Who Needs Workers Compensation Insurance by Law?

At Heaton Bennett Insurance, we often encounter questions about who is required to have workers’ compensation insurance. This critical coverage protects both employers and employees in case of work-related injuries or illnesses.

Understanding the legal requirements for workers’ compensation can be complex, as they vary by state and industry. In this post, we’ll break down the federal and state mandates, explore exceptions to these laws, and discuss the consequences of non-compliance.

Who Must Have Workers’ Compensation Insurance?

Workers’ compensation insurance forms a critical part of employee protection and business risk management. While the federal government doesn’t mandate private employers to carry this insurance, each state sets its own rules, creating a complex landscape of requirements.

Federal Coverage

The Federal Employees’ Compensation Act (FECA) covers federal employees, but private employers must look to state laws for guidance.

State-Specific Mandates

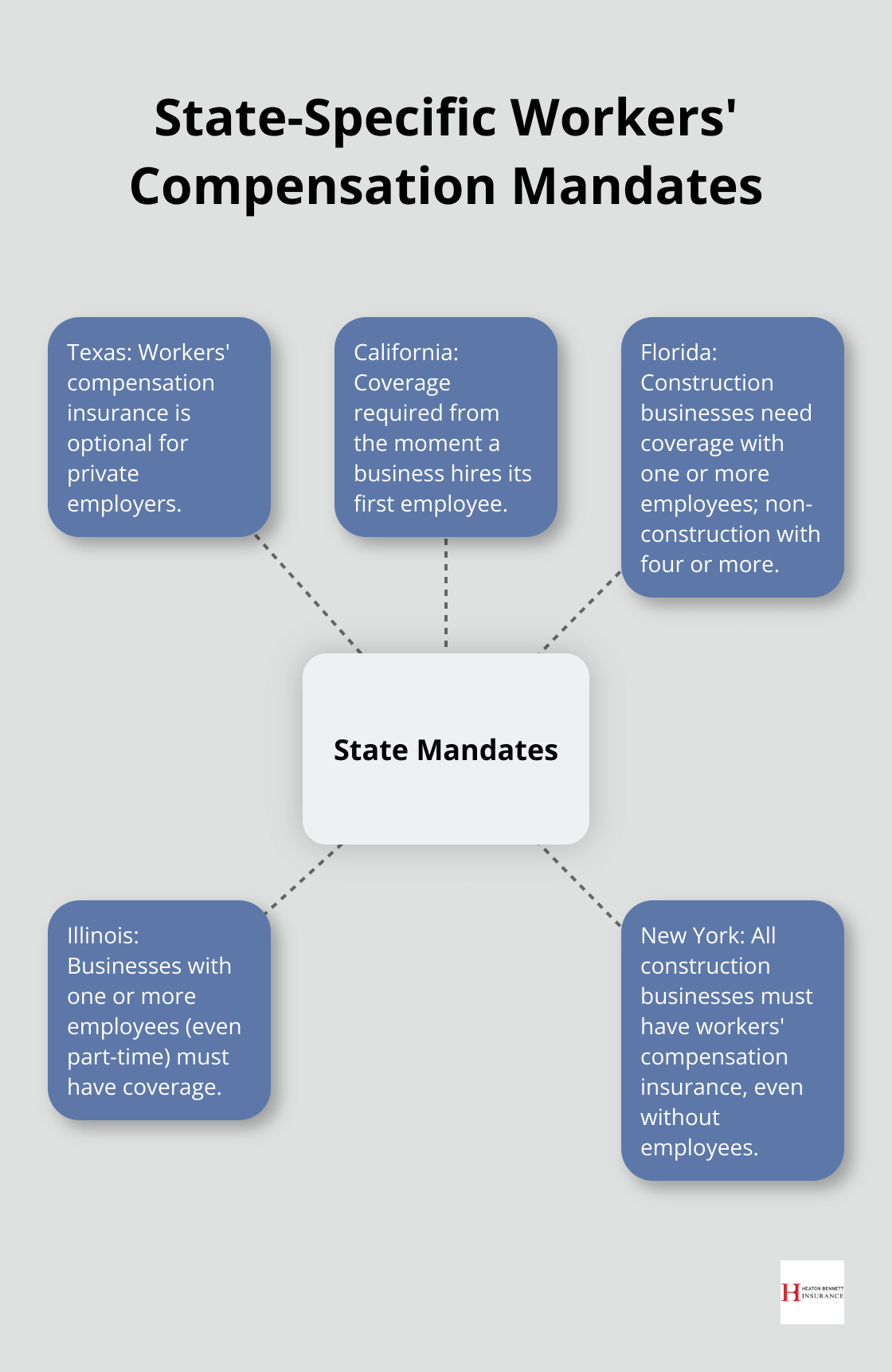

State requirements vary significantly. Texas stands alone as the only state where workers’ compensation insurance remains optional for private employers. In contrast, California requires coverage from the moment a business hires its first employee.

Employee Thresholds

Many states set employee thresholds that trigger the need for workers’ compensation insurance:

- Florida: Construction businesses need coverage with one or more employees; non-construction businesses with four or more.

- Illinois: Businesses with one or more employees (even part-time) must have coverage.

Industry-Specific Regulations

High-risk industries often face stricter regulations:

- Construction, manufacturing, and healthcare typically require coverage regardless of employee count.

- New York mandates all construction businesses to have workers’ compensation insurance, even without employees.

Exceptions and Special Cases

Some states carve out unique exceptions:

- Missouri exempts agricultural businesses from workers’ compensation requirements.

- Oklahoma allows certain small businesses to opt-out if they provide alternative benefit plans.

The National Federation of Independent Business reports severe penalties for non-compliance. California treats operating without required coverage as a criminal offense (punishable by fines up to $10,000 or a year in jail). New York imposes penalties of $2,000 per 10-day period of noncompliance.

Proper workers’ compensation coverage can shield businesses from financial catastrophe. For example, a small manufacturing company avoided a potential $500,000 lawsuit when an employee suffered an injury on the job. Their policy covered medical expenses and lost wages, averting a devastating financial blow.

The complex and ever-changing nature of workers’ compensation laws underscores the importance of working with experienced insurance professionals. These experts can navigate the intricacies of state laws and industry-specific needs, ensuring businesses remain compliant and protected.

As we move forward, let’s explore the exceptions to workers’ compensation laws, including small businesses, independent contractors, and specific industries with alternative arrangements.

Who’s Exempt from Workers’ Comp Requirements?

Workers’ compensation laws don’t apply uniformly to all businesses. While most companies must provide this coverage, significant exceptions exist. Understanding these exemptions can help you avoid unnecessary expenses and potential legal issues.

Small Business Thresholds

Many states set employee thresholds to determine when a business must obtain workers’ compensation insurance. For example:

- Alabama exempts businesses with fewer than five employees

- California requires coverage as soon as you hire your first employee

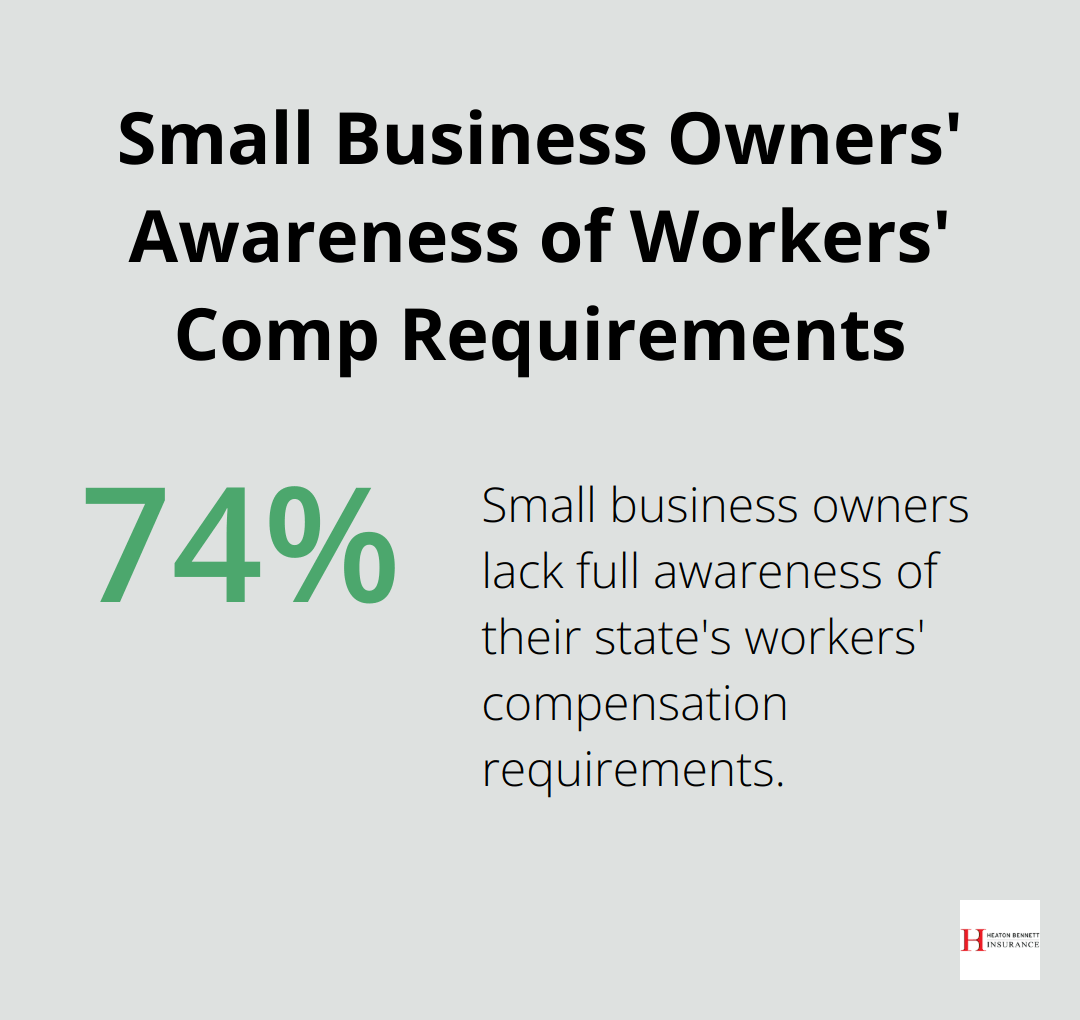

A National Federation of Independent Business study revealed that 74% of small business owners lacked full awareness of their state’s workers’ compensation requirements. This knowledge gap can lead to costly mistakes.

Independent Contractors and Self-Employed Individuals

Independent contractors and self-employed individuals typically don’t need to carry workers’ compensation insurance for themselves. However, this situation isn’t always clear-cut.

Some states (like California) may consider certain independent contractors as employees for workers’ compensation purposes. This classification depends on factors such as the hiring entity’s control over the worker’s performance.

Self-employed individuals should note that some clients might require them to have their own workers’ compensation policy as a condition of doing business.

Industry-Specific Exceptions

Certain industries have unique arrangements for workers’ compensation:

- Agriculture: Many states (including Texas and Kansas) exempt small agricultural operations from workers’ compensation requirements.

- Real Estate: Some states (like Florida) exempt real estate agents working on commission from mandatory coverage.

- Maritime Workers: These employees often fall under federal laws (such as the Longshore and Harbor Workers’ Compensation Act) instead of state workers’ compensation systems.

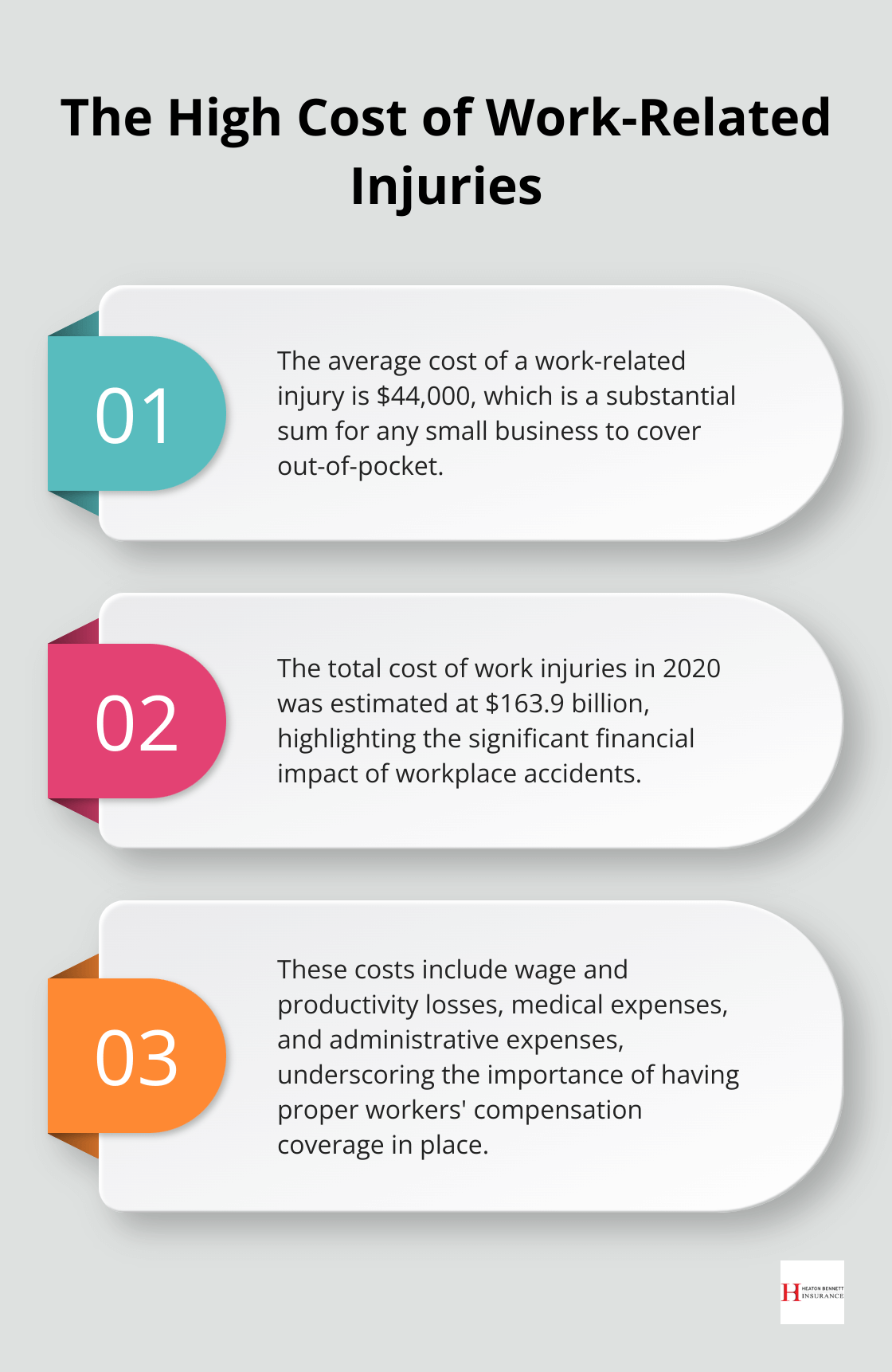

Even if your business qualifies for an exemption, voluntary workers’ compensation insurance can provide valuable protection. A 2022 National Safety Council report found that the average cost of a work-related injury was $44,000 (a substantial sum for any small business to cover out-of-pocket).

Laws change, and exceptions can be nuanced. Always consult with a qualified insurance agent or legal professional to understand your specific obligations and options. In the next section, we’ll explore the consequences of non-compliance with workers’ compensation laws.

The High Cost of Ignoring Workers’ Comp Laws

Financial Penalties That Bite

State-imposed fines for non-compliance can devastate businesses. California imposes penalties up to $100,000 or twice the amount the employer would have paid in premiums during the period of non-coverage (whichever is greater). New York fines businesses $2,000 per 10-day period of non-compliance, which can quickly accumulate into substantial amounts.

Legal Vulnerabilities Exposed

Businesses without workers’ compensation insurance lose their statutory protection against civil lawsuits from injured employees. This exposure can lead to costly legal battles and potentially bankrupting settlements. A 2021 study by the Insurance Information Institute found that the average workers’ compensation claim cost $41,353. Without insurance, businesses must bear this cost entirely out-of-pocket.

Reputational Damage and Operational Disruptions

Non-compliance can tarnish a company’s reputation, making it difficult to attract and retain employees. Some states (like Pennsylvania) can issue stop-work orders for businesses operating without required coverage. This can lead to project delays, contract breaches, and lost revenue.

The Texas Department of Insurance reports that businesses without workers’ compensation coverage lose important legal protections. These include limits on the amount that might be recovered in a lawsuit and prohibitions against recovering damages if the injured employee was intoxicated.

The Hidden Costs of Non-Compliance

Non-compliance can lead to increased insurance premiums in the future. Insurance providers often view businesses with gaps in coverage as high-risk, resulting in higher rates when coverage is eventually secured.

The National Safety Council estimates that the total cost of work injuries in 2020 was $163.9 billion. This figure includes wage and productivity losses, medical expenses, and administrative expenses. It underscores the importance of having proper coverage in place.

Final Thoughts

Businesses must understand who is required to have workers’ compensation insurance. The legal landscape varies across states, with most mandating coverage for employers once they reach a certain number of employees. Exceptions and special cases exist, which makes it essential to stay informed about specific obligations. Compliance with workers’ compensation laws protects businesses and employees from financial and legal risks.

Workers’ compensation provides financial protection and legal immunity for businesses, while ensuring access to medical care and wage replacement for employees. This mutual protection creates a safer, more secure work environment for all parties involved. The complexities of workers’ compensation laws and the high stakes underscore the value of expert guidance in navigating these intricate regulations.

At Heaton Bennett Insurance, we can help you understand your obligations and explore your options (including finding the right coverage for your business needs). Our team specializes in workers’ compensation insurance and can assist you in staying compliant with ever-changing regulations. Regular reviews of your coverage will help ensure your business remains protected and compliant with the law.