Contractor Liability Insurance Texas: A Quick Overview

Running a contracting business in Texas means managing real risks. One accident on a job site can lead to expensive lawsuits and financial losses that threaten your company’s survival.

Contractor liability insurance in Texas protects you from these threats. At Heaton Bennett Insurance, we’ve helped countless contractors understand their coverage options and build protection plans that fit their specific needs.

What Contractor Liability Insurance Actually Covers

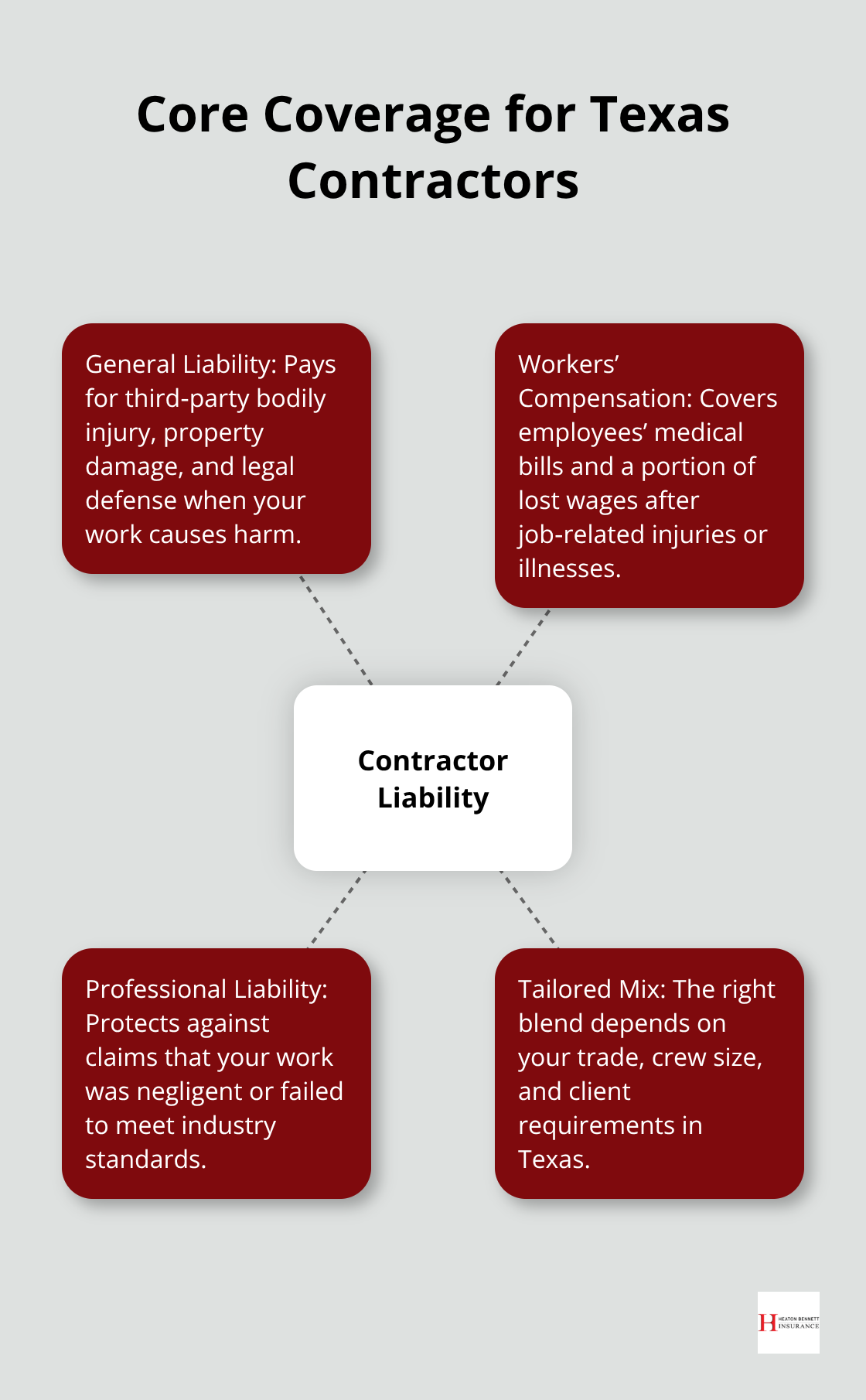

The Three Core Coverage Types

Contractor liability insurance protects your business when someone gets hurt or property gets damaged because of your work. General liability coverage pays for medical bills, repair costs, and legal fees if a client or third party sues you. Workers’ compensation covers your employees if they get injured on the job, paying their medical expenses and lost wages. Professional liability insurance, sometimes called errors and omissions coverage, protects you when a client claims your work was negligent or didn’t meet standards.

These three form the foundation of contractor protection in Texas, though the exact mix depends on your trade, the size of your crew, and what your clients require.

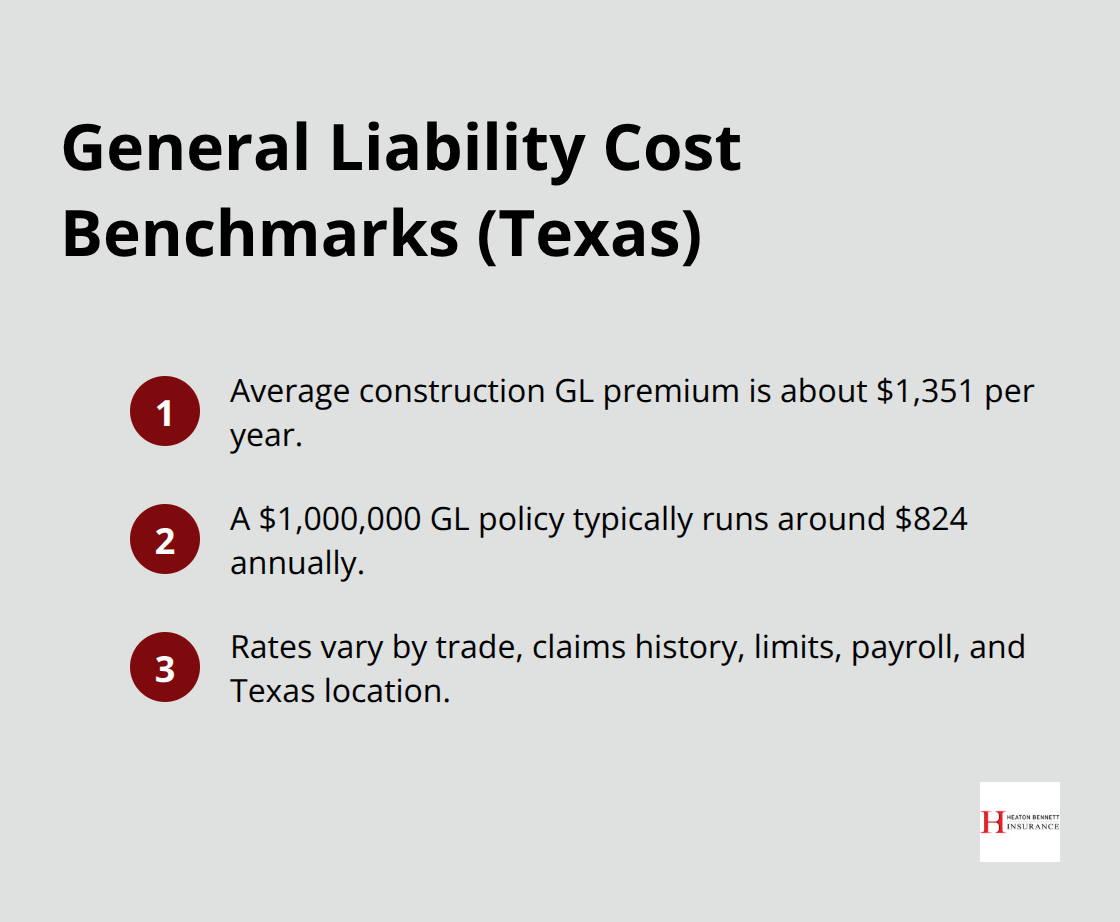

What General Liability Actually Costs

According to The Hartford, the average general liability policy costs about $1,351 per year for construction businesses, though rates vary significantly based on your specific trade and claims history. A $1,000,000 general liability policy typically runs around $824 annually, but that number shifts based on factors like the number of employees you have, your location within Texas, your coverage limits, your deductible, and whether you’ve had previous claims.

Texas Law Doesn’t Require It-But Your Clients Do

Texas doesn’t require general contractors to carry liability insurance by state law, but that’s where most contractors get it wrong. Municipalities across Texas demand proof of insurance before you can pull permits or start work on municipal projects. Commercial leases regularly require general liability coverage as a condition of occupancy. Most clients won’t hire you without a certificate of insurance showing adequate coverage.

If you work on projects with general contractors or developers, they’ll require you to carry coverage and often ask to be named as an additional insured on your policy (which protects them from liability claims tied to your work). The reality is that operating without liability insurance in Texas exposes your personal assets to catastrophic risk. A single lawsuit over a construction defect or injury can wipe out years of profit and force you into bankruptcy.

Why Contractors Can’t Afford to Wait

That’s why contractors serious about protecting their business don’t wait for a legal requirement-they get covered before their first job. The financial exposure is too high, and the market expectations are too clear. Once you understand what coverage costs and what it protects, the next step is figuring out which specific types matter most for your trade and your client base.

Types of Coverage Every Contractor Should Know

General Liability: Your Foundation Coverage

General liability stands as the foundation for any Texas contractor, and it’s where most of your protection dollars should go. This coverage handles bodily injury claims when someone gets hurt on your job site, property damage claims when your work damages a client’s building or belongings, and legal defense costs if you end up in court. According to The Hartford, a $1,000,000 general liability policy costs approximately $69 per month for construction businesses, though electricians typically pay $83 to $167 monthly, while roofers pay significantly more at $250 to $500 monthly due to higher injury rates. The Hartford reports that general liability costs average around $113 per month across all construction trades.

Your actual premium depends on your specific trade classification, the number of employees on your payroll, your location within Texas, previous claims history, and the deductible you choose. If a client requires you to carry a $2,000,000 limit instead of $1,000,000, expect to pay roughly 30% to 40% more annually. One serious injury claim can easily exceed $100,000 in medical costs and legal fees alone, which is why carrying this coverage isn’t optional in practice even if Texas law doesn’t mandate it. The hard truth is that skipping adequate general liability coverage creates personal liability exposure that can destroy your business.

Workers’ Compensation: Protecting Your Team

Workers’ compensation coverage protects your employees when they suffer job-related injuries or illnesses, covering their medical treatment, rehabilitation costs, and a portion of lost wages during recovery. Texas doesn’t require workers’ compensation for private employers, but if you work on public projects or government contracts, coverage becomes mandatory. More importantly, if you have even one employee and an accident occurs, you face massive personal liability without this protection.

The cost depends heavily on your trade classification and payroll; construction work classified as high-risk typically costs $15 to $25 per $100 of payroll annually, meaning a contractor with $500,000 in annual payroll might pay $7,500 to $12,500 yearly for workers’ compensation. This investment protects both your employees and your business from financial catastrophe when injuries happen on the job.

Professional Liability: Defending Your Workmanship

Professional liability insurance, also called errors and omissions coverage, protects you when a client claims your workmanship was negligent or failed to meet industry standards. This coverage pays defense costs and settlements for these claims, and many commercial contracts now require it as a condition of hiring. For trades like HVAC, plumbing, and electrical work, professional liability costs typically range from $500 to $2,000 annually depending on your revenue and claims history.

Bundling for Better Value

The smart approach combines these three into a Business Owner’s Policy, which pairs general liability and property coverage at a discount often worth 7% to 15% off your total premium compared to purchasing policies separately. This strategy reduces your overall cost while ensuring you maintain comprehensive protection across all three critical areas. When you work with an independent agency like Heaton Bennett Insurance in Austin, they can help you compare multiple carriers and find the right bundle that fits your specific trade and budget.

The next step involves understanding what types of claims actually happen on job sites and how your insurance responds when they do.

Common Claims and How Insurance Protects You

Property Damage Claims on Job Sites

Construction sites produce property damage claims constantly across Texas. A subcontractor’s equipment punctures a client’s roof during installation, or your crew accidentally damages an adjacent building while demolishing a wall. These claims typically range from $5,000 to $50,000, though they can exceed $100,000 when structural damage occurs. Your general liability policy covers the repair costs and legal defense if the property owner sues.

The deductible applies first to every claim, which most contractors overlook. If you carry a $2,500 deductible and the damage costs $8,000, your insurance pays $5,500 and you cover the rest. This detail shapes your deductible strategy significantly. A higher deductible like $5,000 lowers your monthly premium by 15% to 25%, but it also means you absorb more of smaller claims out of pocket. Most Texas contractors find that a $2,500 deductible balances affordability with manageable risk exposure.

Bodily Injury Claims and Medical Costs

Bodily injury claims carry far higher financial stakes than property damage and happen when someone gets hurt on your job site or because of your work. A homeowner trips over your equipment and breaks their leg, or a client’s employee gets burned by materials you’re using. Medical costs alone can reach $50,000 to $200,000 depending on injury severity, and if the injured party hires an attorney, legal fees add another $15,000 to $40,000 minimum.

Your general liability policy covers all of this, including the attorney’s fees to defend you in court. Workers’ compensation operates separately and covers only your own employees, paying their medical bills and 60% to 70% of lost wages during recovery. If you have employees and skip workers’ compensation coverage, a single serious injury can cost you $100,000 to $300,000 in medical expenses plus ongoing wage replacement, devastating most small contracting businesses.

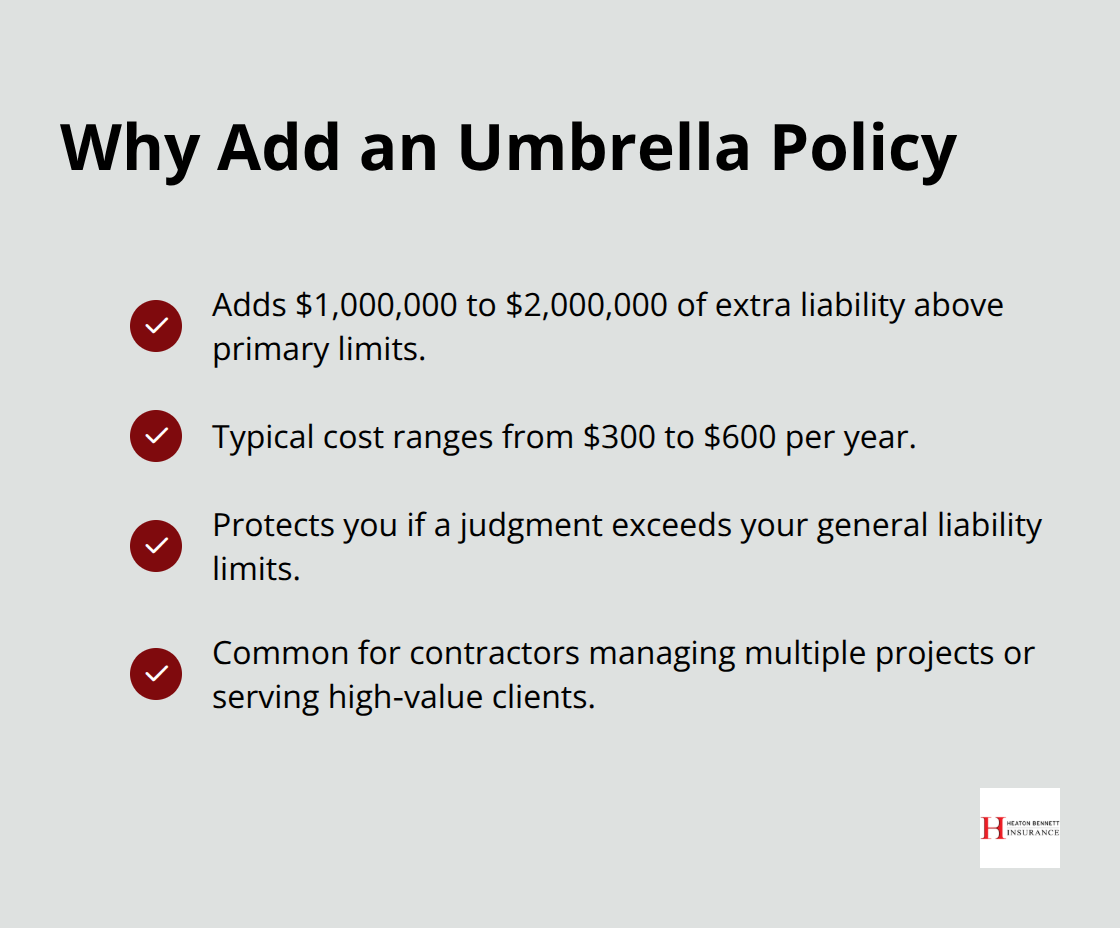

Third-Party Lawsuits and Umbrella Protection

Third-party lawsuits represent the most complex claims because they involve multiple parties with competing interests. A contractor you hired causes damage to a client’s property, and the client sues both you and the subcontractor. Your general liability policy covers your defense and any settlement or judgment up to your policy limits, typically $1,000,000 per occurrence.

However, if the judgment exceeds your policy limit, you pay the difference personally. This exposure is why many Texas general contractors now carry umbrella policies that provide an additional $1,000,000 to $2,000,000 in coverage for roughly $300 to $600 annually, protecting against catastrophic liability when claims spike beyond standard limits.

This extra layer of protection (sometimes called excess liability) has become standard practice for contractors managing multiple projects or working with high-value clients.

Final Thoughts

Contractor liability insurance in Texas protects your business, your employees, and your personal assets from the real risks that happen on job sites every day. A single bodily injury claim can cost $50,000 to $200,000 in medical expenses alone, while property damage claims regularly exceed $100,000 when structural damage occurs. Without proper coverage, these incidents transform from manageable business problems into personal financial catastrophes that force contractors into bankruptcy.

Texas contractors face a unique situation where state law doesn’t mandate general liability coverage, but the market does. Municipalities require proof of insurance before issuing permits, clients won’t hire you without a certificate of insurance, and general contractors demand you carry coverage and often require additional insured status on your policy. The practical reality is that operating without adequate contractor liability insurance Texas isn’t an option if you want to compete for real work.

Finding the right coverage means matching your specific trade, employee count, and client requirements to a policy that actually protects you. Bundling general liability with property coverage through a Business Owner’s Policy typically saves 7% to 15% compared to buying policies separately, making comprehensive protection more affordable than most contractors expect. Work with an independent agency that has access to multiple carriers and understands Texas contractor needs-contact Heaton Bennett Insurance to start your coverage review today and get the protection your business actually needs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.