Protecting Your Business Why Key Person Life Insurance Matters

Your business depends on specific people whose skills, relationships, and knowledge drive revenue and growth. When these key person contributors leave unexpectedly, the financial impact can threaten your company’s survival.

We at Heaton Bennett Insurance see businesses struggle with this reality every day. Key person life insurance provides the financial protection your company needs when losing essential team members.

What Is Key Person Life Insurance and How It Works

Key person life insurance pays your business a lump sum when someone who generates significant revenue or holds specialized knowledge dies or becomes permanently disabled. The company owns the policy, pays premiums, and receives the death benefit directly. This protection differs from standard life insurance because your business protects its financial interests rather than provides family benefits.

Who Qualifies as a Key Person in Your Business

Revenue generators top the list of key personnel. A salesperson who brings in 40% of annual sales qualifies immediately. The owner of a specialized skill set also counts as key personnel. A software developer who built your proprietary system cannot be replaced quickly.

Partners who hold major client relationships represent another category of key personnel. When they leave, clients often follow. Small Business Administration data shows businesses lose an average of 17% of revenue when key personnel depart unexpectedly.

How Premiums and Payouts Are Determined

Insurance companies base premiums on the key person’s age, health status, and coverage amount. Most businesses purchase coverage worth 5 to 10 times the key person’s annual salary or their estimated revenue contribution. A key employee who generates $500,000 annually might warrant $2.5 to $5 million in coverage.

Premiums typically range from $500 to $5,000 annually per $100,000 of coverage (depending on risk factors). The business receives tax-free death benefits in most cases, which provides immediate cash flow to cover replacement costs, lost revenue, and debt obligations during the transition period.

These financial protections become even more critical when you consider the specific risks your business insurance faces without proper coverage in place.

Financial Risks Your Business Faces Without Key Person Coverage

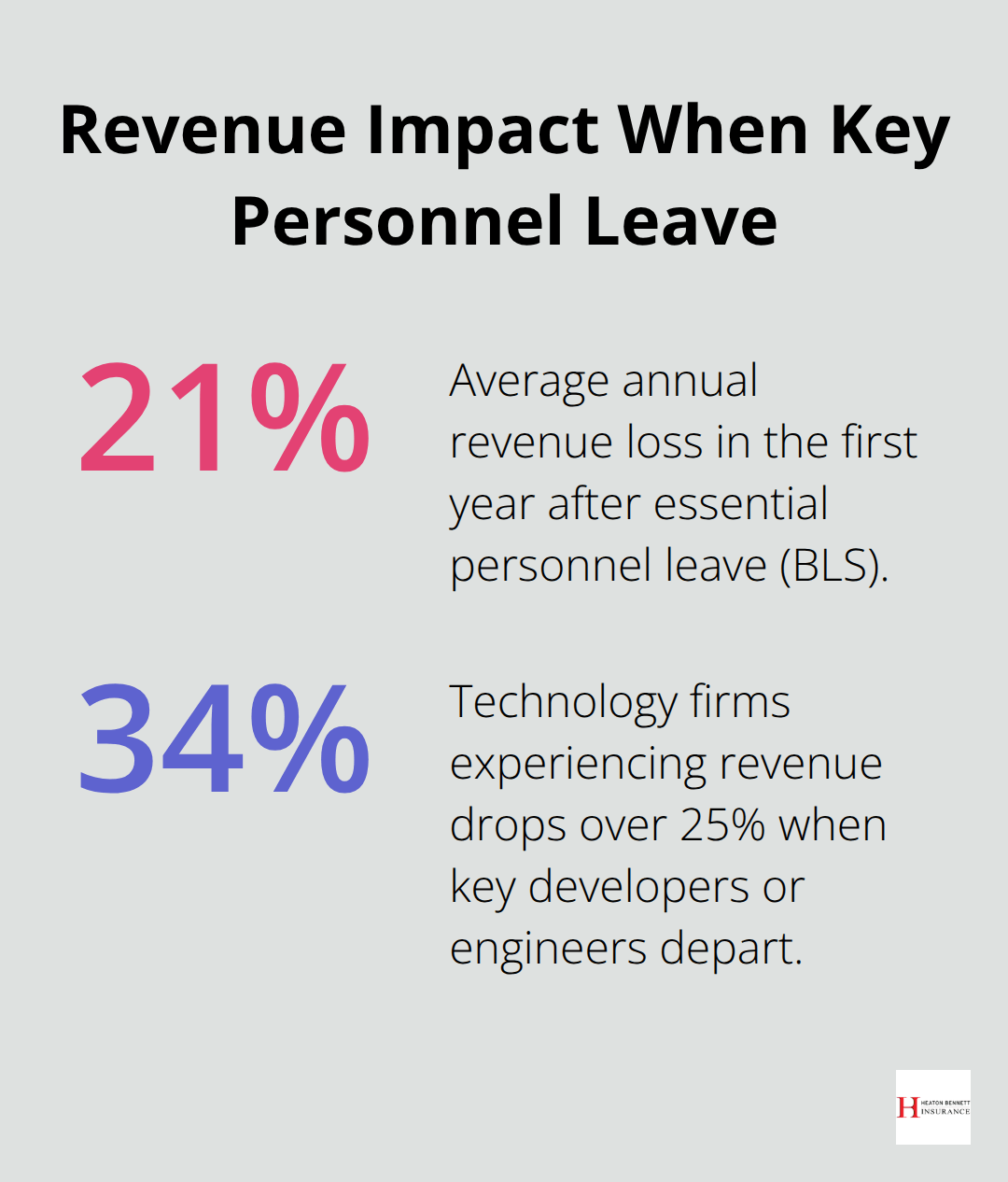

Key employee departures without insurance protection create immediate revenue disruption that most businesses underestimate. Bureau of Labor Statistics data reveals that companies lose an average of 21% of their annual revenue within the first year after essential personnel leave. Technology firms face even steeper losses, with 34% experiencing revenue drops that exceed 25% when key developers or engineers depart unexpectedly.

The financial damage starts immediately because these individuals often control client relationships, proprietary knowledge, or specialized processes that cannot transfer quickly.

Revenue Loss from Essential Team Members

Key personnel departures trigger cascading revenue losses that extend far beyond their direct contributions. Manufacturing companies lose an average of $1.2 million annually when production managers leave (according to Manufacturing Institute research), while professional service firms see client retention rates drop by 40% within six months of key relationship managers departing. These losses compound because remaining staff cannot immediately fill specialized roles or maintain the same productivity levels.

Costs of Recruiting and Training Replacements

Qualified replacements for key personnel cost businesses far more than most owners anticipate. Society for Human Resource Management research shows that executive replacement costs reach 213% of annual salary, while specialized technical roles cost 150% of annual compensation. A $100,000 key employee replacement actually costs your business $150,000 to $213,000 in recruitment fees, training expenses, and lost productivity during transition periods. Companies that spend $1,500 annually per employee on disability coverage often save $60,000 to $240,000 in replacement costs for each worker. These costs multiply when you factor in the 6 to 18 months new hires require to reach full productivity levels.

Impact on Business Loans and Credit Lines

Banks and lenders view key person departures as significant risk factors that can trigger loan covenant violations or credit line reductions. Federal Reserve Bank of St. Louis data indicates that 43% of small business loans include key person clauses that allow lenders to demand immediate repayment or modify terms when essential personnel leave. This creates dangerous cash flow crises precisely when your business needs financial flexibility most. Companies face emergency refinancing at higher rates or reduced credit availability just when they need capital to navigate transition periods.

Certain industries face even greater exposure to these risks, making key person insurance protection particularly valuable for specific business types and sectors.

Industries and Business Types That Need Key Person Insurance Most

Professional service firms face the highest risk exposure because client relationships concentrate in individual partners or senior staff members. Accounting firms lose 65% of their clients within 18 months when key partners depart (according to American Institute of CPAs research). Law practices see even steeper drops, with 78% of clients who follow attorneys to competitors.

These businesses generate revenue through personal expertise and trust relationships that cannot transfer to replacement staff quickly.

Professional Services Face Immediate Client Loss

Clients purchase specific expertise rather than company brands when they hire consultants. McKinsey research shows that strategy firms lose $2.3 million in annual revenue for every senior consultant who departs unexpectedly. Marketing agencies face similar challenges, with 83% that lose major accounts within six months of creative directors who leave. The specialized knowledge and client chemistry that drive these businesses cannot be replaced through standard processes.

Manufacturing and Technology Companies Risk Production Disruption

Small manufacturers depend heavily on production managers and quality control specialists whose departure stops operations immediately. National Association of Manufacturers data reveals that 67% of companies with fewer than 100 employees experience production delays that exceed 30 days when key technical personnel leave. Technology startups face even greater risks, with 45% that fail within two years of their lead developer or technical co-founder departure. These businesses require key person coverage worth 8 to 12 times annual salary because replacement costs include both recruitment expenses and extended revenue losses.

Family Businesses Concentrate Risk in Few Individuals

Family-owned companies create the most dangerous concentration of business-critical knowledge in single individuals. Family Business Institute research indicates that 71% of these businesses depend on one family member for major client relationships, financial management, and operational decisions. When these key family members become unavailable, 34% of family businesses close within 24 months because no succession plans or knowledge transfer systems exist. These companies need the highest coverage amounts because they face complete business failure rather than temporary revenue disruption.

Final Thoughts

Key person insurance protects your business from financial devastation when essential employees leave unexpectedly. The data shows clear patterns: professional service firms lose 65% of clients, manufacturers face production shutdowns, and family businesses risk complete closure without proper coverage. These risks make key person policies necessary business protection rather than optional coverage.

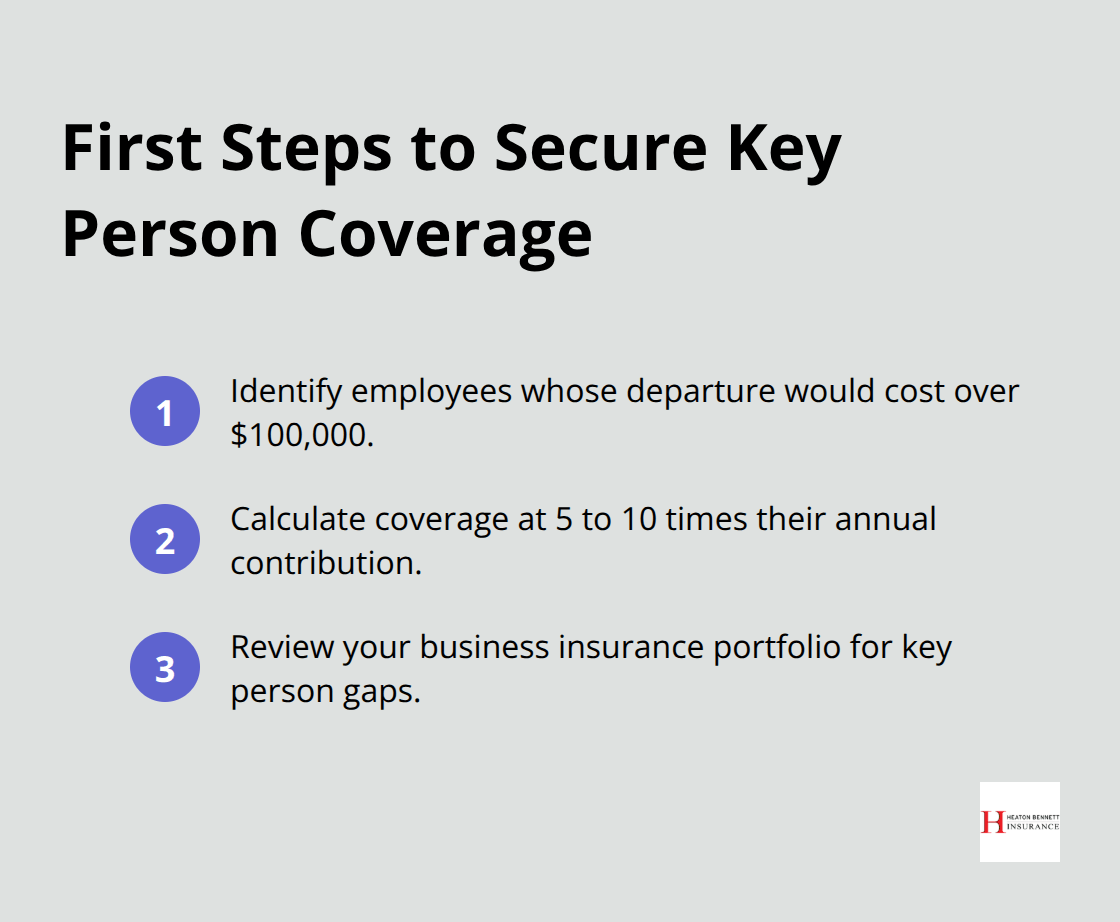

Start by identifying employees whose departure would cost your business more than $100,000 in lost revenue or replacement expenses. Calculate coverage amounts based on 5 to 10 times their annual contribution to your company. Review your current business insurance portfolio to identify gaps in key person protection.

We at Heaton Bennett Insurance help Austin businesses evaluate their key person insurance needs through our comprehensive Security Snapshot process (which includes detailed risk assessment and coverage recommendations). Our independent agency provides access to multiple carriers, allowing us to find tailored coverage solutions that match your specific business risks and budget requirements. Contact us today to protect your company from the financial impact of losing essential team members.