Restaurant Equipment Coverage: Keeping Kitchens Running

A broken oven or failed refrigerator doesn’t just mean a repair bill-it means lost revenue, frustrated customers, and staff standing idle. Restaurant equipment failures happen without warning, and the costs add up fast.

Restaurant equipment coverage protects your kitchen’s most critical assets when breakdowns occur. We at Heaton Bennett Insurance help restaurant owners understand what’s covered, what it costs to go without protection, and how to choose the right policy for your operation.

What Equipment Breakdown Coverage Actually Includes

The Gap Between Property Insurance and Equipment Protection

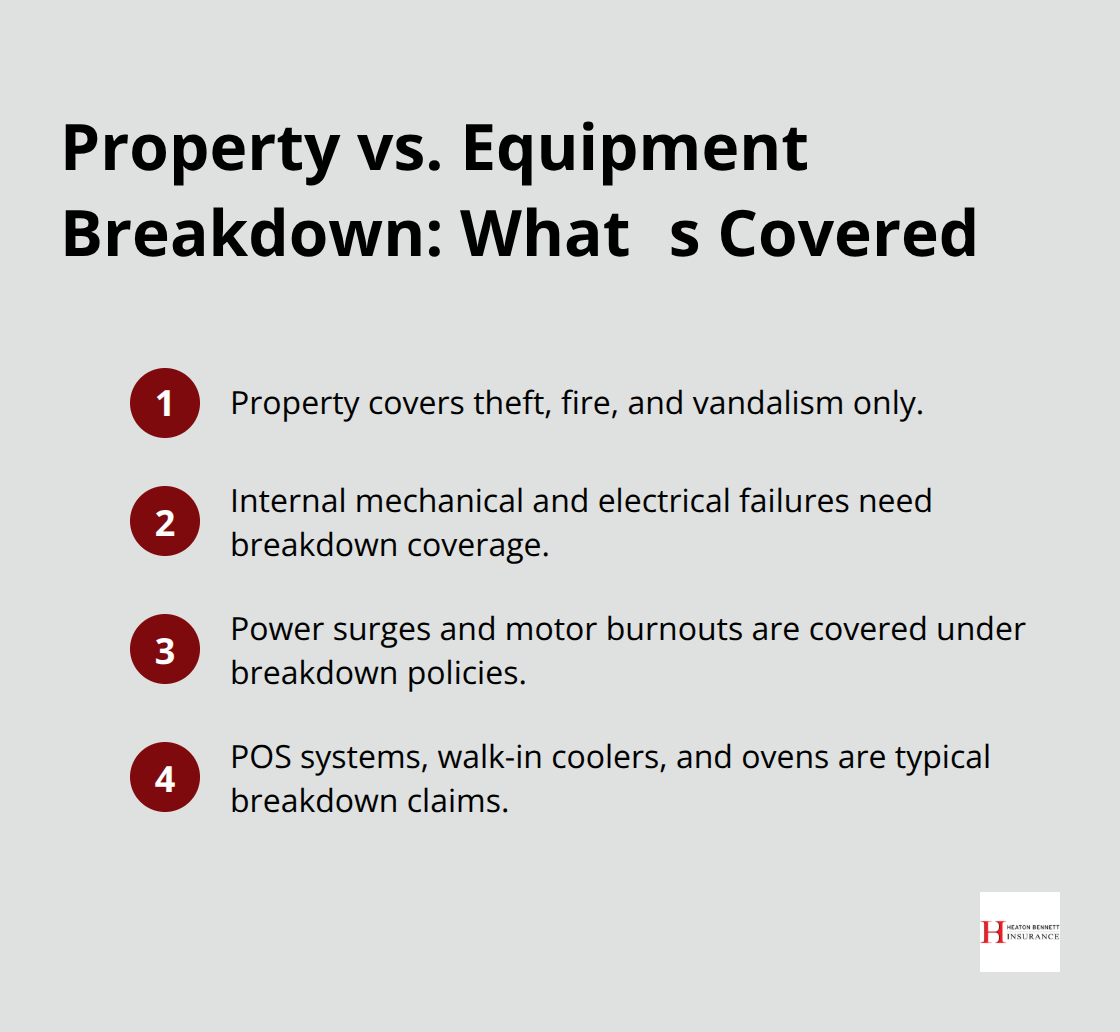

Restaurant equipment breakdown coverage protects against internal mechanical and electrical failures that your standard commercial property insurance won’t touch. Commercial property insurance covers theft, fire, and vandalism, but it stops there. When a power surge fries your point-of-sale system, when a compressor motor burns out in your walk-in cooler, or when an electrical short disables your convection oven, property coverage leaves you exposed. Equipment breakdown coverage fills that gap by paying for repairs or replacements when internal malfunctions occur.

What Your Coverage Actually Protects

The National Restaurant Association projects US foodservice sales to exceed $1 trillion in 2025, which means restaurants invest heavily in equipment to capture that revenue. Most kitchens carry between $40,000 and $200,000 in equipment value, making breakdown protection a financial necessity rather than an optional add-on. Coverage typically applies to boilers and pressurized equipment, HVAC systems, refrigeration units, food processing equipment, computers, point-of-sale devices, and security systems. Some policies even include business income coverage, which reimburses lost profits during downtime, and food spoilage coverage, which replaces perishable inventory destroyed after a breakdown. Without these protections, a single equipment failure can force temporary closure and erode customer loyalty.

Why Equipment Fails When You Need It Most

Equipment failures strike when you’re busiest. A failed dishwasher during dinner service means dishes pile up, staff falls behind, and customers wait longer. A refrigeration breakdown puts your entire inventory at risk and can trigger health code violations. Fryer thermostat failures, oven heating element burnouts, and mixer motor seizures happen regularly in high-volume kitchens because constant heat, mechanical stress, and grease buildup accelerate wear.

Understanding Limits, Deductibles, and Exclusions

Coverage limits matter significantly-you need enough protection to cover the actual replacement cost of your highest-value equipment. Deductibles typically range from $250 to $2,500, and choosing a higher deductible lowers your premium but increases your out-of-pocket expense when a claim occurs. Some carriers offer rush repair options that prioritize rapid technician dispatch, minimizing downtime on critical equipment. Understanding what your policy excludes is equally important: most coverage excludes breakdowns caused by neglect, improper maintenance, normal wear and tear, and unauthorized repairs. This means regular preventive maintenance isn’t optional-it’s a requirement to keep your coverage valid. You must purchase equipment breakdown insurance before a loss occurs; retroactive coverage doesn’t exist, so waiting until after a failure leaves you unprotected.

The specific equipment you operate and your kitchen’s age determine which coverage options make the most sense for your operation.

What Equipment Breakdowns Actually Cost Your Restaurant

The Price Tag of Common Kitchen Failures

Refrigeration failures top the list of expensive kitchen disasters. A walk-in cooler compressor burnout runs $3,000 to $8,000 in repairs, and that’s before you factor in the food spoilage. A single breakdown destroys $2,000 to $5,000 in perishable inventory within hours. Commercial dishwashers fail regularly in high-volume operations-spray arm clogs, pump malfunctions, and heating element failures cost $1,500 to $4,000 to repair. Convection ovens and ranges malfunction from thermostat failures, broken ignition systems, and damaged heating elements, with repairs ranging from $800 to $3,500 depending on severity. Fryer thermostat and heating element problems cost $1,200 to $2,800 to fix. Food processors, mixers, and steam tables round out the common failures, each carrying repair bills between $600 and $2,000.

The National Restaurant Association data shows kitchens carry $40,000 to $200,000 in total equipment value, meaning a single major breakdown represents a meaningful percentage of your equipment investment. Repair timelines stretch from 24 to 72 hours for parts ordering and technician availability, leaving your kitchen partially or fully non-operational during that window.

How Downtime Destroys Revenue

The revenue impact of equipment downtime dwarfs the repair cost itself. A full-service restaurant loses $1,500 to $3,000 per day in gross revenue when a major piece of equipment fails during operating hours. A quick-service operation loses $800 to $2,000 daily. A failed dishwasher during dinner service forces hand-washing of plates and glasses, which slows service by 30 to 50 percent and frustrates both staff and customers. A fryer breakdown eliminates an entire category of menu items, forcing customers to order alternatives or leave for a competitor. Refrigeration failure prevents safe ingredient storage, which forces temporary closure and potential health code violations that damage reputation long after the equipment is fixed.

The True Cost of Going Unprotected

A three-day refrigeration breakdown costs most restaurants $3,000 to $9,000 in lost sales alone, plus the $4,000 to $6,000 in spoiled food and repair expenses. Equipment breakdown coverage pays for the repair or replacement and covers lost business income during downtime, turning a $10,000 to $15,000 disaster into a covered loss. Without this protection, equipment failures become financial emergencies that damage cash flow and force difficult decisions about staffing and operations.

Understanding what these failures cost sets the stage for evaluating whether your current coverage actually protects your bottom line-or leaves you exposed when equipment fails.

Choosing Coverage That Matches What Your Kitchen Actually Needs

Inventory Your Equipment and Identify Critical Failures

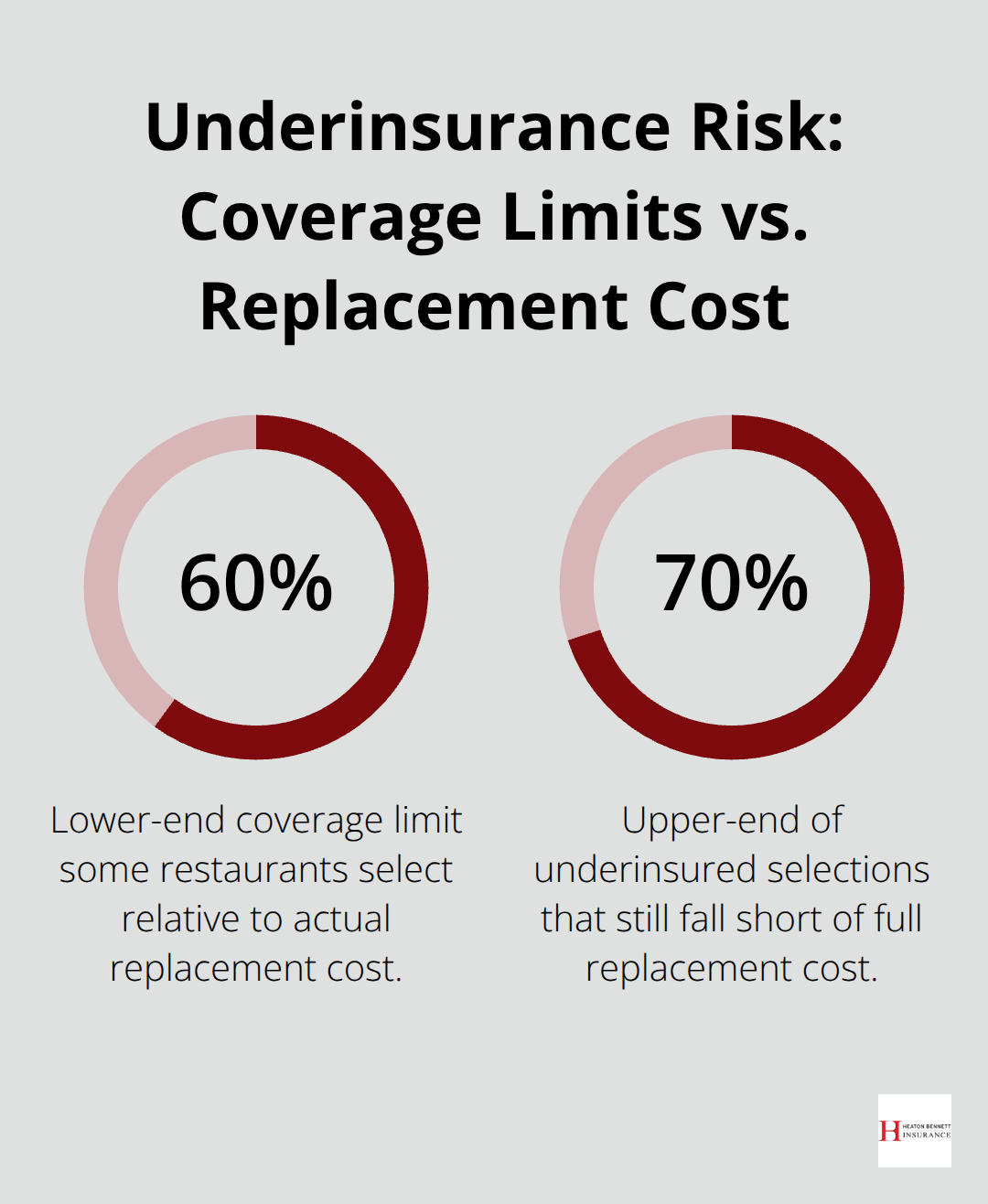

Start by listing your kitchen equipment and determining which pieces would cost the most to repair or replace and cause the greatest revenue loss if they failed. A walk-in refrigerator, commercial dishwasher, and convection oven typically top this list because failures in these units shut down entire service lines. A fryer breakdown eliminates fried items from your menu, but a refrigeration failure forces complete closure and health code violations. Calculate the replacement cost for each critical piece-refrigeration units run $8,000 to $15,000, commercial dishwashers cost $5,000 to $12,000, and convection ovens range from $4,000 to $10,000. Your coverage limit should match or exceed these replacement costs, not fall short. Many restaurants underestimate equipment value and choose limits that cover only 60 to 70 percent of actual replacement costs, leaving them exposed to significant out-of-pocket expenses when major failures occur.

Match Your Coverage Limits to Actual Replacement Costs

Equipment breakdown coverage protects your kitchen only when your policy limits reflect what you actually own. A walk-in cooler that costs $12,000 to replace requires a coverage limit of at least $12,000-anything less leaves you paying the difference out of pocket. Most restaurants carry $40,000 to $200,000 in total equipment value, so your aggregate coverage limit should account for multiple simultaneous failures. Request quotes that show coverage limits at $50,000, $75,000, $100,000, and $150,000 to understand how premium costs scale with protection levels. Higher limits cost more, but they prevent the financial shock of a major breakdown that exceeds your policy cap.

Select a Deductible That Fits Your Cash Flow

Deductibles directly impact your premium cost and your risk tolerance. A $500 deductible means you pay $500 out of pocket when a claim occurs, while a $2,000 or $2,500 deductible substantially lowers your monthly premium but shifts more financial burden to your business when equipment fails. If your restaurant operates with thin margins, a lower deductible protects cash flow during unexpected breakdowns. If you maintain substantial reserves and want to minimize premium costs, a higher deductible makes financial sense. Request quotes at multiple deductible levels-$500, $1,000, $1,500, and $2,500-to understand the premium difference and decide what your business can absorb.

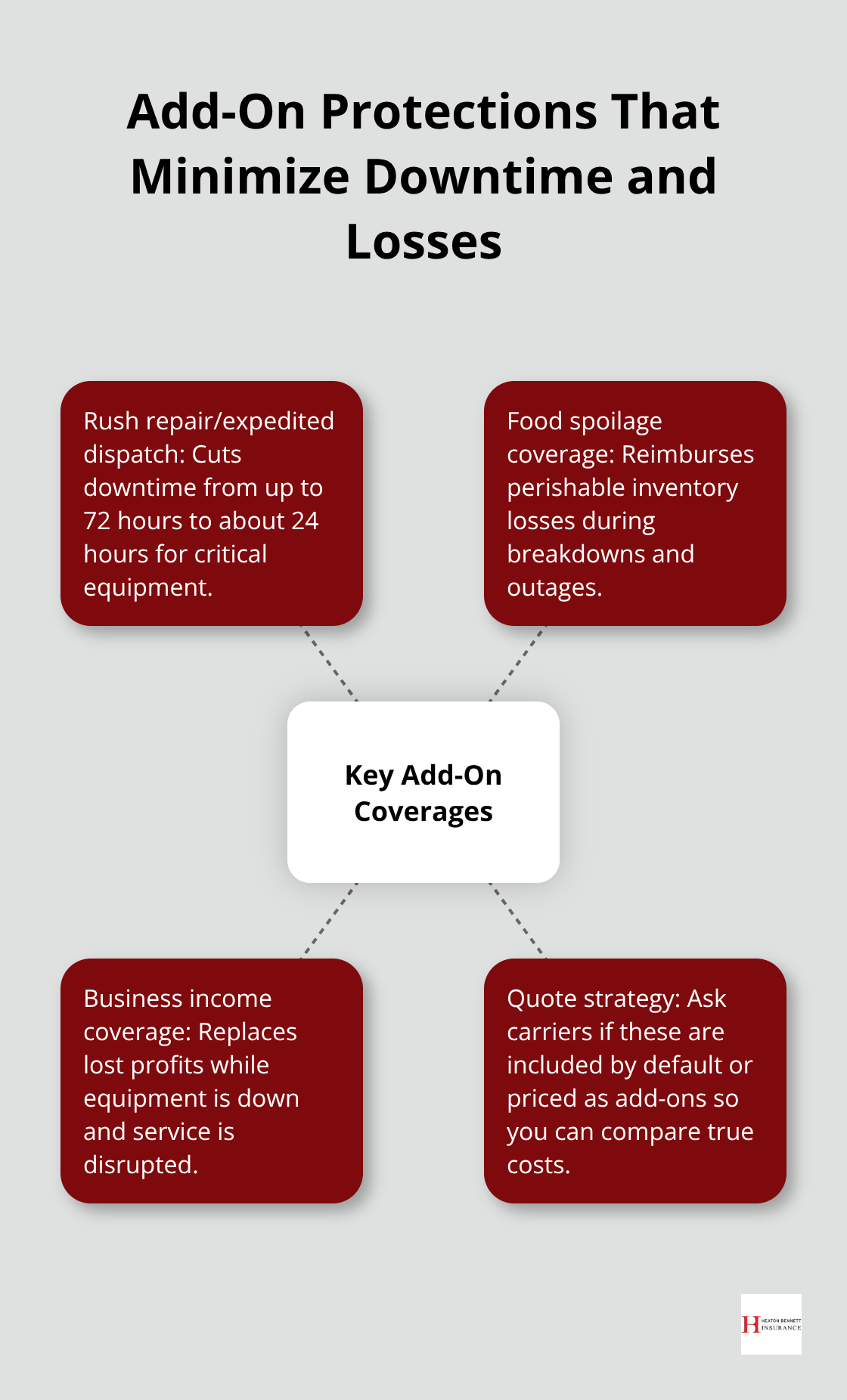

Evaluate Rush Repair Options and Additional Coverages

Beyond deductibles, assess whether rush repair options matter for your operation. Some carriers offer expedited technician dispatch that reduces downtime from 48 to 72 hours down to 24 hours, which justifies the premium increase for high-revenue restaurants. Food spoilage coverage and business income coverage are not always included by default, so explicitly ask carriers whether these protections are part of the base policy or available as add-ons. A three-day refrigeration failure costs $4,000 to $6,000 in spoiled inventory alone, making food spoilage coverage essential for restaurants with significant perishable inventory.

Business income coverage reimburses lost profits during downtime, which typically costs more than the repair itself. Request quotes that include both protections so you understand the true cost of comprehensive coverage versus limited plans.

Final Thoughts

Equipment breakdowns strike without warning, and the financial damage extends far beyond repair bills. Restaurant equipment coverage protects your kitchen’s most valuable assets and keeps your operation running when failures occur. The difference between having comprehensive protection and going unprotected often means the difference between absorbing a manageable loss and facing a financial crisis that disrupts service and damages customer relationships.

Your restaurant’s equipment represents a significant investment, typically ranging from $40,000 to $200,000 in total value. A single major breakdown can cost thousands in repairs, destroy perishable inventory, and eliminate revenue for days. Equipment breakdown coverage addresses these internal mechanical and electrical failures that standard property insurance ignores, covering repair costs, replacement expenses, lost business income, and food spoilage.

We at Heaton Bennett Insurance work with restaurant owners to build customized policies that protect against the specific equipment failures most likely to disrupt your operation. Contact Heaton Bennett Insurance to discuss your restaurant’s equipment protection needs and get a customized quote that reflects your actual kitchen value and operational risks.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.