Contractor Insurance Quotes: How to Compare Multiple Providers

Contractor insurance quotes vary wildly from provider to provider, and most contractors waste time comparing apples to oranges. The difference between a cheap policy and the right policy can cost you thousands when a claim happens.

We at Heaton Bennett Insurance help contractors cut through the noise and find coverage that actually protects their business. This guide walks you through exactly what to look for and how to spot the deals that sound good but leave you exposed.

What Makes a Quote Worth Comparing

Look Beyond the Premium Number

The real work in comparing contractor insurance quotes happens before you look at the price tag. Most contractors focus on the premium number and miss the details that determine whether a policy will actually pay when you need it. General liability limits of $1 million per occurrence sound solid until you file a claim and realize your aggregate annual limit is only $500,000-meaning a second incident that year leaves you uncovered. Contractors pick quotes based on cost and later discover gaps that cost far more than the premium savings.

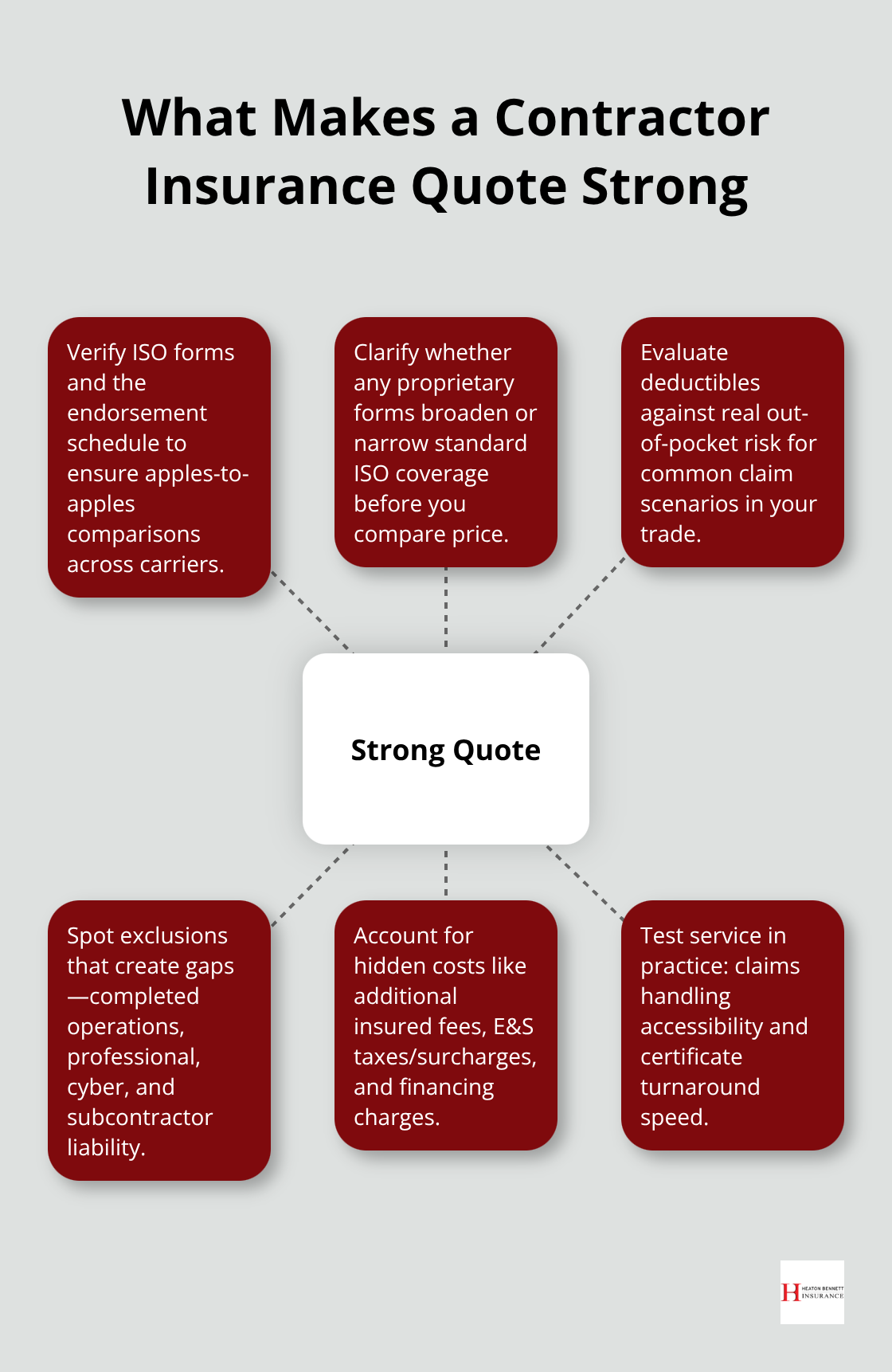

Verify Coverage Forms and Standards

ISO standard forms (identified by prefixes like CG for general liability or CP for commercial property) make apples-to-apples comparison possible, so always verify the form numbers in each quote’s endorsement schedule. If a quote uses proprietary forms instead, ask your broker to confirm whether those forms actually broaden or narrow the standard ISO coverage. This step prevents you from comparing policies that look identical but offer different protections.

Calculate Deductible Impact

Deductibles matter as much as premiums do-a $500 deductible saves money upfront but increases your out-of-pocket exposure on every claim, while a $2,500 deductible might cost more annually but protects you from frequent small losses. Compare multiple insurance carriers to see how deductible choices affect your total cost, since premiums can vary significantly for identical coverage levels. Coastal contractors face catastrophe deductibles (wind, earthquake) that can jump to 5–10% of property value, turning a $50,000 building loss into a $15,000 out-of-pocket expense.

Identify Exclusions That Create Gaps

Read the exclusions section carefully-completed operations coverage is frequently excluded from standard general liability policies, which means claims arising after project completion (like water damage from faulty plumbing) may not be covered at all. Professional liability and cyber liability are separate purchases with their own exclusions; if your contract requires both and you skip cyber, you’ve created a gap that no amount of premium savings will fix. Contractors with subcontractors need to verify how each quote handles subcontractor liability-many policies include CG2294 exclusions that remove coverage for work performed by subs, forcing you to add endorsements or require subs to carry you as additional insured.

Account for Hidden Costs and Real-World Scenarios

The cost of adding an additional insured varies widely; some providers offer it free while others charge $50–$200 per endorsement, so factor these administrative costs into your total comparison. When you receive quotes, ask each provider how they would respond to a specific claim scenario relevant to your trade: a slip-and-fall in your office, faulty workmanship on a completed project, or a data breach if you handle client information. The answer reveals whether the coverage actually applies in the situations that matter to your business. Non-admitted (E&S) policies may quote lower but add hidden taxes, surcharges, and longer underwriting timelines-sometimes 4–6 weeks versus 24 hours with admitted carriers. Request the total cost including all fees, not just the base premium, so you’re comparing the actual out-of-pocket amount. Financing costs add up too: if you pay monthly with interest rates of 6–18%, that premium difference shrinks or disappears entirely. Experience modification (MOD) for workers’ compensation is the biggest long-term lever you control-a contractor with a poor safety record might pay 20–30% more in premiums than a competitor with identical payroll, making loss prevention far cheaper than shopping for a lower rate.

With the real costs and coverage details in front of you, you’re ready to compare multiple providers side by side and spot which quotes actually protect your business.

How to Compare Multiple Providers

Request Quotes from At Least Three Carriers

Start by requesting quotes from at least three carriers, not two. The difference between a $2,000 annual premium and a $3,500 premium on identical coverage might signal differences in how each carrier underwrites risk or pays claims. Top carriers frequently underwriting contractor coverage include The Hartford, Travelers, Chubb, Liberty Mutual, Acuity, Hanover, Hiscox, and AmTrust. Request quotes from carriers with different underwriting philosophies-one that specializes in your trade, one that’s a generalist, and one that focuses on small operations. When you submit applications, compare policies properly by including the same project details, payroll figures, and claims history for each carrier so the quotes are genuinely comparable.

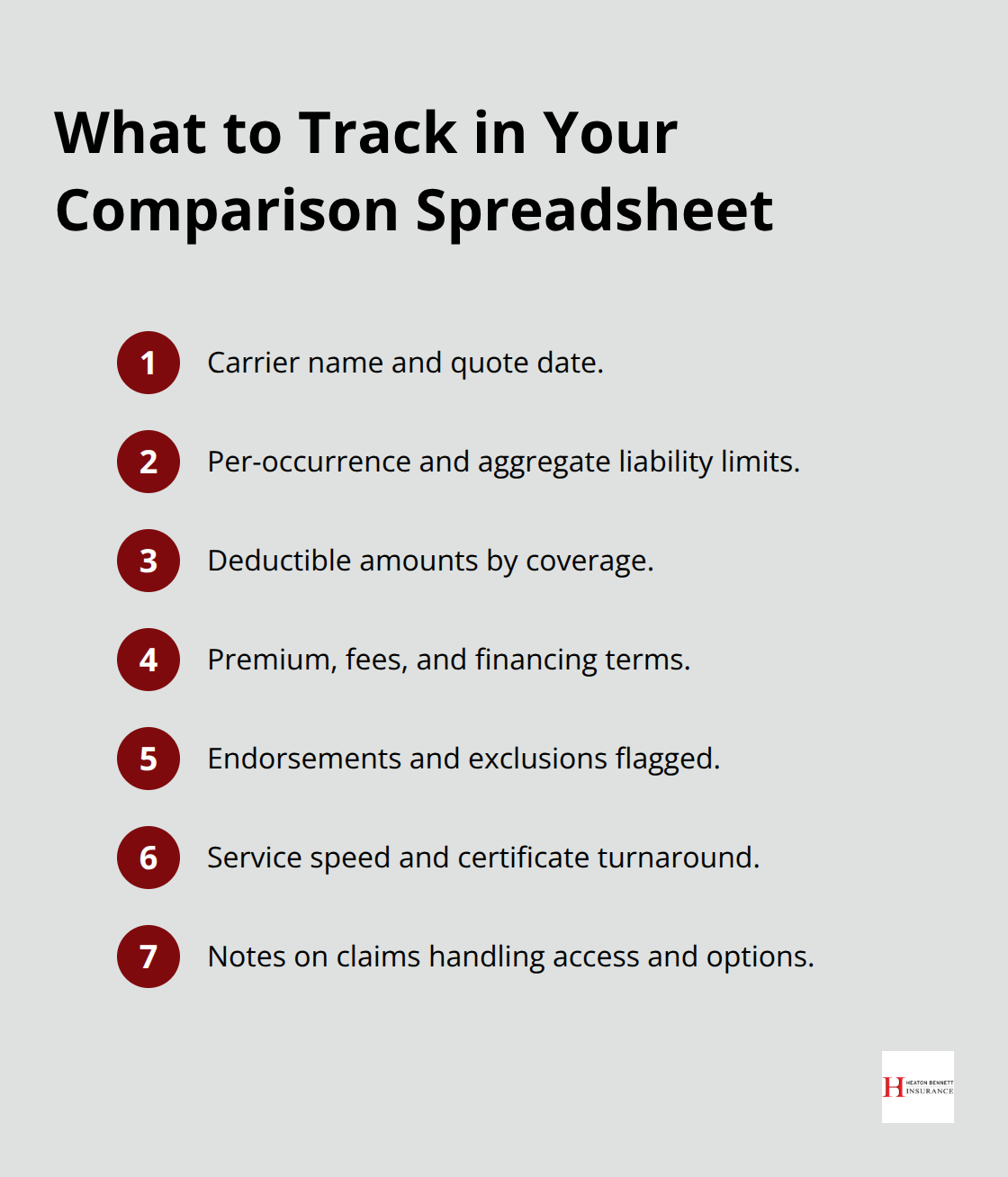

Many carriers now offer online quotes within minutes, but don’t rush through the application. Incomplete information leads to revised quotes later, wasting time and making side-by-side comparison impossible. Create a spreadsheet with each carrier’s name, the quote date, coverage limits (per-occurrence and aggregate), deductible amounts, premium, and any endorsements or exclusions flagged during the application. This forces you to organize details instead of relying on memory or scattered emails.

Calculate Net Cost, Not Just Premium

Once quotes arrive, resist the urge to pick the lowest number. Instead, calculate the net cost difference between the cheapest quote and a higher-priced quote, then estimate how many claim-free years it would take for premium savings to offset the extra protection you’d gain. A contractor paying $3,200 annually for a policy with completed operations coverage and a $500,000 aggregate limit faces less risk than one paying $2,400 for a policy without completed operations and a $250,000 aggregate. If completed operations claims average one incident every five years in your trade, the extra $800 per year is cheap insurance against a gap that could cost $50,000 to defend.

Ask each carrier’s agent directly which quote they would choose and why-their answer reveals whether they prioritize your protection or just close the sale. If you distrust the recommendation, that’s a signal to find a different broker.

Evaluate Claims Support and Service Speed

When comparing customer service, call the claims department before you buy, not after you need them. Ask how they handle a specific claim scenario relevant to your work and whether they offer online claim filing or require phone calls and paperwork. Carriers that provide instant certificate issuance through online portals speed up your ability to meet client contract requirements, while others may take 24–48 hours. For contractors managing multiple projects with different clients, fast certificate turnaround directly impacts your cash flow and project start dates.

Check complaint ratios through the National Association of Insurance Commissioners, which tracks complaints relative to market share-a ratio above 1.0 means more complaints than expected, signaling potential service issues.

Assess Long-Term Cost Reduction Opportunities

Ask each carrier about their experience modification (MOD) tracking and loss prevention tools if workers’ compensation is part of your quote. Some carriers offer safety training discounts or return-to-work programs that can reduce your MOD by 10–20% over time, making the initial premium irrelevant compared to long-term savings potential. A contractor with a poor safety record might pay 20–30% more in premiums than a competitor with identical payroll, so loss prevention becomes far cheaper than shopping for a lower rate.

These comparisons reveal which carrier truly understands your trade and positions you to make decisions based on protection, not just price. The next step is identifying the mistakes that derail most contractors during this process.

Common Mistakes When Comparing Contractor Insurance Quotes

Price Alone Destroys Your Protection

Most contractors sabotage their own comparison process by fixating on the premium number and ignoring what actually matters. The cheapest quote often comes from a carrier that either underprices risk upfront and denies claims later, or strips out coverages you’ll desperately need. Insurance profit margins run roughly 2% of total premium, which explains why some providers quote substantially lower prices than others-they’re either accepting higher risk, using different underwriting standards, or narrowing coverage through exclusions.

A $1,500 annual premium that excludes completed operations or limits your aggregate to $250,000 isn’t a deal; it’s a trap. Contractors who compare only the headline number miss that a $2,000 quote with a $500 deductible and full coverage costs far less out-of-pocket than a $1,400 quote with a $2,500 deductible and missing endorsements. The real cost emerges when you file a claim and discover the coverage doesn’t apply.

One contractor saved $600 annually on premium but then faced a $15,000 out-of-pocket cost on a slip-and-fall claim because they skipped the additional insured endorsement their client required. Another picked a non-admitted carrier to save money, then waited six weeks for underwriting while their project start date slipped. Calculate total cost including deductibles, endorsements, financing interest (if paying monthly at 6–18%), and administrative fees-not just the base premium.

Hidden Gaps in Coverage Destroy Claims

The second major error is failing to read the actual policy language before you commit. Contractors receive quotes, see a number that fits their budget, and sign without verifying what’s covered and what’s excluded. Completed operations coverage is frequently excluded from standard general liability, which means claims arising after project completion-water damage from faulty plumbing, structural failures from poor framing-fall outside your protection entirely.

Professional liability and cyber liability don’t automatically come with general liability; they’re separate purchases with separate exclusions. Subcontractor liability exclusions (CG2294) are common, meaning work performed by subs may not be covered unless you add endorsements or require subs to carry you as additional insured. Read the insuring agreement and subsequent exclusions to understand what actually is and isn’t covered in practice for your operations.

Create a checklist of coverages your client contracts require, then verify each quote provides them before comparing prices. If a client demands $2 million in liability limits with additional insured status and your quote only goes to $1 million without that endorsement, the price is irrelevant. Don’t rely on the agent’s summary; read the endorsement schedule yourself and ask the agent to explain any form numbers, exclusions, or amendments that seem unclear.

Deductibles and Aggregate Limits Shift Your Real Cost

Ask yourself whether the savings justify the gaps. If you’re paying $3,500 instead of $2,800 but gaining completed operations coverage and a $1 million aggregate instead of $500,000, that extra $700 annually protects you against losses that could exceed $50,000. Coastal contractors face catastrophe deductibles (wind, earthquake) that can jump to 5–10% of property value, turning a $50,000 building loss into a $15,000 out-of-pocket expense.

A $500 deductible saves money upfront but increases your out-of-pocket exposure on every claim, while a $2,500 deductible might cost more annually but protects you from frequent small losses. Compare how deductible choices affect your total cost across multiple carriers, since premiums can vary significantly for identical coverage levels. The time you spend verifying these details directly reduces the risk of an expensive claim denial later.

Final Thoughts

Comparing contractor insurance quotes effectively comes down to one principle: protect your business first, then optimize the cost. The contractors who waste money chase the lowest premium without understanding what they actually buy, while those who succeed organize their quotes in a spreadsheet, verify coverage forms against ISO standards, and calculate deductibles plus aggregate limits into their total cost. These steps take time, but they prevent the expensive claim denials that cost far more than any premium difference.

Gather quotes from at least three carriers with different underwriting approaches, then ask each agent which quote they would personally choose and why. Call the claims department before you buy to verify they handle incidents relevant to your work quickly and fairly, and check complaint ratios through the National Association of Insurance Commissioners to spot carriers with service problems. Calculate the net cost difference between the cheapest option and higher-priced alternatives to determine whether the extra protection justifies the premium (including deductibles, endorsements, and financing interest if you pay monthly).

We at Heaton Bennett Insurance have access to multiple carriers and understand the specific risks contractors face across different trades. Our team handles the complexity of endorsements, additional insured requirements, and trade-specific exclusions so you focus on running your operation. Contact Heaton Bennett Insurance to discuss your contractor insurance needs and receive quotes that protect your business without leaving you exposed.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.