Subcontractor Insurance: Why It Matters

Subcontractor insurance isn’t optional-it’s a business necessity. Without proper coverage, you’re exposed to legal liability, job site accidents, and financial losses that could shut down your operations.

At Heaton Bennett Insurance, we’ve seen too many subcontractors operate without adequate protection. The right insurance policy protects your business, your employees, and your clients.

Why Subcontractors Must Have Insurance

State licensing boards across the country require general liability and workers’ compensation coverage before you can legally operate in most trades. In Texas and most other states, workers’ compensation is mandatory if you have employees, with the only exception being Texas, where it remains optional but heavily recommended. General contractors won’t hire you without proof of insurance, and many won’t even let you on job sites without a certificate of insurance showing adequate coverage. The financial exposure is real: a single on-site injury costs thousands in medical expenses and lost wages, and property damage claims can reach tens of thousands. Without coverage, you’re personally liable for these costs, which can drain your business account and potentially force you into bankruptcy. One accident without insurance can end your entire operation.

Your Legal Standing in the Marketplace

General contractors actively verify insurance before awarding contracts, and they require you to name them as additional insured on your general liability policy. This protects their project and reduces their own risk exposure. If you show up without proof of insurance, you lose the bid immediately. Contractors also use your insurance status as a credibility marker-it signals that you’re professional, financially stable, and serious about your business. On high-risk projects like electrical, plumbing, or HVAC work, insurance isn’t just preferred; it’s contractually mandatory. The 2025 Dodge ROI Report highlights that properly insured subcontractors win more contracts and command better rates than uninsured competitors.

Your insurance also protects you from liability claims: if a worker gets injured or a client’s property is damaged, your coverage pays for defense costs and settlements, keeping your business intact.

Tools, Equipment, and On-Site Losses

Tools and equipment floaters protect your expensive gear across multiple job sites from theft, loss, or damage. A single theft costs thousands, and without coverage, that loss comes directly out of your pocket. Commercial auto insurance stands separate from your personal policy and covers vehicles used for work, including rental vehicles and towing. Personal auto policies explicitly exclude business use, leaving you exposed if an accident happens while traveling to a job. If you work with a general contractor, confirm whether you’re listed as additional insured on their policy-most GC policies don’t cover your tools, vehicles, or equipment, only their liability exposure. Understanding these gaps in coverage helps you identify what protection you actually need for your operation.

What Insurance Types Do Subcontractors Actually Need

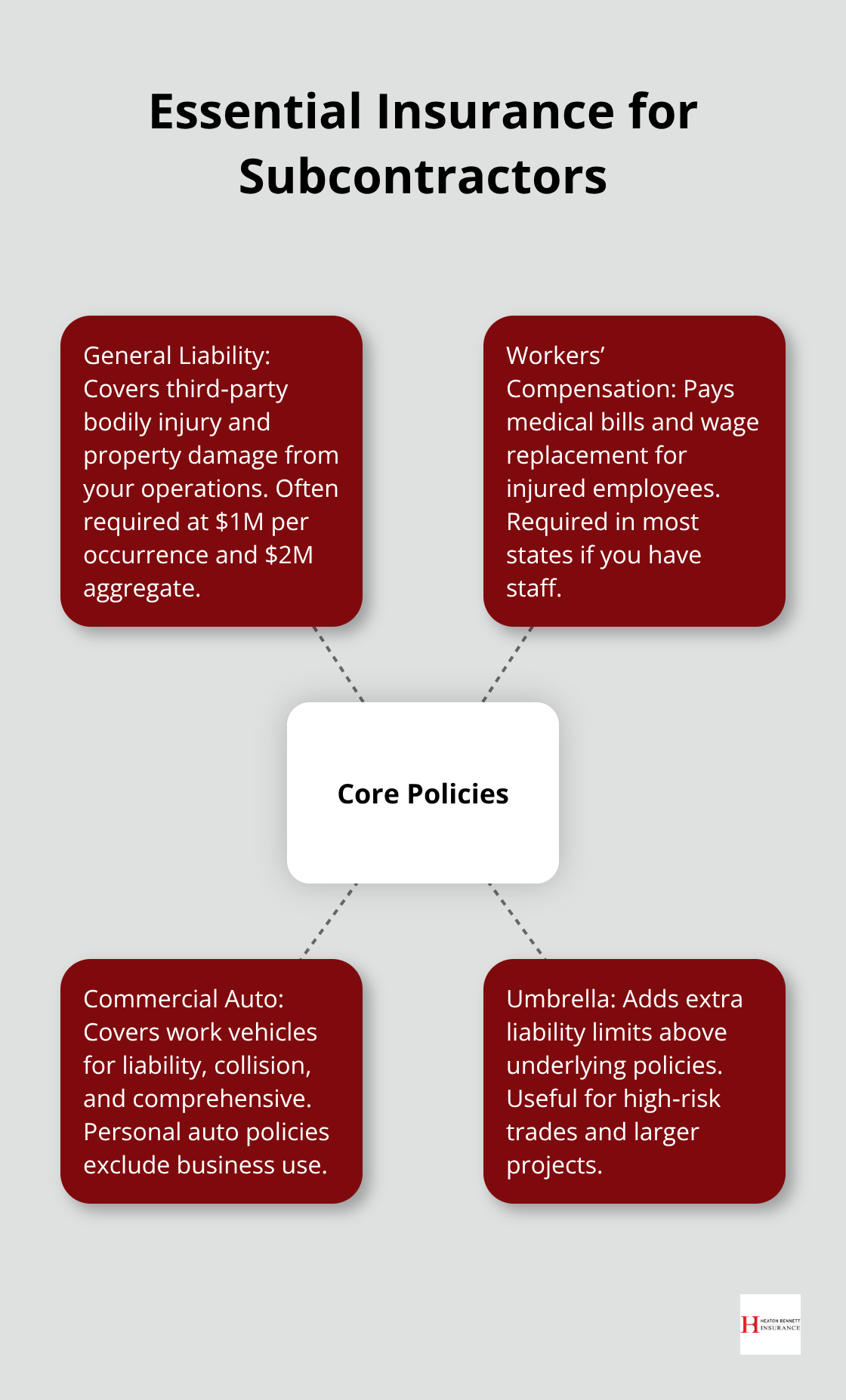

General Liability: Your Foundation

General liability insurance forms your foundation, and it’s non-negotiable. This policy covers bodily injury and property damage that occur while you perform work-the two most common claims on job sites. Standard limits run at $1 million per occurrence and $2 million aggregate, which is what most general contractors require before they hire you. The cost varies by trade and claims history, but electricians and plumbers typically pay between $400 and $1,200 annually for basic coverage.

Without this policy, a single incident where someone gets hurt or property is damaged leaves you personally responsible for medical bills, legal defense, and settlements that can easily exceed $50,000.

General contractors also require you to add them as additional insured on your policy, which means their name appears on your certificate of insurance. This protects them if a claim arises from your work, and it’s a deal-breaker if you don’t comply. You must secure this policy first-everything else builds around it. Comparing your contractor policy options helps ensure you select coverage that protects your business from liability, property damage, and worker injuries.

Workers’ Compensation: Protecting Your Team

Workers’ compensation insurance is legally required in every state except Texas if you have employees, and Texas heavily recommends it even though it’s optional. This coverage pays medical expenses, rehabilitation costs, and partial wage replacement when an employee gets injured on the job. The rates depend on your number of employees, job classification, past claims, and industry risk level. A roofing company pays significantly more per employee than a general contractor’s office staff because the injury risk is higher.

If an employee is injured without this coverage, you face liability for all costs out of your own pocket, potential lawsuits, and fines from state labor boards. The financial and legal consequences can devastate your operation, making this coverage essential for any subcontractor with staff.

Commercial Auto: Separate from Personal Coverage

Commercial auto insurance covers vehicles you own or rent for work purposes and is completely separate from your personal auto policy. Personal policies explicitly exclude business use, so if you drive a work vehicle and get into an accident, your personal insurer will deny the claim. Commercial auto covers bodily injury liability, property damage, collision, comprehensive, and medical payments.

If you own multiple vehicles or frequently rent for jobs, this becomes a substantial line item in your budget, but it’s unavoidable if you want to operate legally. One accident in an uninsured work vehicle can trigger catastrophic financial loss and expose you to lawsuits from injured parties. The next section examines how you actually select the right coverage limits and policy combinations for your specific operation.

How to Choose Your Coverage

Match Your Policies to Your Actual Job Site Risks

Start by identifying which types of work create the highest risk in your operation. If you’re an electrician, electrical fires and shock injuries drive your exposure, so general liability with $1 million per occurrence is non-negotiable, and you may need higher limits if you work on large commercial projects. If you run a plumbing crew with five employees, workers’ compensation becomes your second-largest expense after payroll, and your rate depends directly on your claims history and employee safety record. A roofing subcontractor faces different risks than a drywall installer, so your policy structure should match your actual job site exposures, not a generic template.

Pull your project contracts and review what general contractors explicitly require before you structure your coverage. Many GCs specify minimum limits like $2 million aggregate general liability or $500,000 per employee for workers’ comp, and failing to meet these requirements disqualifies you from bidding. Document these requirements in a spreadsheet and compare them against what you currently carry. If your existing policies fall short, you’re losing bids you could win.

Compare Quotes Across Multiple Carriers

Coverage costs vary significantly across insurers for identical protection. A $1 million general liability policy for a plumbing subcontractor ranges from $600 to $1,800 annually depending on the carrier, your loss history, and the underwriter’s appetite for your specific trade. Workers’ compensation costs swing even more dramatically based on your classification code and past claims, sometimes varying $200 to $500 per employee annually between carriers.

Contact three to five insurers directly and request quotes with identical coverage specifications so you compare options apples to apples, not marketing claims. An independent insurance agent can access multiple carriers simultaneously and negotiate rates on your behalf, often securing better pricing than you’d find shopping alone. We at Heaton Bennett Insurance in Austin work with multiple carriers to help you find the right fit for your business needs.

Leverage Discounts and Bundling Opportunities

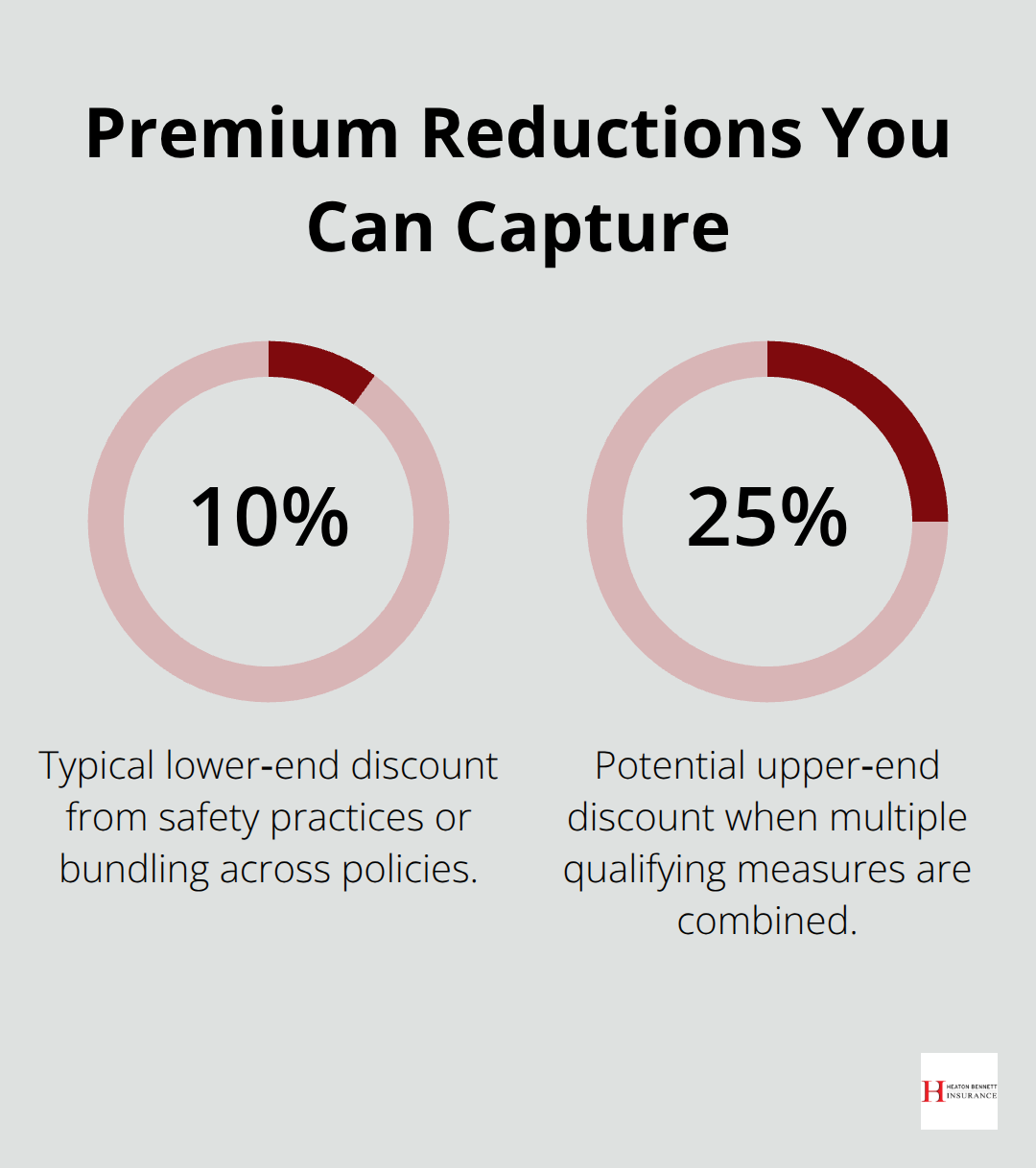

Ask each agent about available discounts: safety certifications, claims-free history, bundling policies, and installing loss-prevention equipment often reduce premiums by 10 to 25 percent. These reductions add up quickly across your entire insurance portfolio. Bundling your general liability, workers’ compensation, and commercial auto policies with one carrier frequently unlocks additional savings that individual policies don’t offer.

Add Umbrella Coverage for High-Risk Operations

Once you’ve selected your base policies, evaluate whether commercial umbrella coverage makes sense for your operation. Umbrella policies extend liability protection beyond your underlying policies in $1 million increments at relatively low cost, typically $200 to $500 annually per million dollars of additional coverage. For high-risk trades or large projects, adding $1 to $2 million in umbrella protection is affordable insurance against catastrophic claims that exceed your standard policy limits.

Final Thoughts

Subcontractor insurance protects your business from financial ruin and keeps you competitive in a market where general contractors demand proof of coverage before awarding contracts. Without it, a single accident drains your bank account, damages your reputation, and potentially forces you out of business. With proper coverage in place, you operate with confidence knowing that medical bills, property damage claims, and legal defense costs won’t destroy what you’ve built.

Start by reviewing your current policies against what general contractors actually require on their projects, then identify gaps in your coverage. General liability forms your foundation, workers’ compensation protects your employees and shields you from state penalties, and commercial auto covers vehicles you use for work. Once you’ve selected these core policies, evaluate whether umbrella coverage makes sense for your operation and explore discounts through bundling or safety certifications.

Contact multiple carriers, compare quotes with identical specifications, and work with an agent who understands construction trades and can negotiate on your behalf. We at Heaton Bennett Insurance in Austin work with multiple carriers to help you find tailored subcontractor insurance that matches your specific business risks and budget. Start your consultation at Heaton Bennett Insurance and secure the coverage your operation needs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.