Restaurant Business Continuity: Planning for Disruptions

Restaurants face constant threats-from severe weather to supply shortages to sudden staff departures. Each disruption can halt operations and damage your bottom line.

At Heaton Bennett Insurance, we know that restaurant business continuity isn’t optional. The restaurants that survive disruptions are the ones that planned ahead.

What Disruptions Actually Cost Restaurants

The Real Financial Impact of Weather and Supply Chain Failures

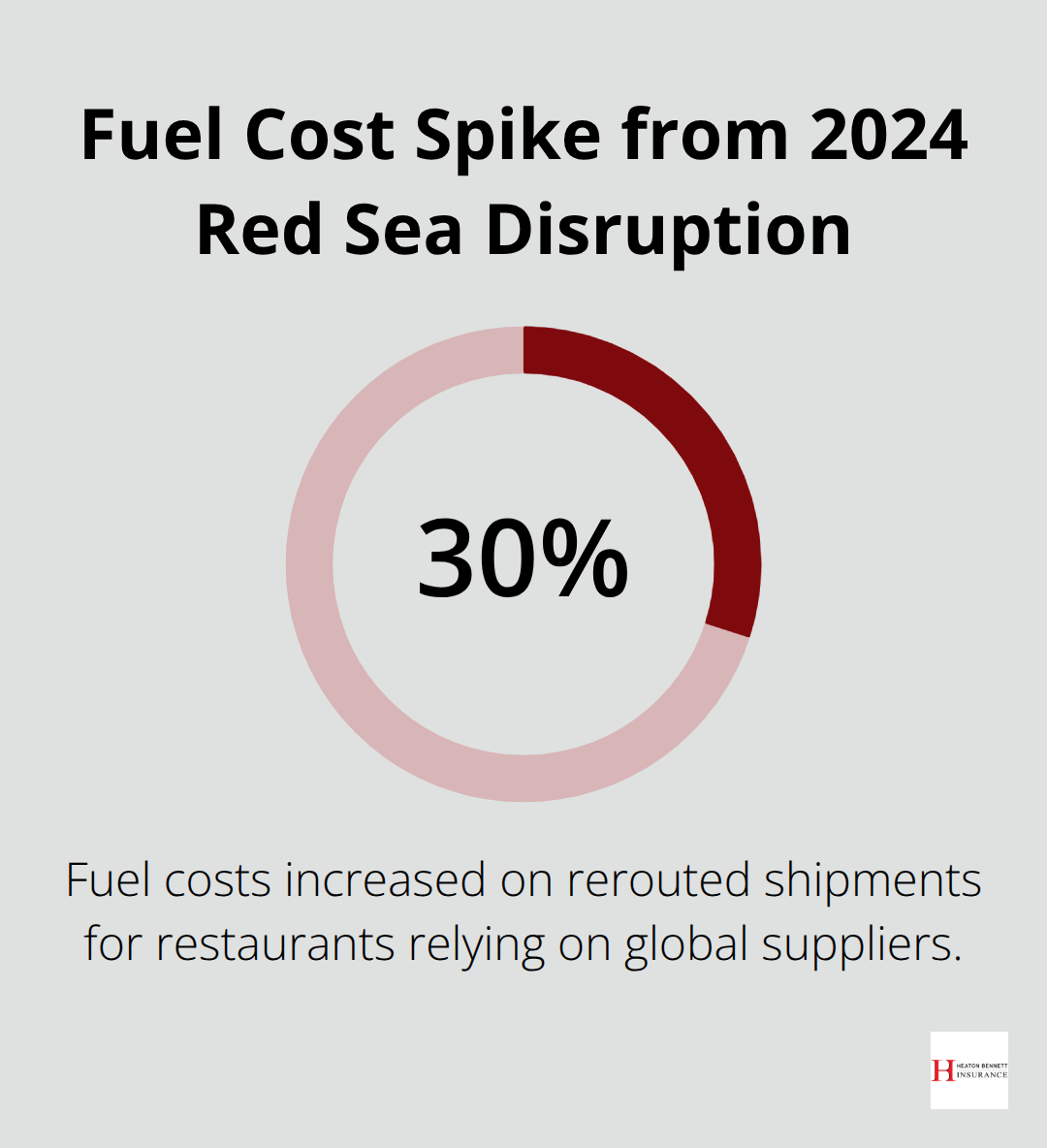

Weather events and supply chain failures hit restaurants harder than most businesses because your operation depends on continuous power, reliable deliveries, and consistent staffing. Atlantic hurricane season runs from June through November, and restaurants in coastal areas face real closure risks during these months. According to the National Restaurant Association, utility outages force restaurant closures and result in lost revenue without warning. Beyond weather, the Red Sea disruption in 2024 added approximately 4,000 miles and 2–3 weeks to shipments for restaurants relying on global suppliers, with fuel costs rising 30 percent. These aren’t theoretical problems-they directly hit your cash flow and customer relationships.

How Staffing Gaps Compound Your Losses

Staffing instability compounds these pressures because restaurant operations require immediate coverage when people don’t show up. A single server shortage forces you to cut tables or close sections, directly reducing revenue. Supply chain interruptions are worse because you lose control of the timeline. If your primary distributor fails or experiences delays, you cannot simply swap in another supplier without advance planning.

Building Your Response Before Crisis Strikes

The National Restaurant Association emphasizes that smart preplanning sets your operation up to withstand disruptions and recover more quickly than ad-hoc responses. This means identifying which utilities are critical to your operation-electricity for refrigeration and cooking, water for food prep and cleaning, gas for heating-and understanding exactly how long you can operate if each fails. Develop standard operating procedures for each scenario now, before a crisis forces you to improvise. Document what inventory you can salvage, which menu items you can still prepare, and which staff roles shift during outages. Create an outage response playbook that your team can execute immediately when disruptions occur, not something you figure out as the crisis unfolds.

Your next step involves translating this understanding into a formal business continuity plan that covers every critical operation your restaurant depends on.

Building Your Business Continuity Plan

Map Your Critical Dependencies

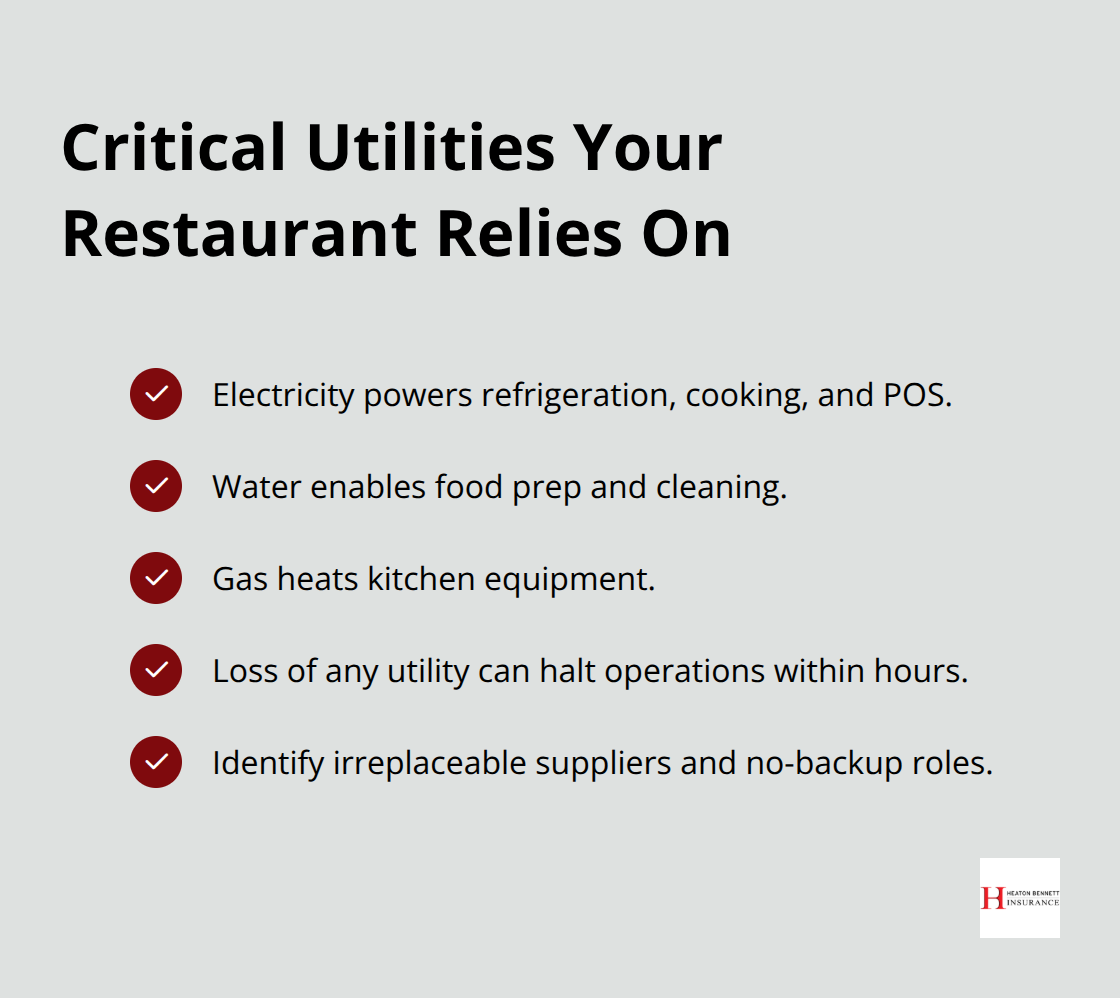

Start with a hard inventory of what actually stops your restaurant from operating. Electricity powers refrigeration, cooking equipment, and your POS system. Water enables food prep and cleaning. Gas heats your kitchen. If any one of these fails, your operation halts within hours.

The National Restaurant Association’s framework calls this step risk assessment, and it requires you to identify which utilities are critical and how their loss impacts service levels. Map your dependencies: which suppliers are irreplaceable, which staff positions have no backup, which menu items drive your revenue.

Write down exactly how long you can operate if electricity fails for 4 hours, 8 hours, or 24 hours. This isn’t guesswork. Test it. Know whether you can hand-write checks if your POS goes offline, whether you have a generator that actually works, whether your walk-in cooler can hold temperature long enough for you to salvage inventory. Document these findings in writing. A business continuity plan that lives only in your head disappears the moment crisis strikes.

Build Redundancy Into Your Supply Chain

The Red Sea disruption showed restaurants that relying on a single distributor is a liability, not a convenience. Identify backup suppliers now, before you need them. Contact at least two alternative sources for your top 20 ingredients and establish relationships with them during normal operations. Test ordering from your backup suppliers quarterly so you know lead times, quality standards, and whether they can actually scale up when your primary distributor fails.

This approach protects your revenue when primary suppliers experience delays or failures. The National Restaurant Association emphasizes that advance planning sets your operation up to recover more quickly than ad-hoc responses. Your backup suppliers become your insurance policy against supply chain shocks.

Cross-Train Staff and Document Procedures

For staffing, cross-train your team so multiple people can handle critical roles. A single sous chef or head bartender who leaves creates a dangerous gap. Document your standard operating procedures for every critical function: how orders flow, how inventory is tracked, how cash is handled, how food safety protocols work. The National Restaurant Association emphasizes that standard operating procedures guide actions during outages, including inventory management, service adjustments, and staff roles.

Create a written playbook for specific scenarios. If the power goes out during dinner service, who manages the POS backup, who communicates with guests, who assesses what food can be salvaged, who handles refunds or comps? Assign specific names to specific roles. When crisis hits, your team executes the plan rather than debates who should do what.

Test Your Plan Before You Need It

Your documented procedures only work if your team actually knows them. Walk through your outage scenarios with staff during slower shifts. Have your POS operator practice the manual checkout process. Ask your kitchen manager to identify which menu items they can prepare without electricity. Test your backup supplier relationships by actually placing orders. These exercises reveal gaps in your plan while you still have time to fix them (no customers are waiting, no revenue is at stake).

The restaurants that recover fastest from disruptions are the ones that practiced their response beforehand. Your business continuity plan transforms from a document gathering dust into a living operational guide that your team can execute under pressure.

With your critical operations mapped, backup suppliers identified, and staff trained on their roles, you now need to protect your financial exposure when disruptions do occur. Insurance coverage fills the gaps that planning alone cannot prevent.

Insurance Coverage That Protects Your Restaurant When Disruptions Strike

Your business continuity plan identifies what can fail and how to respond, but planning alone does not cover your financial losses when disruptions strike. Insurance fills the gaps between what you can prevent and what you cannot control. The difference between a restaurant that recovers from a major disruption and one that closes permanently often comes down to having the right coverage in place before crisis hits.

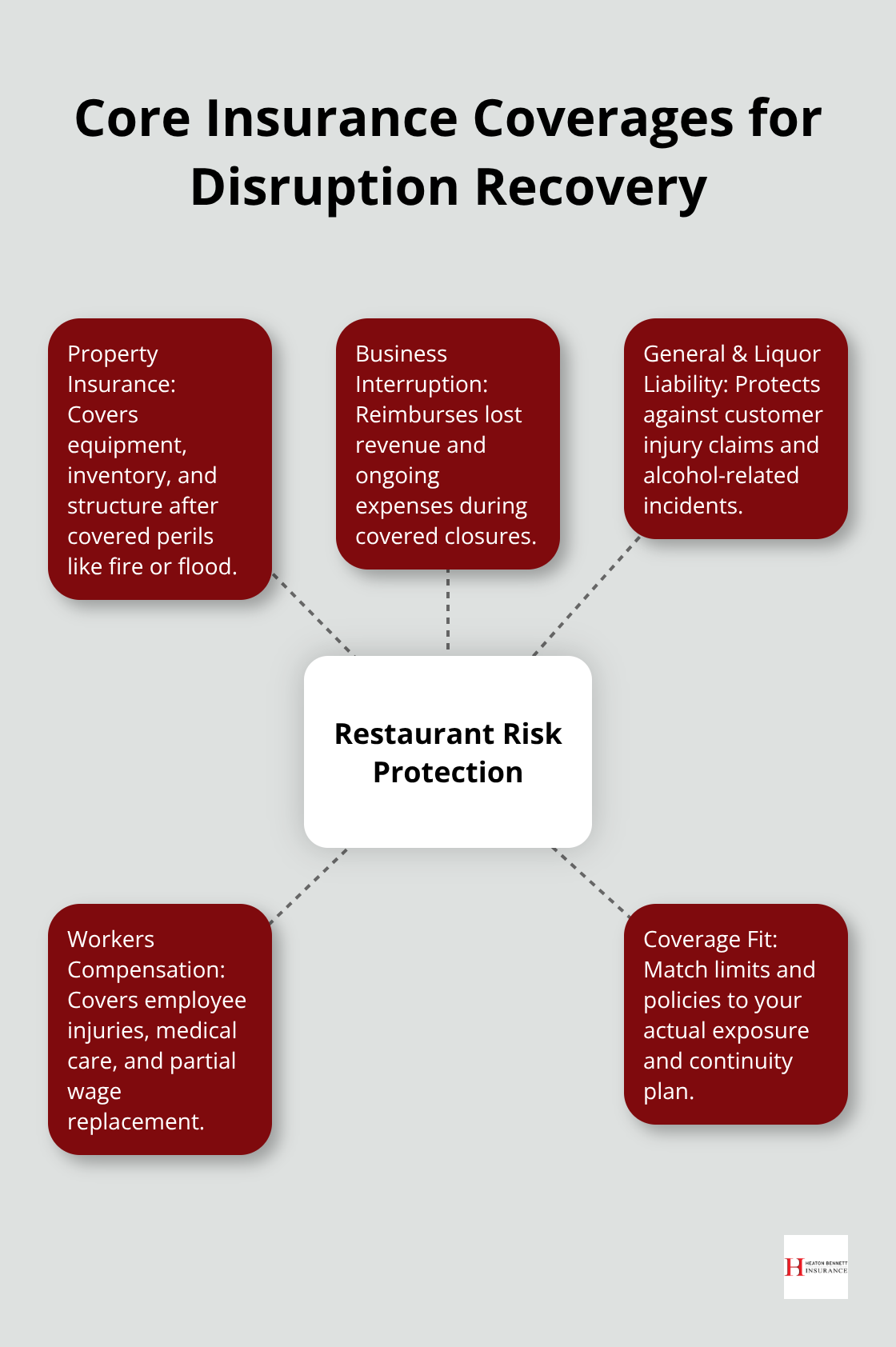

Property Insurance Covers Your Equipment and Inventory

Property insurance covers your equipment, inventory, and building structure when weather, fire, or other disasters damage them. A single kitchen fire or flood can destroy refrigeration units, cooking equipment, POS systems, and food inventory worth tens of thousands of dollars. Your property policy should cover replacement cost, not just actual cash value, because rebuilding your kitchen at current prices costs significantly more than it did when you originally purchased the equipment.

Review your policy limits annually because restaurant equipment depreciates on paper but costs far more to replace. If you have a generator as part of your continuity plan, make sure your policy covers it. Many restaurant owners discover too late that their coverage has gaps around backup power systems or outdoor equipment.

Business Interruption Insurance Reimburses Lost Revenue

Business interruption insurance reimburses lost income and operating expenses when a covered event forces you to close temporarily. If a utility outage shuts down your restaurant for three days, this coverage pays your lost revenue, payroll for staff you retain, and rent or mortgage payments. Without this coverage, you absorb the full financial impact yourself.

The National Restaurant Association notes that utility outages force restaurant closures and result in lost revenue without warning, making business interruption coverage essential for restaurants in areas prone to weather events or infrastructure failures. Calculate your average daily revenue and monthly fixed costs, then try to match your business interruption limits to those figures. Underinsuring this coverage means you cover the gap out of pocket.

General Liability and Liquor Liability Protect Against Customer Claims

General liability insurance protects you when a customer is injured at your restaurant and holds you responsible. A customer slips on a wet floor, suffers a fall, and sues you for medical bills and damages. Without general liability coverage, you pay the legal defense costs and any judgment from your operating capital.

Your policy should include premises liability for injuries that occur on your property, products liability for food-related illnesses, and liquor liability if you serve alcohol. Many restaurants underestimate their liquor liability exposure, especially if you serve late-night crowds or have a bar component. Liquor liability coverage is critical because it covers claims arising from serving alcohol to someone who then causes injury to themselves or others.

Workers Compensation Covers Employee Injuries and Protects Your Business

Workers compensation insurance is mandatory in most states and protects both you and your employees when someone is injured on the job. A line cook burns their hand on a griddle, a server ruptures a disc lifting heavy boxes, a dishwasher slips in the wet kitchen area. Workers compensation covers medical treatment, rehabilitation, and partial wage replacement while the employee recovers.

Without this coverage, injured employees can sue you directly for damages, and you face potential fines from your state labor department. The cost of workers compensation varies based on your payroll, your industry classification, and your claims history. Restaurants are classified as higher-risk than many other businesses because of kitchen hazards and fast-paced environments. Maintaining a strong safety culture and documenting your safety practices can help keep your claims history clean and your premiums lower.

Match Your Coverage to Your Actual Exposure

Many restaurant owners purchase insurance based on what they think they need rather than what they actually face. A restaurant in a flood-prone area needs different coverage than one in a stable location. A restaurant with a large bar operation needs higher liquor liability limits than one that only serves wine with meals. A restaurant that relies on a single distributor has different supply chain risk than one with backup suppliers in place.

Work with an insurance professional who understands restaurant operations and can assess your specific vulnerabilities. Your insurance should complement your business continuity plan by covering the financial impact of disruptions you cannot fully prevent, even with the best planning in place.

Final Thoughts

Restaurant business continuity requires two parallel tracks that work together. Your planning efforts identify what can fail, establish backup systems, and train your team to respond under pressure. Your insurance coverage protects your financial position when disruptions strike despite your best efforts. Neither approach works alone.

The restaurants that survive major disruptions act before crisis arrives. You map your critical dependencies, build relationships with backup suppliers, cross-train staff, and document procedures your team can execute immediately. You test these plans during normal operations so your team knows exactly what to do when pressure hits. Insurance fills the gaps that planning cannot eliminate-a generator keeps your refrigeration running during a power outage, but property insurance reimburses you if that generator fails and your inventory spoils.

Start with a realistic assessment of your operation. Which utilities would shut you down fastest? Which suppliers are truly irreplaceable? Which staff positions have no backup? Document your findings and build your continuity plan around these vulnerabilities. Then work with an insurance professional who understands restaurant operations to ensure your coverage matches your actual exposure. Contact Heaton Bennett Insurance today to review your current coverage and identify where your restaurant is exposed to disruption.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.