Weather Related Property Insurance: What to Consider

Weather can destroy your home in seconds. A single storm, flood, or hail event can cost tens of thousands in repairs-and most homeowners don’t realize their standard policy won’t cover everything.

At Heaton Bennett Insurance, we help property owners understand their actual protection gaps. This guide walks you through assessing your weather-related property insurance needs and building a plan that actually covers your home.

Weather Actually Destroys Homes-And Your Policy Might Not Cover It

The Office of Financial Regulation reported that US homeowners’ property and casualty underwriting losses occurred in five of the last six years, with 2023’s first half showing losses even without a single mega-event. This isn’t bad luck-it’s the new normal. Severe convective storms, hail, flooding, and wind events hit differently now. NOAA data shows the US averaged 8.1 billion-dollar weather events annually from 1980 to 2022, and 2023 alone saw seven separate billion-dollar catastrophes in just the first half.

Your standard homeowners policy covers dwelling damage, personal property, liability, medical payments, and loss of use, but it has hard limits on what weather damage it actually pays for. Wind and hail damage typically fall under coverage, as do snow-related losses in most policies. However, water damage splits into categories that confuse most homeowners. Sudden, accidental water damage from a burst pipe might be covered, but gradual leaks from aging systems won’t be.

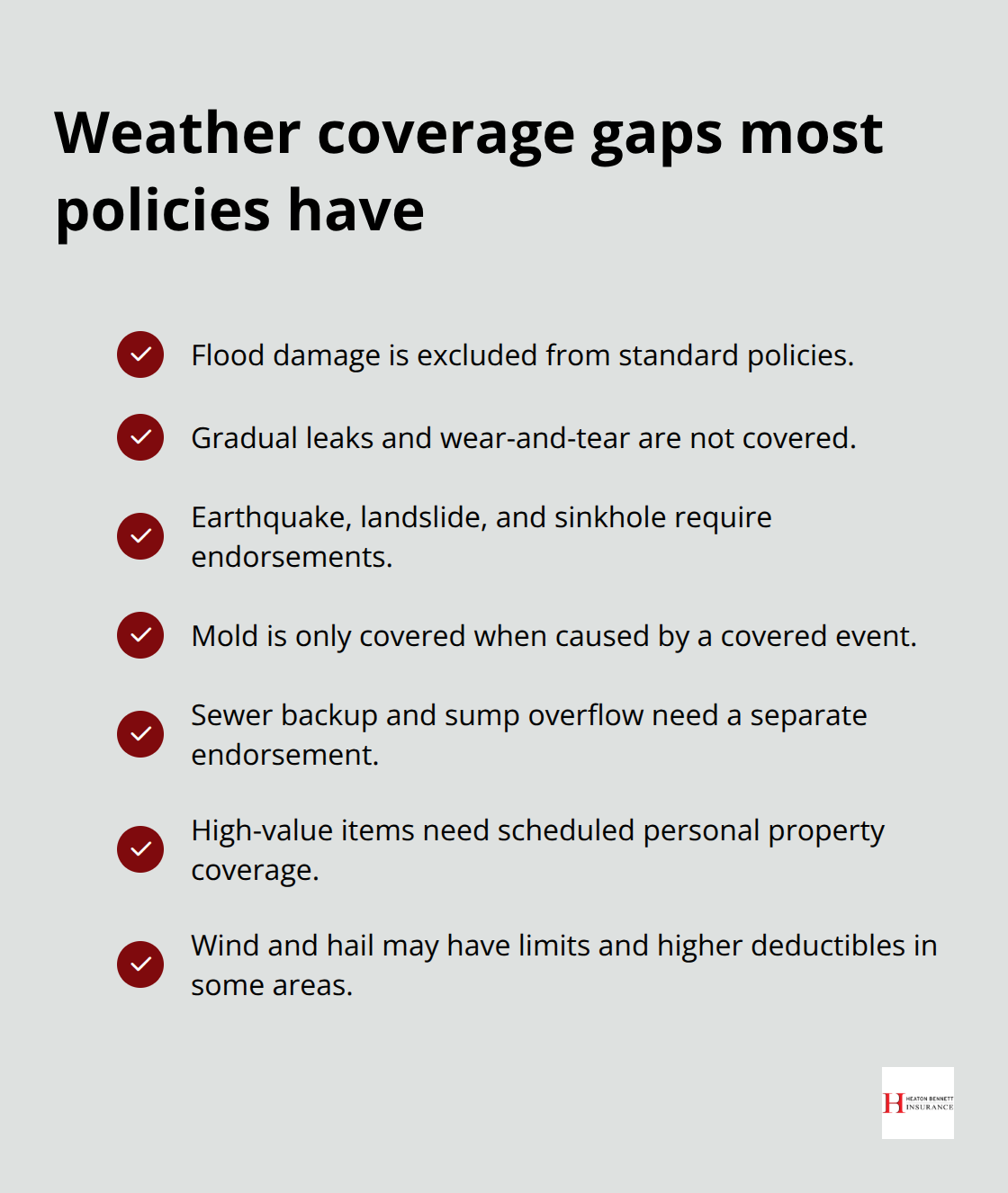

Flood damage is completely excluded from standard policies-you need separate flood insurance through the National Flood Insurance Program or a private insurer. Earthquake damage, landslides, and sinkholes are also excluded unless you add a specific endorsement. This matters because the reinsurance market has tightened significantly, forcing primary insurers to raise premiums and restrict coverage in high-risk areas, meaning the gaps in your policy grow more expensive to fill.

What Your Current Policy Actually Covers

Standard homeowners insurance protects against named perils like windstorms and hail, but the devil lives in the definitions section of your policy. The California Department of Insurance requires insurers to provide you a complete copy of your policy, including the declarations page, within 30 days of your request-obtain this and read it carefully. Review how the policy defines water damage, because sudden damage from a storm differs legally from water that seeps in over months. Ask your agent or insurer to explain exactly how much coverage you have and the proper steps to file a claim before you need to file one.

What Your Policy Explicitly Excludes

Mold is generally not covered unless it results from a covered event like a storm that breaks a window. General wear and tear, aging systems, and preventable failures are never covered. If your roof is old, insurers may limit roof-related claims or deny coverage entirely. High-value items like jewelry, art, or collectibles need scheduled personal property endorsements to be fully covered under a weather event. Sewer backups and sump pump overflow damage typically require a separate endorsement. Dog bite liability may be restricted by breed or history.

The Action You Need to Take Now

The practical step here is straightforward: obtain your declarations page today, identify what perils are listed, and ask your agent which endorsements make sense for your location and home age. This foundation matters because the next section covers the specific coverage options that actually fill these gaps-and knowing what you’re missing helps you understand which additions protect your home most effectively.

Know Your Property’s Real Weather Risk

Map Your Location’s Flood and Wildfire Exposure

Your location determines whether you need basic coverage or comprehensive protection. A house built in 1985 on the Gulf Coast faces different threats than a 2020 home in Denver, yet most homeowners treat weather risk as generic. The first step is mapping your actual exposure.

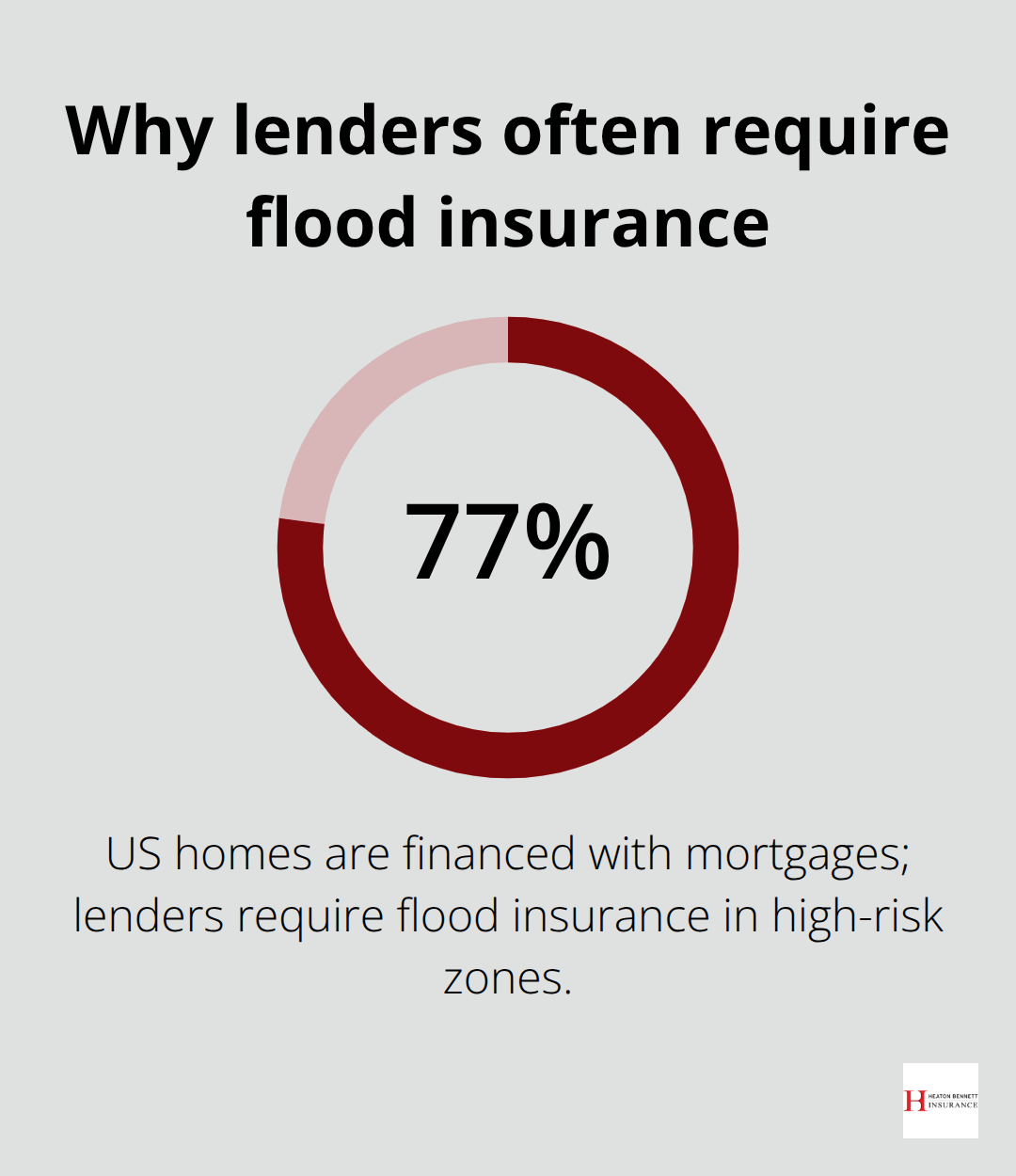

Check FEMA’s flood maps to see if your property sits in a flood zone-about 77 percent of US homes are financed with mortgages, and lenders require flood insurance if you’re in a high-risk zone. If you’re in California, CoreLogic estimates over 1.2 million homes face wildfire risk, and insurers have restricted coverage for roughly one in five of the leading homeowners policies statewide. If you live in Florida, understand that nine property and casualty insurers became insolvent since 2021, and Citizens Property Insurance now covers properties that private insurers have abandoned. These aren’t edge cases-they’re signs your property may be harder to insure and more expensive to protect.

Identify Your Home’s Structural Vulnerabilities

Next, examine your home’s structural vulnerabilities. An older roof with multiple layers of shingles fails faster under hail than a five-year-old roof. Homes near trees face higher wind damage risk, and properties with poor drainage invite flood damage. A local contractor or engineer can walk your property and identify vulnerabilities-this costs $200 to $400 but reveals exactly where your home bleeds money in a weather event. This assessment shows you which endorsements matter most before you talk to your insurance agent.

Review Your Area’s Claims History

Then pull your area’s claims history. Your county assessor’s office and local property records show what kinds of losses neighbors have filed. If you see patterns of wind damage, flood claims, or hail damage in your zip code, you know which endorsements matter most. Insurers price policies based on these patterns, so high-loss areas pay higher premiums-this is not unfair, it’s actuarial reality. Florida homeowners pay roughly $6,000 per year on average for homeowners insurance compared to $1,700 nationwide, a gap driven entirely by concentration of billion-dollar storms and insurer losses.

Connect Your Risk Profile to Coverage Decisions

Understanding your property’s specific risk profile-not a generic assessment of your state-lets you build coverage that actually matches your exposure and avoids paying for protection you don’t need. Once you’ve identified your location’s flood and wildfire exposure, assessed your home’s structural condition, and reviewed what losses your neighbors have filed, you’re ready to evaluate which additional coverage options will actually protect your investment.

Filling the Coverage Gaps Insurance Companies Won’t

Flood Insurance: The Coverage You Must Understand

Flood damage destroys homes faster than any other weather event, yet the National Flood Insurance Program carries roughly $20.5 billion in debt to the U.S. Treasury because standard homeowners policies exclude water damage entirely. If you live in a FEMA flood zone, your mortgage lender will require flood insurance, but flood risk exists everywhere-heavy rainfall overwhelms drainage systems in areas that never flooded before. The NFIP’s Risk Rating 2.0 program shifts toward full risk-based rates over multiple years, meaning premiums will climb steeply for properties with repetitive losses. Private insurers now offer flood coverage as an alternative to the NFIP, and these policies sometimes cost less and cover more than federal options.

The trade-off is availability: private flood insurers operate selectively, so if you live in a high-loss area, you may be locked into the NFIP regardless of cost.

Wind and Hail Coverage: Check Your Deductible

Standard homeowners policies cover wind and hail damage in most states, but in coastal areas like Florida and the Carolinas, insurers separate wind coverage into a distinct endorsement with higher deductibles-sometimes 5 to 10 percent of your home’s value instead of the standard $500 or $1,000. This means a $400,000 home might face a $20,000 deductible for wind damage, making the coverage worthless unless damage exceeds that threshold. CoreLogic data shows over 1.2 million California homes face wildfire risk, and in those regions, insurers increasingly restrict hail and wind coverage or withdraw entirely. Check your declarations page to confirm wind and hail are listed as covered perils, then ask your agent whether your deductible is standard or elevated.

Earthquake Insurance: Location Determines Value

Earthquake insurance requires a separate endorsement or standalone policy in virtually every state, and insurers price these policies aggressively because earthquake losses are catastrophic and unpredictable. California’s Proposition 103 rate regulation limits insurers’ ability to charge actuarially sound earthquake premiums, which is why coverage remains expensive and availability remains tight. A $500,000 home in Los Angeles might cost $1,500 to $3,000 annually for earthquake coverage with a 15 percent deductible, meaning you absorb the first $75,000 in losses yourself. In high-risk zones like the San Francisco Bay Area or the Los Angeles basin, earthquake insurance is worth the cost because a major event could total your home. In lower-risk areas like Denver or Austin, the premium-to-risk ratio may not justify the expense unless your home sits directly above a known fault line. Work with your agent to map your property against USGS earthquake hazard data, then run the numbers on whether the annual premium makes financial sense for your situation.

Final Thoughts

Weather destroys homes, and your standard policy won’t cover everything. The three steps we’ve outlined-understanding what your current coverage actually protects, mapping your property’s specific weather vulnerabilities, and identifying which endorsements fill your gaps-form the foundation of real weather related property insurance protection. Start by pulling your declarations page and asking your agent which perils are listed, then assess your location’s flood and wildfire exposure using FEMA maps and CoreLogic data.

The reinsurance market has tightened, premiums have climbed, and insurers have restricted coverage in high-risk regions, which means the cost of filling gaps grows every year. Acting now to build comprehensive protection costs less than waiting until after a loss forces you to scramble for coverage you can’t afford. Your home’s protection depends on moving forward with a plan that matches your property’s real risk profile, not a generic assessment of your zip code.

An independent agent who understands your property’s actual exposures can help you navigate these decisions and connect you with multiple carriers so you’re not locked into a single option. Contact Heaton Bennett Insurance to discuss your weather-related property insurance needs and build a protection plan that fits your home and your budget.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.