Restaurant Insurance Austin TX: Tailored Coverage for Local Markets

Running a restaurant in Austin means facing unique insurance challenges that generic policies simply don’t address. From slip-and-fall claims to liquor liability issues, the risks are real and costly.

At Heaton Bennett Insurance, we’ve helped Austin restaurant owners find restaurant insurance coverage that actually fits their operations. The right policy protects your business, your staff, and your bottom line.

Why Austin Restaurants Face Greater Insurance Risks

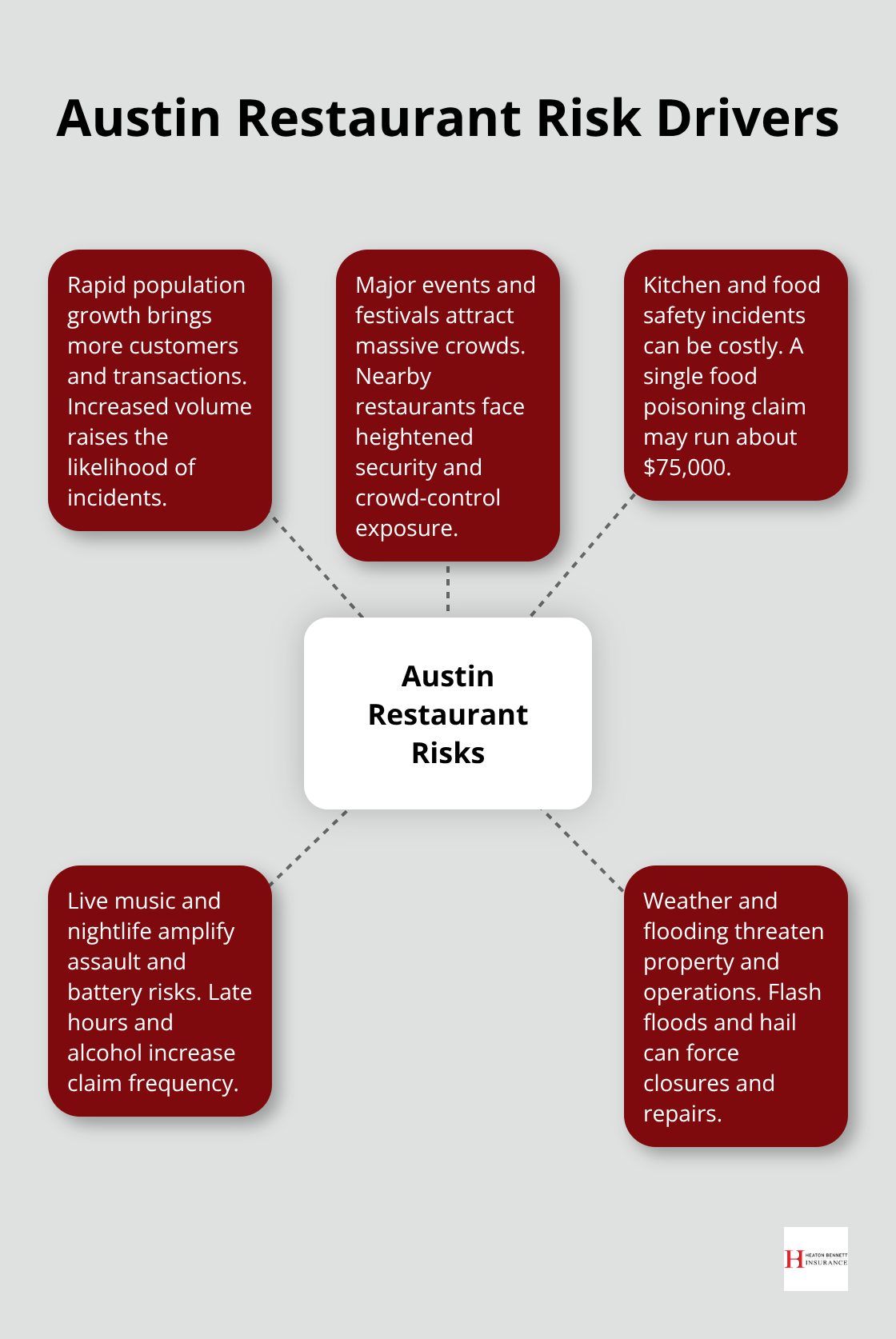

Austin’s restaurant landscape presents distinct challenges that go beyond typical operational headaches. The city’s rapid growth has created a perfect storm of liability exposure. With a metropolitan population exceeding 2.5 million and counting, Austin ranks as one of the fastest-growing regions in the United States. This explosive expansion means more customers, more transactions, and statistically more incidents. A single food poisoning claim costs about $75,000 in legal expenses alone, according to industry data.

Kitchen fires affect thousands of restaurants annually across the country, and Austin’s bustling food scene makes your operation a potential statistic. Austin’s status as the Live Music Capital of the World creates additional exposure for restaurants that host events or sit near large crowds. The city’s major events like SXSW and Austin City Limits draw massive crowds that strain operations and increase liability risks for nearby establishments.

Weather and Environmental Threats

Texas weather presents hazards that standard policies often miss. While Austin sits further inland than Gulf Coast regions, the state’s hail storms and flash flooding remain serious threats. Austin experiences flash floods regularly due to its geography and heavy rainfall patterns, which destroy inventory, equipment, and force temporary closures. Property damage from weather events easily reaches thousands of dollars without proper coverage. Equipment breakdown coverage becomes critical when a freezer fails during a power outage and spoils perishables worth thousands. Business interruption insurance isn’t optional in Austin-it covers lost revenue during forced closures from health department violations, storms, or other disruptions.

The Austin-Specific Liability Landscape

Austin’s alcohol culture amplifies liquor liability risks significantly. Restaurants and bars that serve alcohol face lawsuits from intoxicated patrons far more frequently than non-alcohol establishments. Assault and battery claims occur regularly in nightlife settings, particularly in venues near downtown and the entertainment districts. Workers’ compensation becomes essential when staff injuries happen during high-volume service periods. Generic policies fail because they don’t account for Austin’s specific operational patterns-late-night service, high customer turnover, and the prevalence of outdoor patios where weather exposure increases accident risk.

Cyber Threats in Silicon Hills

Cyber liability deserves serious attention in Austin, given the city’s position as Silicon Hills with major tech companies like Dell, Apple, Google, and Tesla headquartered or operating regionally. Restaurants that handle customer payment data face the same breach risks as tech companies. The P.F. Chang’s 2014 data breach affected 60,000 customers across 33 locations with losses around $3.5 million, demonstrating how payment processing vulnerabilities devastate restaurants. Your restaurant’s digital systems require protection that matches the sophistication of threats in this tech-forward market.

Understanding these Austin-specific risks shapes what coverage your restaurant actually needs. The next section breaks down the essential insurance types that protect against these distinct exposures.

Essential Coverage for Austin Restaurants

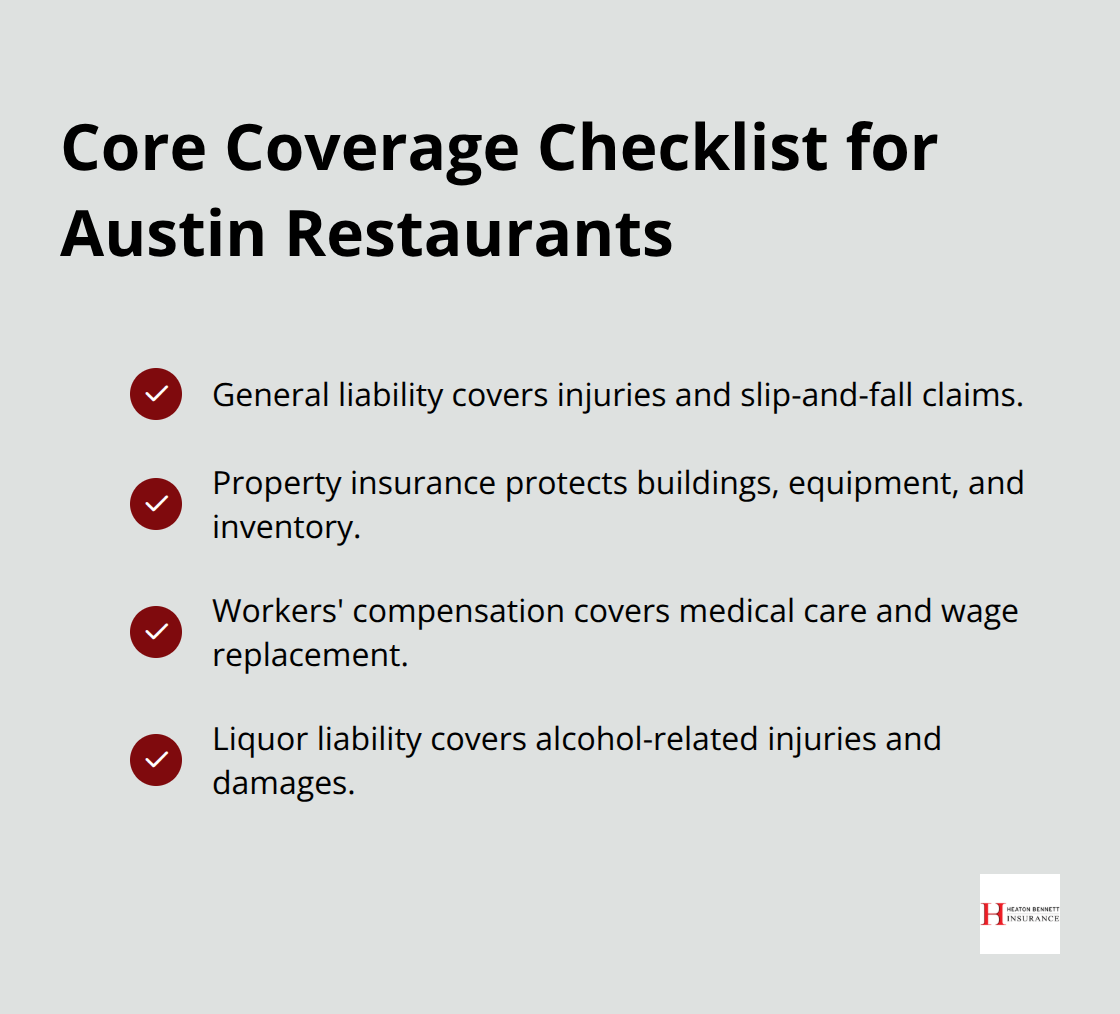

General Liability: Your First Line of Defense

General liability insurance protects your restaurant from the slip-and-fall claims and customer injury lawsuits that happen constantly in Austin’s busy dining scene. This coverage pays for medical expenses, legal defense, and settlements when a customer gets hurt on your premises. The average general liability policy for Texas restaurants costs between $800 and $2,500 annually, depending on your location, square footage, and customer volume. Austin restaurants in high-traffic areas like downtown or near entertainment districts pay premiums at the higher end because foot traffic increases incident frequency. Try securing at least $1 million in general liability protection rather than settling for minimum coverage limits of $300,000 or $500,000.

Austin’s litigation environment and high customer density mean serious injury claims can exceed what minimal coverage provides.

Property Insurance and Equipment Protection

Commercial property insurance covers your building, kitchen equipment, and inventory from fires, theft, and weather damage. This matters enormously in Austin because equipment breakdown during power outages forces spoilage of perishable inventory worth thousands of dollars. Standard property policies typically cost between $2,000 and $10,000 annually for Austin restaurants, but this varies dramatically based on your building’s age, construction materials, and location relative to flood zones. Flash flooding in Austin destroys restaurant inventory regularly, so add flood endorsements to your property policy rather than hoping standard coverage applies. Equipment floaters protect high-value kitchen gear like commercial ovens, refrigeration units, and POS systems when they fail or get damaged outside your main property policy.

Workers’ Compensation and Staff Protection

Workers’ compensation becomes mandatory the moment you hire your first employee in Texas, and it covers medical treatment and wage replacement when staff get injured during service. The cost depends entirely on your payroll and the number of employees you have, but this coverage isn’t optional. High-volume service periods create the greatest injury risk for your team, making adequate coverage essential for protecting both your staff and your business from liability exposure.

Liquor Liability: A Non-Negotiable Requirement

Liquor liability insurance specifically covers damages and injuries caused by intoxicated customers, including assault and battery claims that occur frequently in Austin’s nightlife venues. If you serve alcohol, liquor liability costs between $600 and $3,000 yearly depending on your annual alcohol sales and claims history. Austin’s bar and restaurant scene generates liquor liability claims constantly, making this coverage non-negotiable rather than nice-to-have. Many landlords and event organizers actually require proof of liquor liability before allowing alcohol service on premises, so this becomes a practical business requirement alongside legal protection.

These four coverage types form the foundation of restaurant protection in Austin. However, your specific operation may require additional layers depending on your menu, service model, and location. The next section walks you through selecting an insurance partner who understands these Austin-specific needs and can build a customized policy that actually covers your restaurant’s unique exposures.

Selecting an Insurance Partner Who Understands Austin’s Restaurant Market

Why Generic Policies Fail Austin Restaurants

Finding the right insurance provider means working with someone who understands Austin’s specific operational environment rather than applying a generic restaurant template to your business. Most national insurance companies treat Austin restaurants the same way they handle operations in rural markets or suburban strip malls, which misses the distinct risks that come with high-traffic urban locations, late-night service patterns, and weather exposure unique to Central Texas. An independent agency in Austin has access to multiple carriers and can match your restaurant’s actual risk profile to specialized policies rather than forcing you into standard packages.

Evaluating Provider Experience and Local Knowledge

When you contact potential providers, ask specifically about their experience with Austin restaurants that operate similar to yours. If they cannot reference restaurants in your neighborhood or with your service model, move on. The right partner should know the difference between insuring a food truck near Congress Avenue and a fine-dining establishment downtown, because those operations face completely different liability exposures and require different coverage structures. Heaton Bennett Insurance, an independent agency in Austin, provides access to multiple carriers and offers a Security Snapshot process that tailors coverage to your restaurant’s actual needs rather than one-size-fits-all solutions.

Comparing Quotes and Coverage Limits

Request detailed quotes from at least three providers and compare not just the annual premium but what each policy actually covers and excludes. A $2,000 annual policy with $500,000 in general liability protection leaves you dangerously exposed compared to a $2,500 policy with $1 million in coverage. Ask each provider to identify potential gaps in your current coverage or what they would recommend adding based on your specific operations.

The best providers also commit to annual policy reviews because your restaurant’s risks change as you expand service hours, add menu items, or modify your space.

Claims Support and Speed of Coverage

A provider who quotes you once and disappears until renewal time does not protect your business effectively. Ask about claims support too-when something goes wrong, you need an agency that handles the process directly rather than forcing you to navigate carrier bureaucracy alone. Most Texas restaurant insurance quotes can be bound within 24 to 48 hours, so speed matters when you need coverage fast, but do not let urgency push you toward a provider who has not properly assessed your actual risks.

Final Thoughts

Restaurant insurance in Austin TX requires more than standard coverage templates because your restaurant operates in a market shaped by rapid growth, weather threats, and liability exposures that generic policies overlook. The foundation of protection starts with general liability, property insurance, workers’ compensation, and liquor liability if you serve alcohol. These four coverage types address the most common claims Austin restaurants face, from slip-and-fall incidents to equipment failures during power outages.

Tailored coverage solutions matter because your restaurant’s specific risks depend on your location, service model, menu, and operational hours. A food truck near Congress Avenue faces different exposures than a downtown fine-dining establishment, and a late-night bar with outdoor patios encounters different hazards than a lunch-focused café. Generic policies force you into coverage structures that either leave dangerous gaps or waste money on protections you don’t need.

The right insurance partner understands Austin’s restaurant landscape and identifies coverage gaps before they become expensive problems. Contact Heaton Bennett Insurance for a free quote and risk assessment, and most restaurant insurance quotes bind within 24 to 48 hours so you can move quickly from assessment to protection. Your restaurant’s success depends on managing risks before they damage your business, and proper insurance coverage removes that uncertainty.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.