15-20% from carriers who recognize proactive maintenance reduces claim frequency by 40%. Winterization protocols that include pipe insulation and heating system maintenance prevent freeze damage claims that average $25,000 per incident in northern climates. Air conditioning maintenance in humid climates like Florida prevents mold growth that can trigger claims exceeding $100,000 for commercial properties.

Specialized Carriers Offer Better Terms Than Standard Insurers

Direct work with carriers that focus exclusively on vacant properties generates savings of 25-40% compared to standard insurers who view empty buildings as high-risk accounts. These specialized carriers understand vacant property risks and price policies more competitively because they don’t need to subsidize losses from other coverage lines. Portfolio policies that cover multiple vacant properties under one policy reduce administrative costs and generate bulk discounts of 10-20%. Property owners who increase deductibles from $1,000 to $5,000 can reduce premiums by nearly 20% (provided they can handle higher out-of-pocket expenses during claims).

Professional Property Management Services Lower Risk Profiles

Property management companies that specialize in vacant buildings provide comprehensive oversight that insurers reward with premium discounts. These services include regular maintenance checks, emergency response protocols, and security coordination that reduce claim frequency by 35%. Professional management companies maintain relationships with local contractors who respond quickly to issues like roof leaks or broken windows before they escalate into major claims.

Properties under professional management receive preferential treatment from insurers because documented maintenance records and rapid response times demonstrate reduced risk exposure.

Final Thoughts

Property owners must act before standard policy exclusions take effect at 60 days of vacancy. Comprehensive security systems, weekly inspection schedules, and specialized carriers reduce insurance costs by 30-50% while they prevent devastating financial losses. Vacant commercial property insurance protects investments during transition periods when standard policies fail.

General agents often lack the expertise that empty buildings demand. We at Heaton Bennett Insurance connect property owners with specialized carriers who offer competitive rates and comprehensive coverage. Our independent agency status provides access to multiple vacant property insurers (which means better terms and pricing for your specific situation).

Proper vacant property coverage extends benefits far beyond premium costs. Properties with adequate insurance maintain their value during extended vacancies and avoid forced sales due to uninsured losses. Smart property owners recognize that vacant commercial property insurance represents protection rather than expense, safeguarding their investments until new opportunities emerge.

![Annuities Explained The Ultimate Guide for Retirees [2025]](https://insureaustin.com/wp-content/uploads/emplibot/Annuities-Explained-The-Ultimate-Guide-for-Retirees-_2025__1760663225-80x80.jpeg)