How to Choose Small Business Medical Insurance for Staff

Small business medical insurance for employees represents one of the most significant decisions you’ll make as an employer. The right plan attracts top talent while managing costs effectively.

We at Heaton Bennett Insurance understand that navigating healthcare options can feel overwhelming. This guide breaks down the selection process into manageable steps, helping you make informed decisions for your team.

Understanding Small Business Medical Insurance Requirements

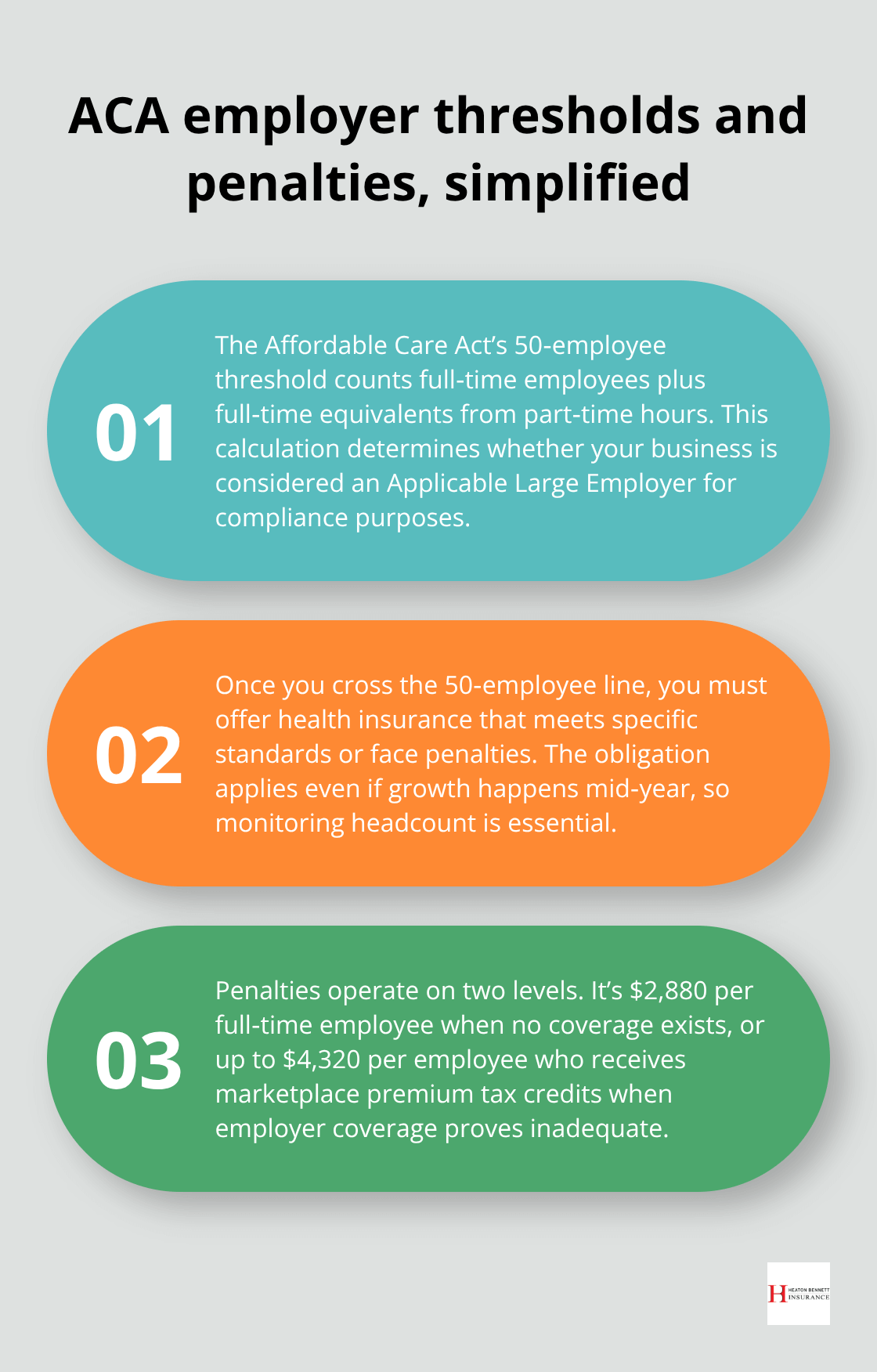

Small businesses face different medical insurance obligations based on their size and structure. Companies with fewer than 50 full-time equivalent employees have no federal mandate to provide health coverage under the Affordable Care Act. However, businesses that reach 50 or more full-time employees must offer health insurance that meets specific standards or face penalties of $2,880 per employee annually (according to 2024 IRS guidelines).

ACA Compliance Thresholds Create Clear Boundaries

The 50-employee threshold calculation includes full-time workers plus full-time equivalents based on part-time hours. Companies that cross this line face the employer shared responsibility payment if they fail to offer coverage. The penalty structure operates on two levels: $2,880 per full-time employee when no coverage exists, or up to $4,320 per employee who receives marketplace premium tax credits when employer coverage proves inadequate.

State Requirements Add Complexity

State requirements vary significantly across the country. Some states impose additional mandates on smaller employers beyond federal requirements. California requires businesses with five or more employees to provide workers’ compensation coverage. Hawaii mandates health insurance for employees who work more than 20 hours per week. These state-level variations make compliance research essential before you select any plan.

Tax Advantages Reduce Real Costs

Small businesses that qualify for the Small Business Health Care Tax Credit receive up to 50% of premiums paid back as credits. Eligibility requires fewer than 25 full-time equivalent employees with average wages below $64,000 annually. The JPMorgan Chase Institute reports that health insurance represents approximately 4% of operating expenses for nonemployer firms as of 2023. Premium payments qualify as business deductions and reduce taxable income dollar-for-dollar.

Health Savings Account contributions and Health Reimbursement Arrangements provide additional tax-advantaged options for both employers and employees. These benefits create a foundation for smart plan selection, which requires careful evaluation of different insurance plan types and their specific features.

Key Factors When Selecting Medical Insurance Plans

The three dominant plan types each serve different business priorities, and your choice determines both cost structure and employee satisfaction levels. HMO plans cost approximately 10-15% less than PPO alternatives according to the Kaiser Family Foundation, but restrict employees to specific provider networks and require primary care physician referrals for specialist visits. PPO plans offer broader provider access and no referral requirements, which makes them attractive to employees who value flexibility over cost savings. High-deductible health plans paired with Health Savings Accounts create the lowest premium costs but shift more financial responsibility to employees through deductibles that typically range from $1,500 for individuals to $3,000 for families in 2024.

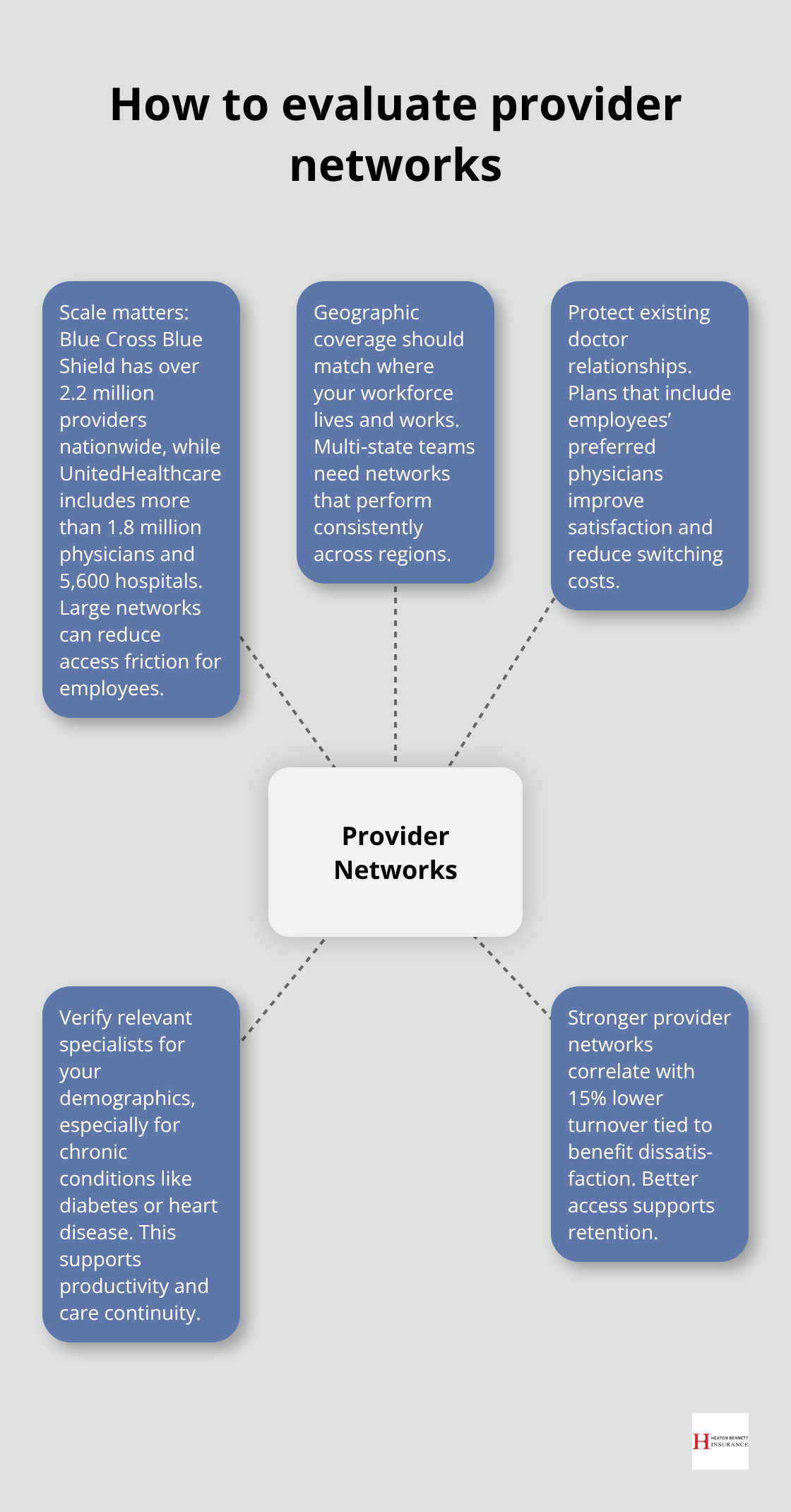

Network Size Determines Employee Access

Provider network evaluation requires specific data rather than general promises. Blue Cross Blue Shield operates the largest network with over 2.2 million providers nationwide, while UnitedHealthcare serves more than 1.8 million physicians and 5,600 hospitals. Network adequacy becomes critical when your workforce spans multiple geographic areas or includes employees with established doctor relationships. Small businesses should verify that networks include specialists relevant to their employee demographics, particularly for chronic conditions like diabetes or heart disease that affect workforce productivity.

The JPMorgan Chase Institute found that businesses with stronger provider networks experience 15% lower employee turnover rates related to benefit dissatisfaction.

Premium Structure Reveals True Costs

Premium analysis must account for the complete cost picture beyond monthly payments. Family coverage averages $605 monthly before tax credits, but employer contributions typically range from 50% to 100% of total costs. Businesses under $600,000 in annual revenue face median health insurance payroll burdens of 11.7% according to JPMorgan Chase Institute data. Smart employers calculate total annual costs (including deductibles, copayments, and out-of-pocket maximums) to understand real employee expenses. Plans with $500 monthly premiums but $5,000 deductibles often cost employees more than $750 premium plans with $2,000 deductibles when medical utilization occurs.

Coverage Areas Impact Employee Satisfaction

Geographic coverage becomes particularly important for businesses with remote workers or multiple locations. National carriers like UnitedHealthcare and Blue Cross Blue Shield provide consistent coverage across state lines, while regional insurers may offer better rates but limited geographic reach. Employees who travel frequently for business need plans that maintain coverage quality outside their home state. The average monthly premium for individual coverage reached $605 in 2023, but regional variations can create 20-30% cost differences between metropolitan and rural areas. Group health insurance premiums are paid with pre-tax dollars, which helps reduce overall payroll tax burden for employers.

Once you understand these plan fundamentals, the next step involves creating a smooth implementation process that gets employees enrolled efficiently while maximizing their understanding of available benefits.

Implementation and Employee Communication Strategies

Successful implementation begins 90-120 days before your desired start date, which allows sufficient time for carrier negotiations, employee education, and enrollment completion. The timeline depends heavily on your chosen effective date and carrier requirements. Most insurers require completed applications 30-45 days before coverage begins, but complex cases with medical underwriting can extend this timeline to 60 days. Small businesses that miss these deadlines often face delayed start dates or limited plan options, which creates gaps in coverage that expose both employer and employees to financial risk.

Employee Education Drives Enrollment Success

Effective communication requires multiple touchpoints rather than single announcement meetings. Research from the Society for Human Resource Management shows that employees need an average of seven exposures to benefit information before they make informed decisions. Host initial announcement meetings 60 days before enrollment, followed by individual consultation sessions 30 days later, and reminder communications weekly during the enrollment period.

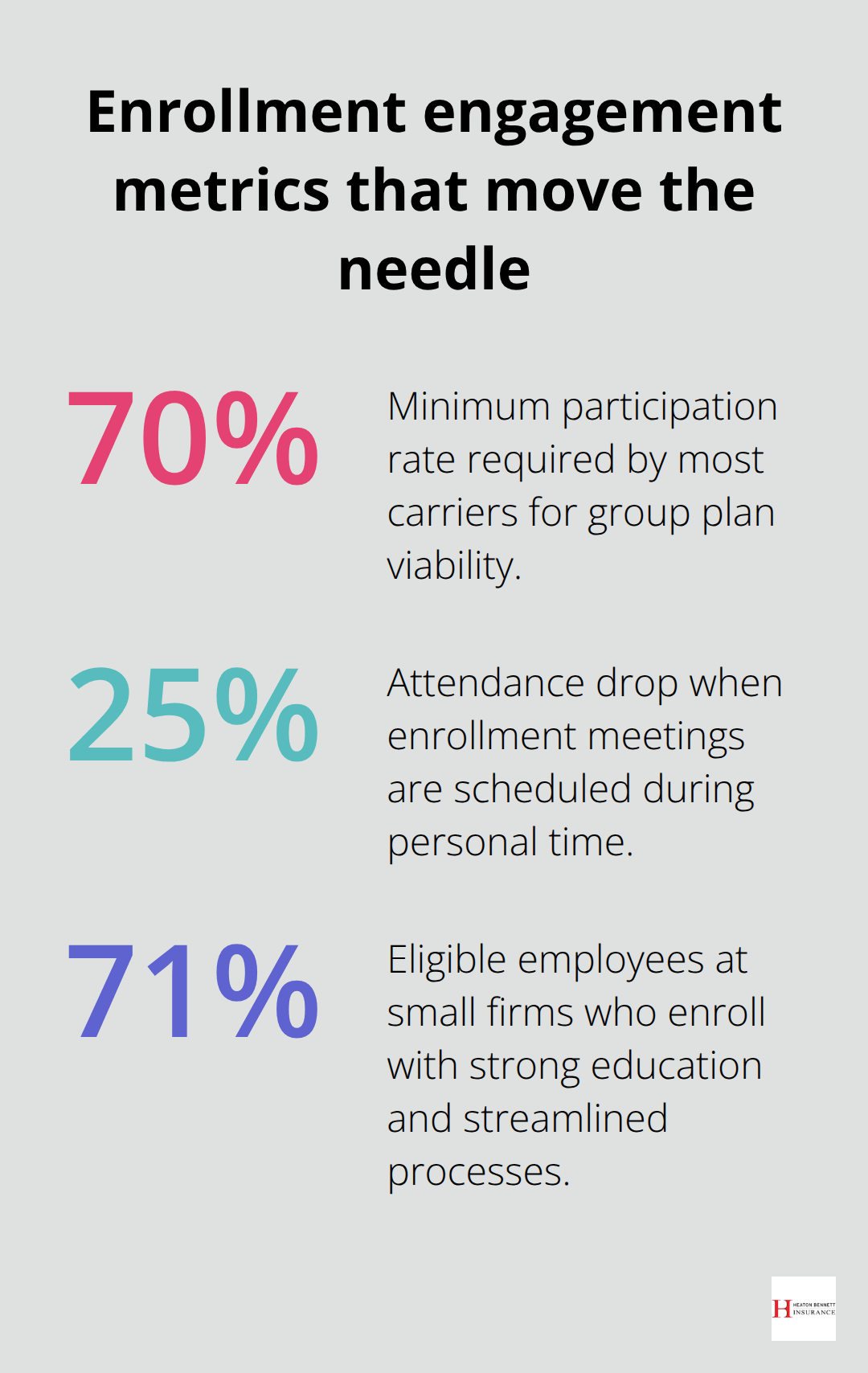

Provide comparison charts that show actual dollar amounts for common medical scenarios like emergency room visits, prescription medications, and specialist consultations. Employees respond better to concrete examples than abstract benefit descriptions. For instance, show that a $50 urgent care copay costs less than a $200 emergency room visit for minor injuries. The 70% minimum participation rate required by most carriers makes thorough education essential for plan viability.

Create simple decision trees that guide employees through plan selection based on their family size, preferred doctors, and typical medical usage patterns.

Open Enrollment Management Prevents Coverage Gaps

Annual open enrollment periods require systematic management to avoid administrative chaos and missed deadlines. Schedule enrollment meetings during work hours rather than lunch breaks to maximize attendance, as voluntary participation rates drop 25% when meetings occur during personal time. Use enrollment software that tracks completion status and sends automated reminders to employees who haven’t submitted forms.

The Kaiser Family Foundation reports that 71% of eligible employees at small firms enroll when offered comprehensive education and streamlined enrollment processes. Document all enrollment decisions with signed acknowledgment forms to protect against future disputes about coverage elections.

Plan Changes and Qualifying Events

Handle plan changes outside open enrollment only for qualifying life events like marriage, birth, or job status changes (as IRS regulations strictly limit mid-year modifications). Create backup communication methods including text messages and phone calls for employees who miss initial enrollment deadlines, since incomplete enrollments can disqualify entire groups from coverage.

Maintain detailed records of all qualifying events and their documentation requirements. Employees have 30 days from the qualifying event date to request coverage changes, and missing this window means they must wait until the next open enrollment period.

Final Thoughts

Small business medical insurance for employees requires you to balance multiple priorities: legal compliance, cost management, and employee satisfaction. The most successful employers focus on three essential criteria: understand your specific legal obligations based on company size, evaluate total cost structures beyond monthly premiums, and choose provider networks that serve your workforce effectively. Professional guidance becomes invaluable when you navigate the complex landscape of plan options, tax credits, and compliance requirements.

The JPMorgan Chase Institute data shows that businesses make informed decisions with expert support and achieve better cost outcomes and higher employee satisfaction rates. We at Heaton Bennett Insurance help Austin-area businesses find the right coverage solutions through our comprehensive approach to group benefits. Our independent agency status provides access to multiple carriers, which allows us to compare options and identify plans that match your specific needs and budget constraints.

Your next step involves three actions: gather employee demographic data, establish your budget parameters, and schedule consultations with qualified insurance professionals. Start this process 90-120 days before your desired effective date to allow sufficient time for thorough evaluation and smooth implementation (this timeline prevents coverage gaps and ensures proper plan selection). Contact Heaton Bennett Insurance to begin building a benefits package that attracts talent while managing costs effectively.