Nonprofit Liability Coverage: Safeguarding Your Mission

Nonprofits operate with limited resources and big missions. One lawsuit or accident can drain your budget and distract your team from the work that matters.

At Heaton Bennett Insurance, we’ve seen how the right nonprofit liability coverage protects organizations when things go wrong. This guide walks you through the risks you face, the coverage options available, and the gaps you need to fill.

What Liability Risks Keep Nonprofit Leaders Up at Night

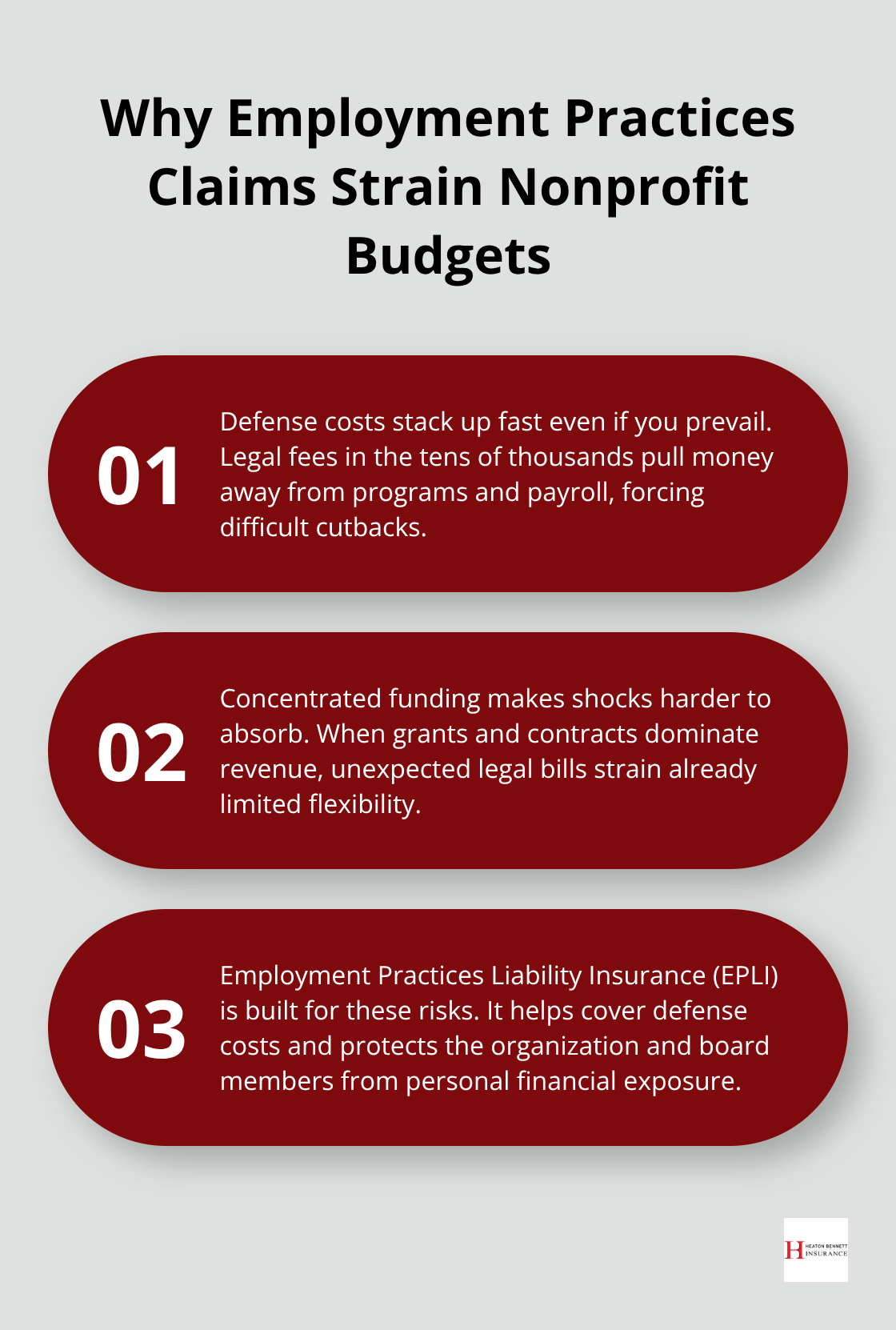

Employment Practices Claims Drain Your Budget

Employment practices claims hit nonprofits harder than most realize. When you terminate a staff member, deny a promotion, or fail to accommodate a disability, you face allegations of wrongful termination, discrimination, or retaliation. These claims cost money to defend even when you win. A single employment lawsuit runs $50,000 to $150,000 in legal fees alone, draining resources that should fund your mission. The Urban Institute reports that about two-thirds of nonprofits receive at least one government grant or contract, which means your funding stays concentrated and less flexible when unexpected legal costs emerge. Employment Practices Liability Insurance covers these claims directly, protecting both your organization and your board members from personal financial exposure.

Without this coverage, you pay legal bills out of pocket while your programs suffer.

Directors and Officers Face Personal Liability

Board members and executives face personal liability for decisions made in their official capacity. Directors and Officers liability claims arise from alleged mismanagement of funds, breach of fiduciary duty, or poor governance decisions. A former volunteer might sue the board for how grant money was spent. A donor could claim the executive director misused restricted funds. These cases expose individual board members to personal financial risk, which deters qualified leaders from serving your organization. D&O Insurance protects the organization and shields directors, officers, and employees from personal liability for these alleged wrongful acts. Without it, talented people avoid board roles because they fear personal bankruptcy.

General Liability and Property Damage Claims Happen Constantly

General liability and property damage claims occur throughout nonprofit operations. Someone slips at your fundraiser and breaks their leg. A volunteer causes property damage during a community event. Your organization accidentally injures a client through service delivery. General liability covers bodily injury, property damage, and personal injury claims from third parties. Property insurance protects your buildings, equipment, and supplies from fire, theft, vandalism, and weather damage. These two coverages form the foundation of nonprofit protection. Rising litigation trends (including what industry experts call social inflation and nuclear verdicts) push liability costs higher. The Council of Insurance Agents and Brokers reported that as of Q4 2024, commercial property and casualty rates have risen for 29 consecutive quarters. This trend directly affects nonprofit premiums, making adequate coverage limits essential right now.

Why Coverage Gaps Matter Most

The risks you face today demand more than basic protection. Your organization needs coverage that matches the actual scope of your operations and the vulnerabilities your team encounters daily. Understanding what each policy covers-and what it doesn’t-separates organizations that recover from claims and those that face financial crisis. The next section explores the specific coverage options that address these liability risks head-on.

Building the Right Coverage Foundation

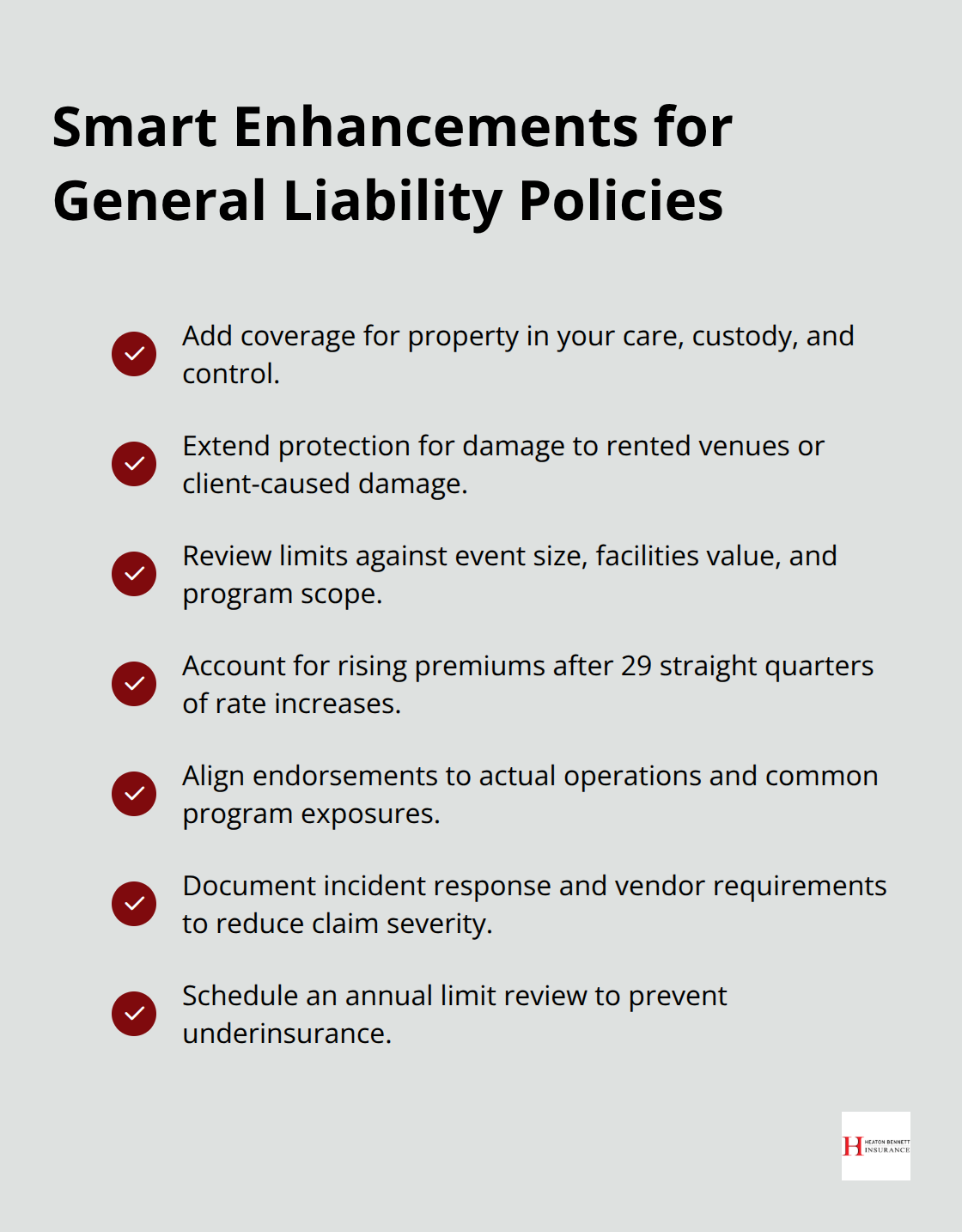

General Liability Policies Require Strategic Enhancement

General liability insurance forms the backbone of nonprofit protection, but the standard policy has limits that expose your organization to financial risk. A comprehensive general liability policy for nonprofits goes beyond basic third-party coverage by including endorsements that address gaps in standard commercial policies. The enhancement endorsement adds coverage for property in your care, custody, and control and for damage caused by clients to rented property-both common exposures nonprofits face during programs and events. Your coverage limits matter enormously right now. With commercial property and casualty rates rising for 29 consecutive quarters as of Q4 2024 according to the Council of Insurance Agents and Brokers, many nonprofits discover their existing limits no longer match their actual risk exposure. A small nonprofit carrying $1 million in general liability coverage may find that a serious injury at a community event triggers a lawsuit exceeding that limit.

Evaluate Your Coverage Limits Against Real Exposure

Review your current limits against your annual budget, your largest single event attendance, and the value of your facilities. If your organization operates multiple programs or serves vulnerable populations, higher limits become non-negotiable. This assessment prevents the financial devastation that occurs when a single claim exhausts your coverage and leaves your organization liable for the remainder.

Management Liability Protects Leadership and Operations

Management liability insurance addresses the employment, governance, and professional service risks that general liability ignores completely. This coverage bundles directors and officers liability, employment practices liability, and fiduciary liability into one package that protects your leadership team and organization from the financial devastation of employment claims, wrongful termination disputes, and governance failures. Employment practices claims alone cost $50,000 to $150,000 in legal defense even when you win. Management liability covers these defense costs and any settlements or judgments, allowing your organization to focus on mission work rather than depleting reserves for legal bills.

Abuse and Molestation Coverage Addresses Vulnerable Population Exposure

Abuse and molestation coverage addresses a specific exposure that general liability explicitly excludes. If your nonprofit works with children, elderly adults, or other vulnerable populations, you face exposure to allegations of sexual or physical abuse. A single credible allegation can destroy your organization’s reputation and trigger lawsuits that exceed $500,000 in defense and settlement costs. Standard general liability policies contain abuse exclusions precisely because insurers view this risk as too severe for standard coverage. Abuse and molestation insurance provides first-party coverage for your organization’s defense costs and third-party coverage for claims brought by affected individuals. This coverage becomes mandatory if you employ staff who have unsupervised contact with vulnerable populations or if your programs involve overnight stays, transportation, or one-on-one service delivery.

Identifying Coverage Gaps Requires Honest Assessment

Without abuse and molestation insurance, a single incident can bankrupt your organization. The coverage options outlined here form a strong foundation, but your specific programs and operations may reveal additional exposures that demand specialized protection. The next section examines the common gaps that leave nonprofits vulnerable even when they carry standard policies.

Common Gaps in Nonprofit Insurance Plans

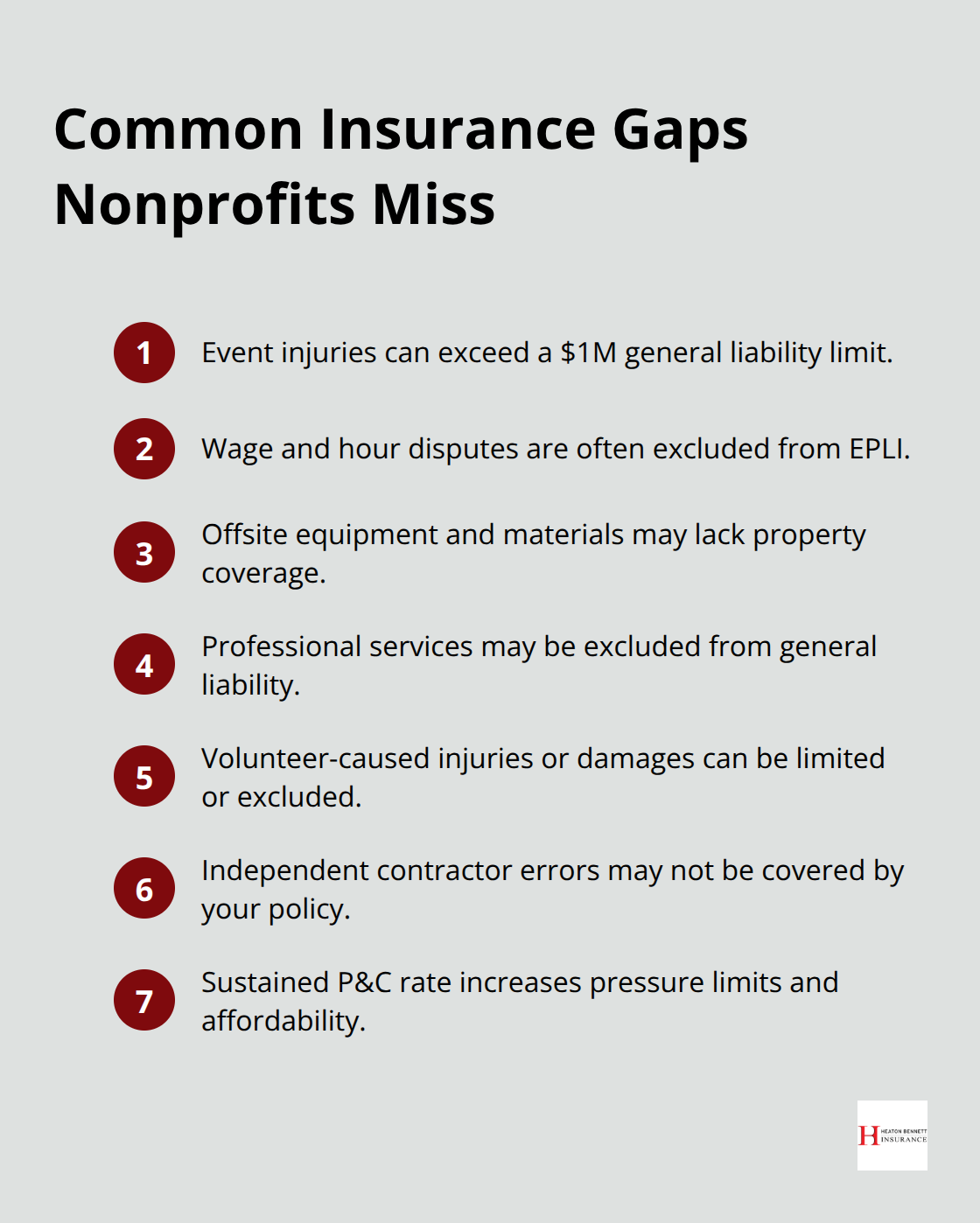

Most nonprofits discover gaps in their insurance plans only after a claim exposes them. The problem isn’t that these gaps are hidden-they’re written right into your policies. Your general liability coverage has a $1 million limit, but a serious injury claim at your largest annual event could reach $2 million. Your employment practices liability covers wrongful termination, but not wage and hour disputes that the Department of Labor increasingly pursues against nonprofits.

You carry property insurance for your main office building, but not for equipment stored at a volunteer’s home or materials staged at an event venue. These gaps exist because standard nonprofit policies assume standard operations. The moment your organization expands programs, adds facilities, or increases volunteer involvement, those standard policies become inadequate. As of Q4 2024, the Council of Insurance Agents and Brokers reported that commercial property and casualty rates have risen for 29 consecutive quarters. This sustained rate environment means nonprofits face harder choices: maintain inadequate limits to control costs, or invest in proper coverage.

Inadequate Coverage Limits Create Financial Exposure

Coverage limits represent the most dangerous gap in nonprofit insurance. A $1 million general liability limit sounds substantial until you face a catastrophic claim. If a participant in your youth program suffers permanent spinal injury during an activity, medical costs, lost wages, and pain and suffering claims routinely exceed $2 million. Your $1 million policy covers the first million dollars, and your organization absorbs the remaining $1 million from operating reserves or future fundraising. This scenario plays out regularly in nonprofit litigation. Pull your current policies and compare the actual coverage language against your organization’s real operations. List every program, every facility, every volunteer role, and every contractor relationship. Then ask your broker whether each item receives explicit coverage or sits in a policy gap waiting to become a claim.

Excluded Activities and Programs Leave You Vulnerable

Your organization faces exposure through excluded activities that don’t appear in your policy language until you need coverage. Does your general liability policy cover your nonprofit’s counseling services, medical advice, or professional guidance? Many standard policies exclude professional services entirely, leaving organizations that provide direct client services dangerously underprotected. If your nonprofit operates vehicles for client transportation, volunteers in your programs, or contractors who work unsupervised with vulnerable populations, your current policies likely contain gaps that create personal liability for board members.

Volunteer and Contractor Protection Gaps

Standard general liability policies often exclude volunteer actions or limit coverage for volunteer-caused injuries. If a volunteer causes property damage or injures someone during a nonprofit activity, your organization may lack coverage and the volunteer themselves becomes a liability target. Contractor coverage presents an identical problem. If you hire independent contractors for program delivery, grant writing, or specialized services, your general liability may not extend to their work. A contractor’s professional error that harms a client leaves your nonprofit financially exposed unless your policy explicitly covers contractor liability.

The gap between what you think you’re covered for and what your policy actually covers costs nonprofits thousands in unexpected out-of-pocket expenses annually. Your broker can help you identify these exposures and recommend coverage that matches your actual operations.

Final Thoughts

Nonprofit liability coverage protects your mission, your team, and your ability to serve your community when unexpected claims arrive. The coverage gaps outlined throughout this guide represent real financial exposure that grows every year as litigation costs rise and nonprofit operations become more complex. Your organization cannot afford to discover these gaps after a claim happens, and the sustained rise in commercial property and casualty rates over 29 consecutive quarters means the cost of waiting only increases.

Regular policy reviews separate organizations that stay protected from those that drift into inadequate coverage. Your nonprofit’s programs evolve, your facilities change, your volunteer base grows, and your board composition shifts-each of these changes creates new exposures that your existing policies may not address. An annual review with your insurance broker identifies these shifts before they become claims and prevents the financial devastation that follows when coverage fails at the moment you need it most.

We at Heaton Bennett Insurance understand that nonprofit leaders balance limited budgets with unlimited missions. Contact us to discuss your nonprofit’s insurance needs and build a protection strategy that lets your team focus on mission work instead of worrying about financial exposure.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.