Construction Contractor Insurance Austin: What Builders Need to Know

Construction contractors in Austin face real financial risks on every job site. One accident, one lawsuit, or one equipment loss can threaten your entire business.

At Heaton Bennett Insurance, we’ve seen contractors lose everything because they didn’t have the right construction contractor insurance in Austin. This guide walks you through the coverage types you actually need and the gaps most builders miss.

The Three Core Coverages Every Austin Contractor Must Have

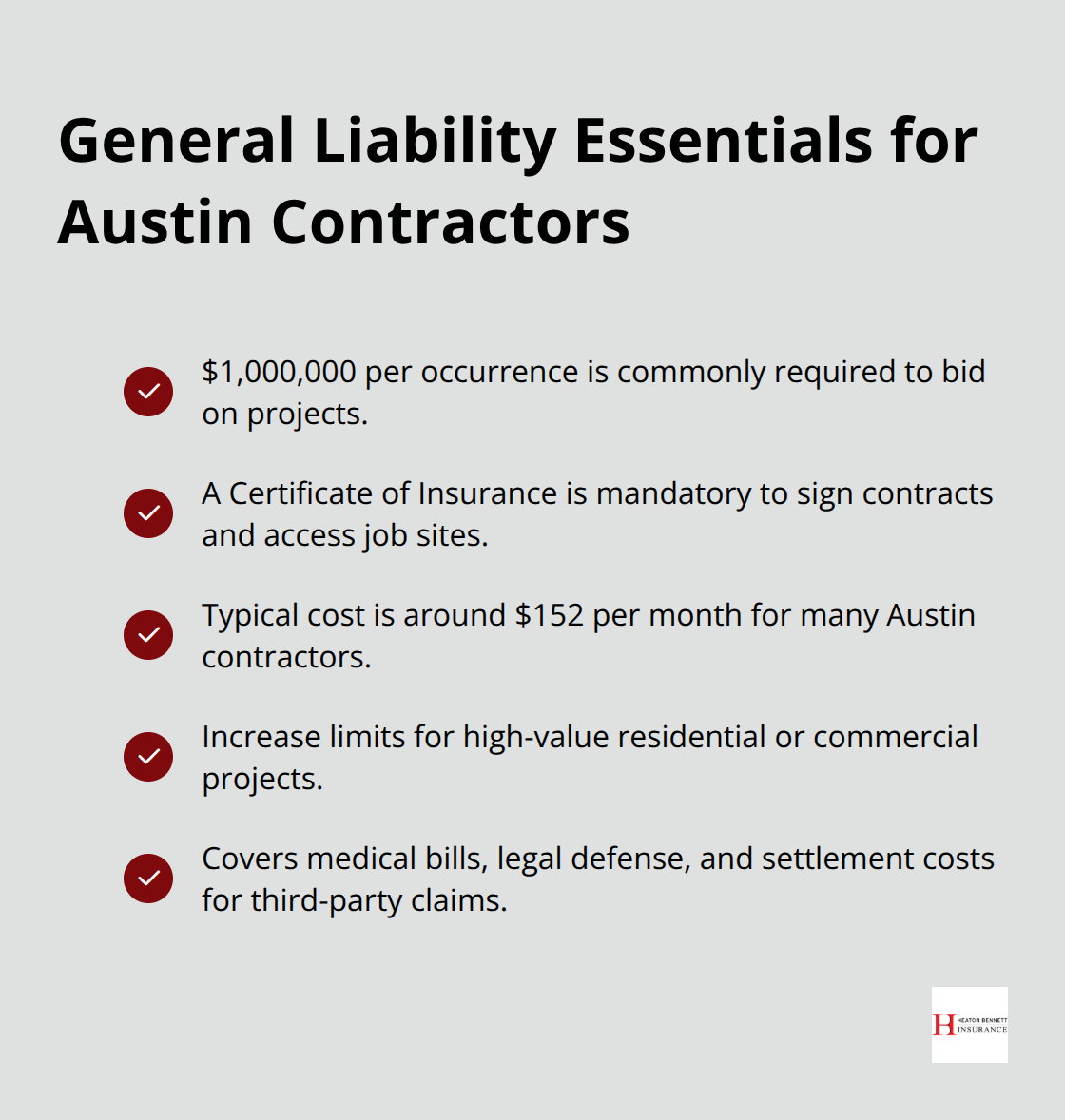

General liability insurance protects you when someone gets hurt or property gets damaged because of your work. If a subcontractor falls off scaffolding on your job site or your crew accidentally damages a client’s existing structure, general liability covers the medical bills, legal fees, and settlement costs. In Austin, most project owners and general contractors require a minimum of $1,000,000 per occurrence before you can even bid on work. Without this coverage, you cannot obtain a Certificate of Insurance, which means you cannot sign contracts or access job sites. The cost runs around $152 per month for most Austin contractors, according to industry data, but this varies based on your project type, claims history, and revenue.

If you work on high-value residential or commercial projects, you should push your limits higher because a single catastrophic injury can exceed standard coverage.

Workers’ Compensation Protects You From Direct Lawsuits

Workers’ compensation is not mandatory in Texas for private employers, but this is where contractors make a fatal mistake. If an employee gets injured and you lack coverage, they can sue you directly for unlimited damages. The medical costs alone for a serious construction injury run into six figures fast, and you become personally liable. Workers’ compensation typically costs around $306 per month in Austin and covers medical expenses, rehabilitation, and lost wages for injured employees. If you have no employees but operate as a sole proprietor, a Ghost Policy lets you claim coverage for yourself at minimal cost, which is essential if you ever bring on help or work on projects that mandate proof of coverage. Many Austin contractors skip this because they think small crews don’t need it, but a single serious injury will bankrupt a business without protection.

Tools and Equipment Need Separate Protection

Tools disappear. Theft from job sites in Austin happens constantly, and your general liability policy will not reimburse you for stolen equipment. Contractors Equipment Insurance covers portable tools, power equipment, and machinery both at the job site and in transit. A single high-end power drill, compressor, or saw costs $500 to $2,000, and most contractors operate with $15,000 to $50,000 in equipment on site. If thieves hit your job, you lose productivity, delay timelines, and spend money replacing gear you already paid for. This coverage typically reimburses theft, weather damage, and accidental loss, making it essential for keeping projects moving and protecting your investment in tools that make your business run.

What Happens When You Skip These Three Coverages

Contractors who operate without these three core policies face exposure that extends far beyond a single bad job. A lawsuit from a third-party injury can drain your business bank account within months. An employee injury without workers’ compensation can force you to liquidate assets to cover medical bills and lost wages. Equipment theft without proper coverage means you absorb the full replacement cost while your crew sits idle waiting for new tools. The combination of these three gaps creates a perfect storm that destroys most small to mid-sized construction businesses in Austin. Your next step involves identifying which coverage gaps exist in your current setup and which specialized policies your specific projects demand.

Why Austin Contractors Face Rising Insurance Demands

Austin’s Construction Boom Raises the Bar for Coverage

Austin’s construction market has expanded significantly over the past decade, with the city’s population growing faster than the national average and residential construction permits increasing year over year. This growth creates more projects, higher competition, and stricter requirements from project owners who demand proof of coverage before any work starts. The construction industry in Texas accounts for over 600,000 jobs according to state labor data, and Austin represents one of the fastest-growing markets in the state. More job sites mean more opportunities for accidents, equipment theft, and property damage claims. Project owners now verify insurance status as a standard part of due diligence, and they eliminate contractors who cannot produce a valid Certificate of Insurance immediately. This shift has forced contractors to move beyond basic coverage and maintain policies that actually protect their operations. Courts and insurance carriers now expect contractors to carry adequate limits that match project value and complexity, making the financial consequences of being uninsured or underinsured far more severe than in previous years.

Workers’ Compensation: The Coverage Contractors Skip at Their Peril

Texas law treats workers’ compensation differently than most states-it is not mandatory for private employers, which creates a dangerous trap for Austin contractors. Many builders mistakenly believe that because coverage is optional, they can skip it and pocket the savings. This decision has destroyed countless businesses. If an employee suffers a serious injury and you lack workers’ compensation coverage, that worker can file a direct lawsuit against you personally for unlimited damages, medical costs, lost wages, and pain and suffering. Construction injuries regularly result in six-figure settlements, and without workers’ compensation protection, your personal assets become the target. A single spinal injury or permanent disability claim can exceed $500,000 in total costs, and you absorb every dollar. Workers’ compensation typically costs around $306 monthly for Austin contractors according to industry benchmarks, which represents genuine insurance against financial catastrophe. The alternative-self-insuring by hoping nothing goes wrong-is a bet most contractors cannot afford to lose. Major construction firms and municipalities increasingly require proof of workers’ compensation as a condition of contract. Government projects in Austin mandate it, and many private developers now demand it as well. Skipping this coverage eliminates entire categories of work from your business pipeline.

Lawsuits Arrive Faster Than You Expect

A property damage claim from faulty workmanship, a bodily injury lawsuit from a job site accident, or a third-party claim from adjacent property damage can arrive within weeks of the incident. Legal defense costs alone run $10,000 to $50,000 before a case even reaches settlement discussions. General liability insurance covers these legal fees, court costs, and settlement amounts up to your policy limits, which means you stay in business rather than spending months fighting claims out of pocket. Without adequate coverage limits, a single catastrophic claim exceeds your protection, leaving you personally liable for the overage. High-value Austin projects-downtown renovations, commercial builds, luxury residential work-create exposure that standard $1,000,000 limits may not cover. Contractors working on projects valued above $5,000,000 should seriously consider excess liability policies that add an additional $2,000,000 to $5,000,000 in protection. The cost of excess coverage runs roughly $300 to $600 annually per million in additional limits, which is trivial compared to the risk. Contractors who operate without this layered approach essentially gamble that no catastrophic incident will occur on their watch, and statistics show this gamble fails for hundreds of Austin builders every year. The next section examines the specific insurance gaps that leave contractors most vulnerable to financial ruin.

Where Contractors Lose Coverage and Expose Themselves to Risk

Coverage Limits That No Longer Match Your Projects

Most Austin contractors operate with coverage limits that made sense five years ago but no longer match the projects they bid on today. A $1,000,000 general liability limit sounds substantial until you price a commercial renovation in downtown Austin or a multi-unit residential project valued at $8,000,000 or higher. A single catastrophic injury or property damage claim on a high-value project can exceed your standard limits within hours, leaving you personally liable for everything above the policy cap.

Contractors working on projects above $3,000,000 regularly encounter clients who demand $2,000,000 or $5,000,000 in coverage before signing contracts. The cost difference between $1,000,000 and $2,000,000 in limits runs roughly $40 to $80 monthly according to industry benchmarks, yet contractors skip this upgrade to save money they later lose in a single claim. Excess liability policies add another $1,000,000 to $5,000,000 in protection for $300 to $600 annually, making layered coverage affordable for any serious operation. Your coverage limits should scale with your project values, not stay frozen at whatever you purchased when you started the business.

Subcontractor Liability Creates Hidden Exposure

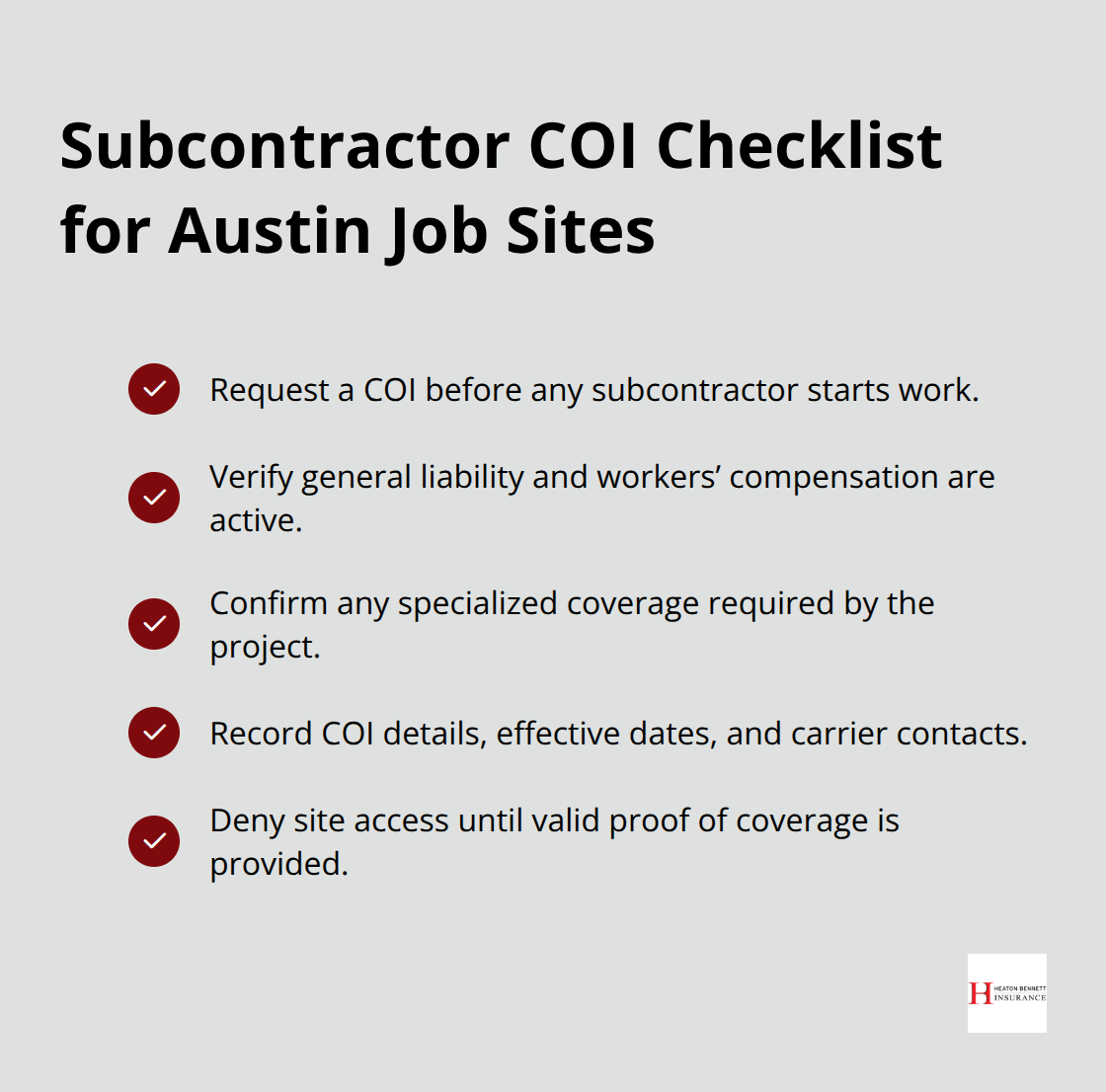

Subcontractors represent another massive gap most general contractors fail to address properly. You cannot simply assume your subcontractor carries adequate coverage or that their policy protects you if something goes wrong on the job site. Texas law holds you responsible for subcontractor negligence, meaning you absorb liability even when the sub caused the damage.

Before any subcontractor sets foot on your job site, you must request a Certificate of Insurance proving they carry general liability, workers’ compensation, and any specialized coverage your project requires. Many Austin contractors skip this step entirely and discover the gap only after an incident occurs. If a sub causes $500,000 in property damage and lacks coverage, you file a claim under your policy, your coverage pays out, and your premiums increase for years.

A documented file with each subcontractor’s COI, policy dates, and carrier contact information takes thirty minutes to assemble but prevents catastrophic exposure.

Specialized Construction Types Demand Unique Coverage

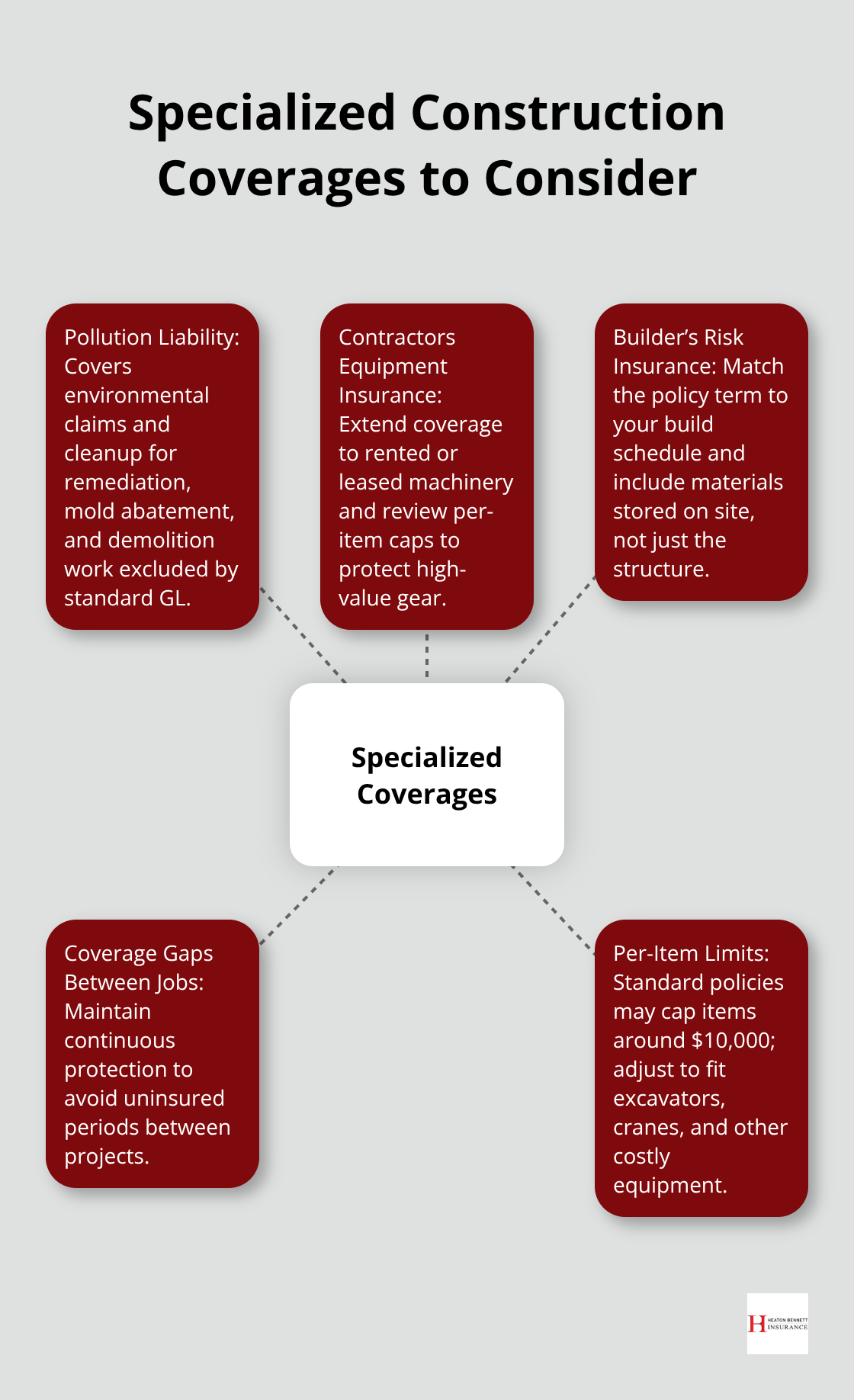

Specialized construction types demand coverage most contractors overlook completely. If you perform environmental remediation, mold abatement, or demolition work, standard general liability policies exclude these activities. Pollution liability coverage specifically addresses environmental claims and cleanup costs, protecting you from six-figure exposures that arise from jobsite contaminants.

Contractors Equipment Insurance must cover your specific equipment types, including rented or leased machinery, because standard policies often cap coverage at $10,000 per item. A single excavator or crane rental can exceed this limit within days, leaving you unprotected for loss or damage. Builder’s Risk Insurance must match your project timeline and include coverage for materials stored on site, not just the structure under construction. A three-month project requires three months of coverage, yet contractors frequently purchase twelve-month policies or miss coverage gaps between jobs.

Finding the Right Coverage for Your Operation

An independent insurance agent who understands Austin’s construction market helps you match coverage to actual project risk rather than guessing at standard limits that no longer fit your operation. At Heaton Bennett Insurance, we work with multiple carriers to provide tailored solutions that align with your specific projects and equipment needs. This approach ensures you carry the right protection without overpaying for unnecessary coverage or leaving dangerous gaps in your policies.

Final Thoughts

Construction contractor insurance in Austin protects your business from the financial devastation that follows a single accident, lawsuit, or equipment loss. The coverage types we’ve outlined-general liability, workers’ compensation, tools and equipment protection, and specialized policies for your project type-form the foundation of a sustainable operation. Without these protections layered together, you expose yourself to unlimited personal liability that can destroy everything you’ve built.

Getting the right coverage means matching your policies to the actual projects you bid on, not relying on generic limits that worked five years ago. A $1,000,000 general liability policy serves small residential jobs but leaves you dangerously exposed on commercial projects valued above $3,000,000. Your coverage limits should scale with project value, and excess liability policies provide affordable additional protection for high-risk work (roughly $300 to $600 annually per million in additional limits).

The next step involves reviewing your current policies against your actual project pipeline and identifying gaps before they become claims. Request Certificates of Insurance from every subcontractor before they start work, document those COIs in a file, and verify coverage dates match your project timeline. We at Heaton Bennett Insurance work with multiple carriers to provide tailored solutions that align with your specific projects and equipment needs-contact us to review your current coverage and identify the gaps that could threaten your business on the next job.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.