First-Time Home Insurance Buyer’s Guide

Buying home insurance for the first time can be overwhelming. There’s a lot to consider, from understanding coverage types to determining the right policy limits for your needs.

At Heaton Bennett Insurance, we’ve guided countless first-time homeowners through this process. Our comprehensive guide will walk you through the essentials of home insurance, helping you make informed decisions to protect your new investment.

What Home Insurance Covers

Protecting Your Home and Belongings

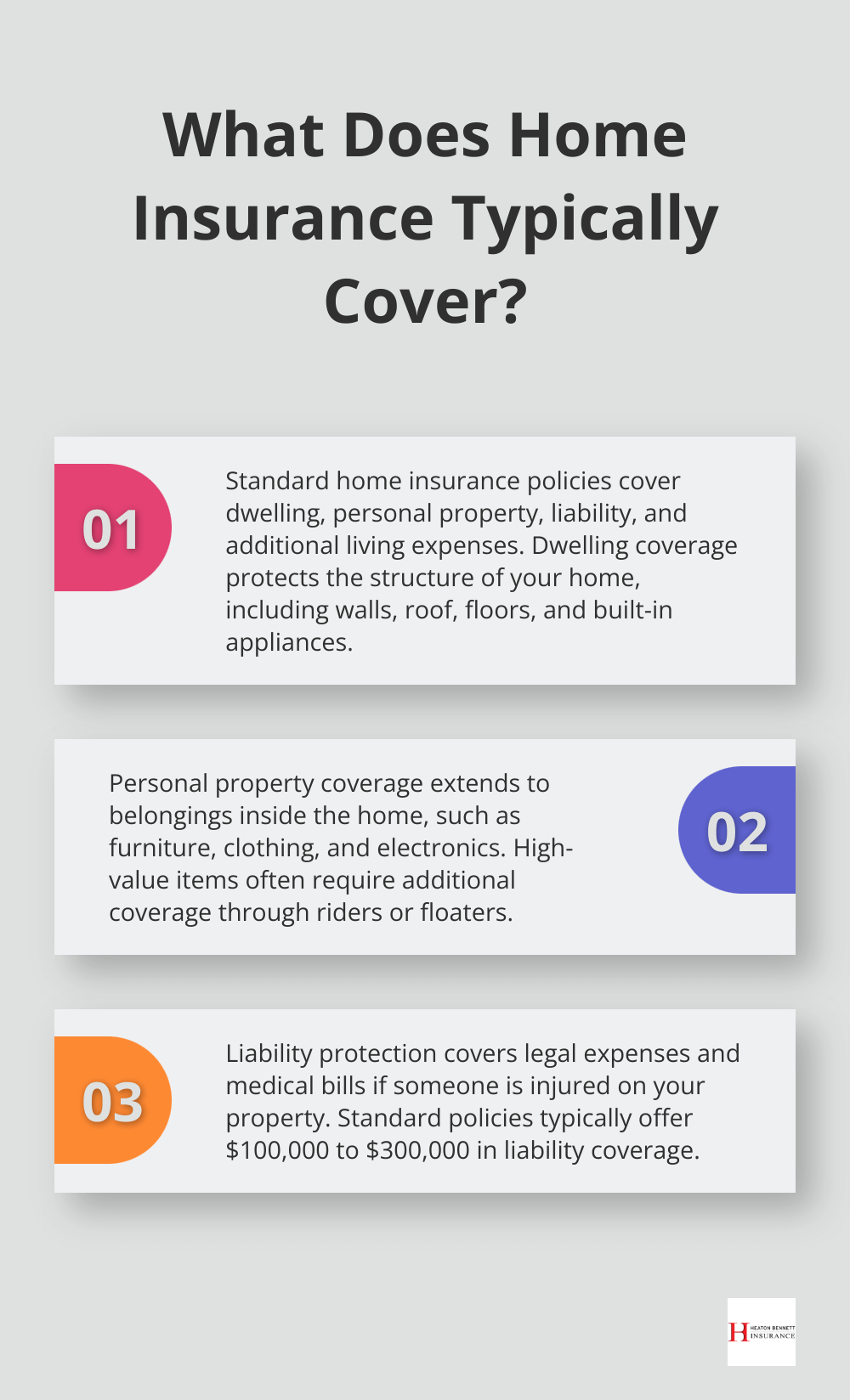

Home insurance serves as a vital safeguard for your property and finances. A standard home insurance policy typically covers your dwelling, personal property, liability, and additional living expenses.

Your dwelling coverage protects the structure of your home. This includes walls, roof, floors, and built-in appliances. Most policies cover damage from fire, windstorms, hail, lightning, and theft (as reported by the Insurance Information Institute).

Personal property coverage extends to your belongings inside the home. This includes furniture, clothing, and electronics. High-value items like jewelry or art often require additional coverage through riders or floaters.

Liability and Additional Living Expenses

Liability protection is an essential component that first-time buyers often overlook. It covers legal expenses and medical bills if someone suffers an injury on your property. Standard policies typically offer $100,000 to $300,000 in liability coverage.

Additional living expenses coverage helps pay for temporary housing if your home becomes uninhabitable due to a covered event. This can provide financial relief during extensive repairs or rebuilding.

Policy Types and Exclusions

Several types of home insurance policies exist, with HO-3 being the most common for single-family homes. It provides broad coverage for the structure and named perils coverage for personal property.

You must understand what your policy doesn’t cover. Standard policies typically exclude damage from floods, earthquakes, and normal wear and tear. In flood-prone areas, mortgage lenders often require separate flood insurance.

Understanding Your Coverage

First-time buyers should review policy details carefully with their agent. Many insurance agencies (including Heaton Bennett Insurance) offer a comprehensive review process to ensure tailored coverage that meets specific needs.

The right home insurance policy does more than meet lender requirements; it protects what’s likely your largest investment. Take time to understand your coverage and ask questions. Your financial security depends on it.

As we move forward, let’s explore the factors that affect your home insurance premiums, helping you make informed decisions about your coverage.

What Impacts Your Home Insurance Costs?

Location Matters

Your home’s location significantly influences your insurance costs. Areas prone to natural disasters like hurricanes, tornadoes, or wildfires typically have higher premiums. Florida homeowners often pay more due to hurricane risk. The Insurance Information Institute reports that Florida’s average annual premium is $4,231 (nearly triple the national average of $1,585).

Urban areas with higher crime rates may also see increased premiums. However, proximity to fire stations can lower costs.

Age and Construction

Older homes often cost more to insure. They may have outdated electrical systems, plumbing, or roofing, which increases the risk of damage. Homes built with fire-resistant materials like brick or stone typically have lower premiums than wood-frame houses.

The National Association of Home Builders states that the median age of owner-occupied homes in the U.S. is 39 years. If your home is older, upgrades to key systems could potentially reduce insurance costs.

Safety First

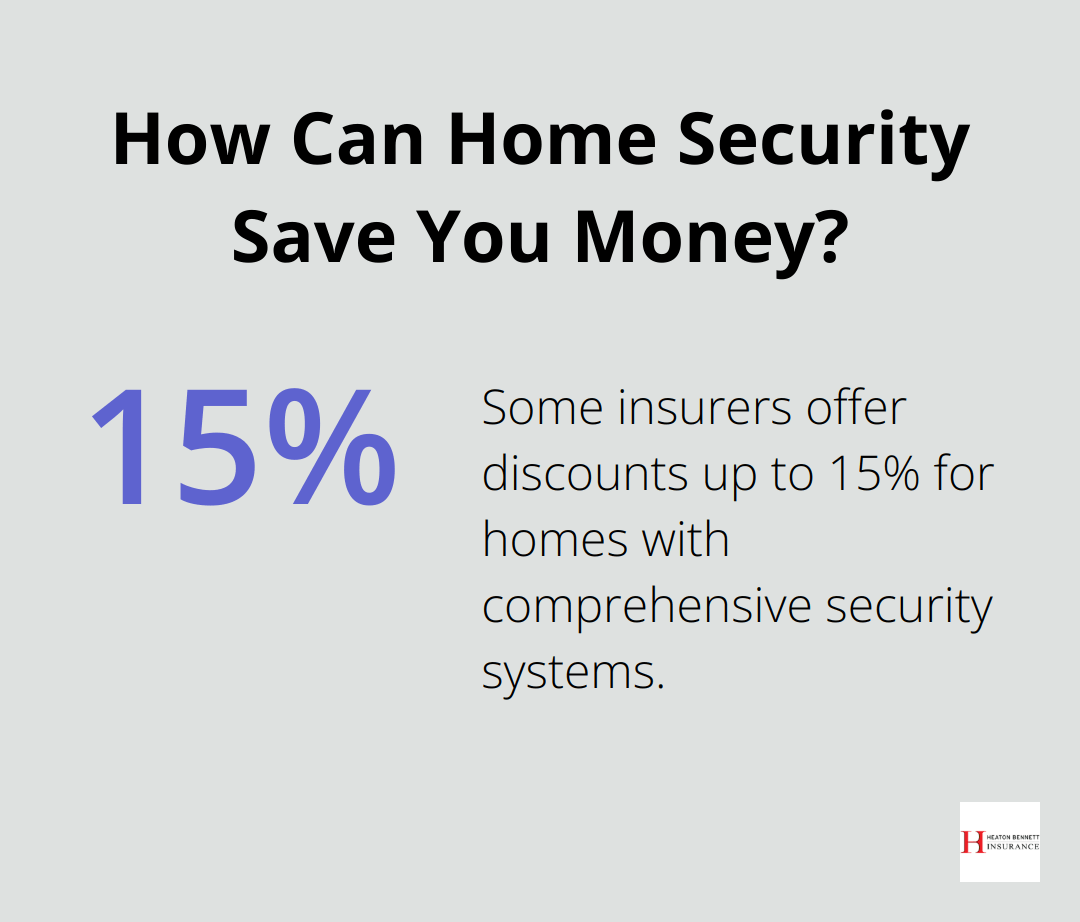

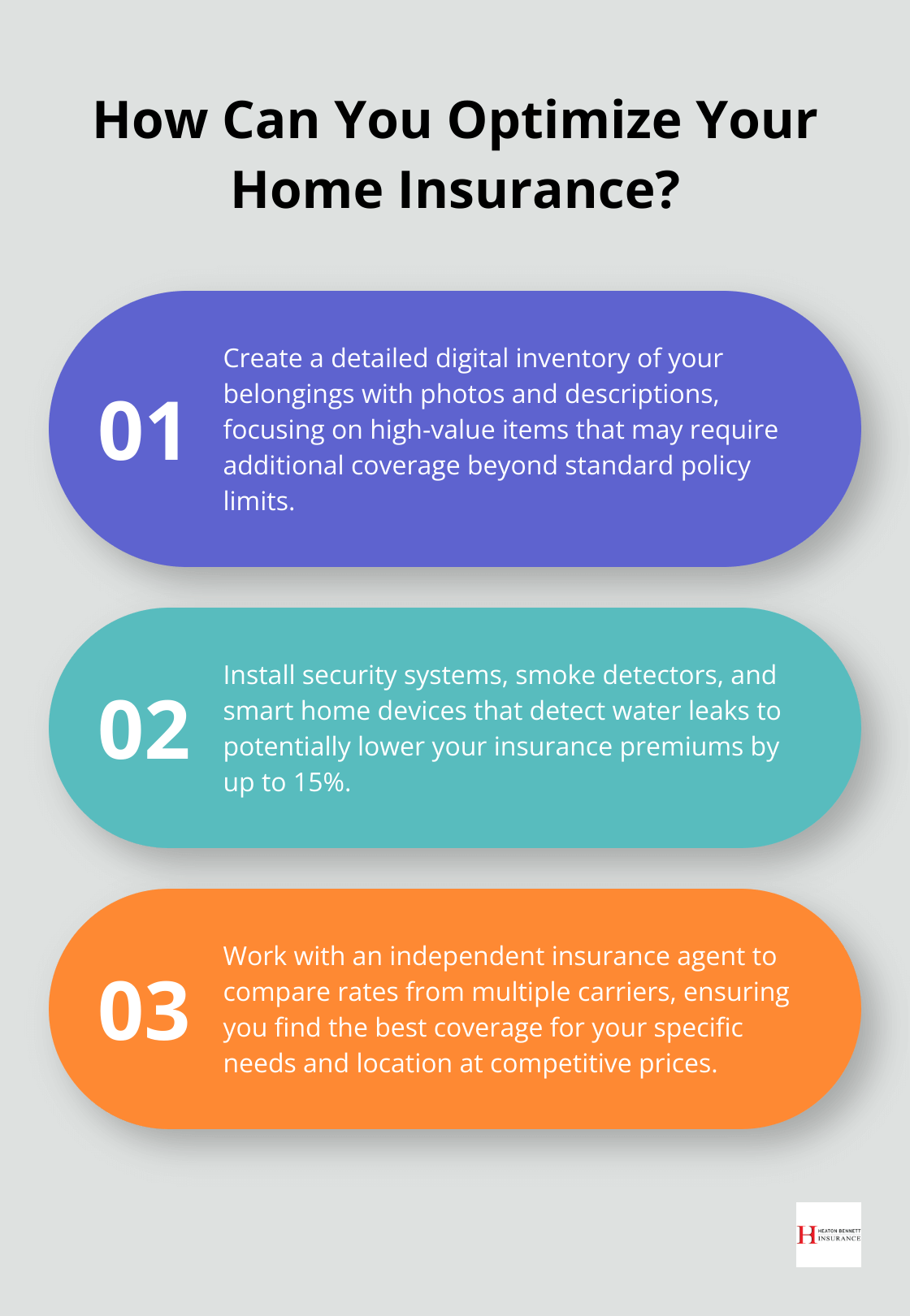

Installing security systems, smoke detectors, and deadbolt locks can lower your premiums. Some insurers offer discounts up to 15% for homes with comprehensive security systems. Smart home devices that detect water leaks or monitor for break-ins can also lead to savings.

Your Financial Picture

Your credit score can affect your home insurance rates. The Federal Trade Commission found that consumers with lower credit scores file insurance claims more frequently. As a result, many insurers use credit-based insurance scores to help determine premiums.

Your claims history also plays a role. Multiple claims in a short period can lead to higher premiums or even policy non-renewal. It’s often wise to pay for minor repairs out-of-pocket rather than filing small claims.

Insurance Company Selection

The insurance company you choose can significantly impact your costs. Each insurer uses different methods to calculate risk and set premiums. Some may offer more competitive rates for certain types of properties or locations.

Independent agencies (like Heaton Bennett Insurance) can compare rates from multiple carriers, potentially finding you better coverage at a lower cost. This approach allows you to benefit from a wider range of options without the hassle of contacting each insurer individually.

As we move forward, we’ll explore how to choose the right coverage for your specific needs, ensuring you’re adequately protected without overpaying.

How to Choose the Right Home Insurance Coverage

Assess Your Home’s Value

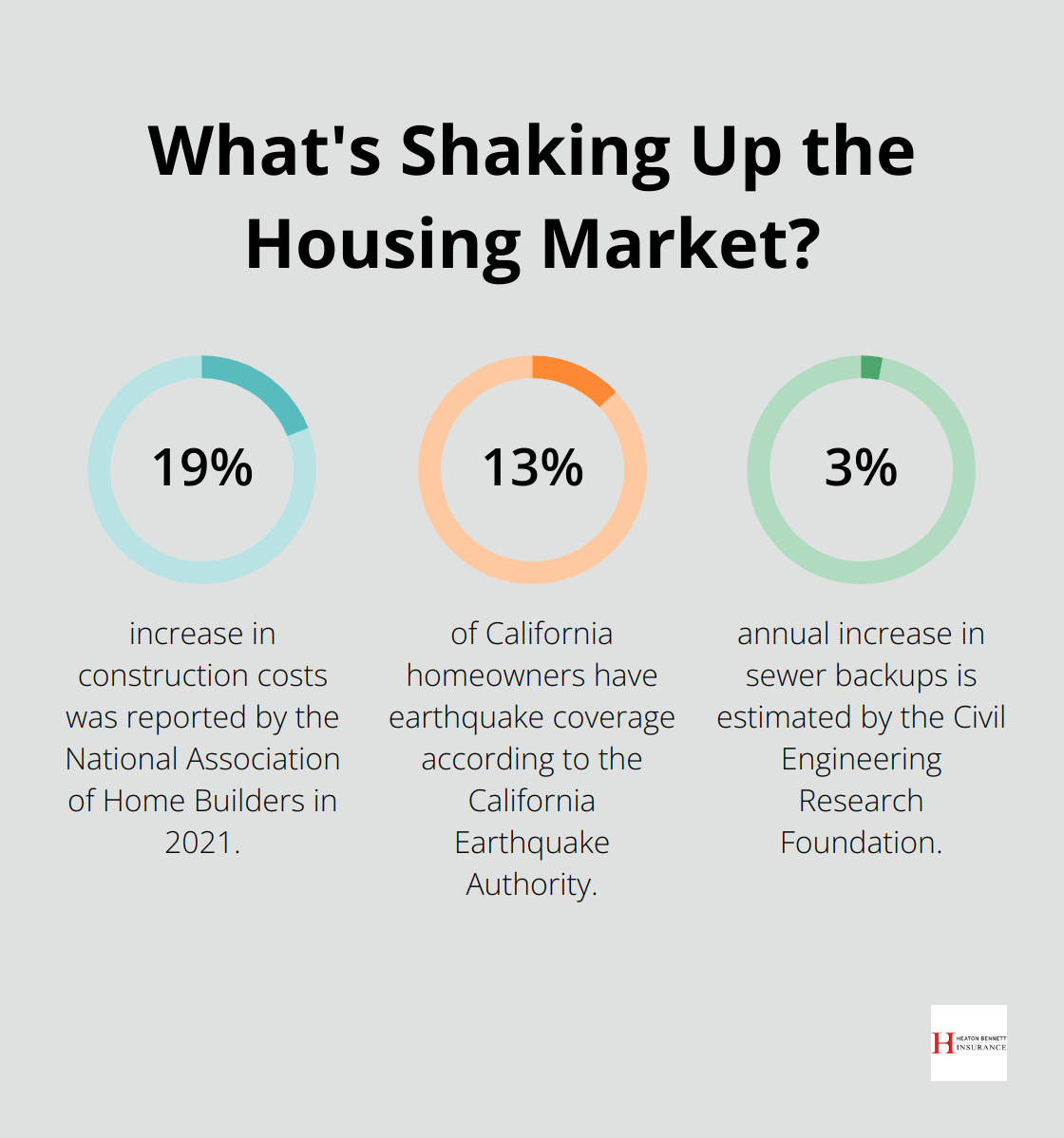

Start with an accurate estimate of your home’s replacement cost. This differs from market value or purchase price. It represents the cost to rebuild your home from scratch. The National Association of Home Builders reports a 19% increase in construction costs in 2021. This suggests your coverage needs might exceed initial expectations.

Advanced tools can calculate replacement costs precisely (ensuring you avoid underinsurance). Underinsurance can result in significant out-of-pocket expenses if disaster strikes.

Create a Personal Property Inventory

Compile a detailed list of your belongings. Most policies cover personal property at about 50-70% of your dwelling coverage (according to the Insurance Information Institute). This might not suffice for everyone.

High-value items like jewelry, art, or collectibles often require additional coverage. A digital inventory with photos and descriptions will help determine coverage needs and simplify potential claims processes.

Consider Liability Needs

Standard policies typically offer $100,000 to $300,000 in liability coverage. Evaluate if this meets your needs. If you possess significant assets or a high income, consider increasing this limit or adding an umbrella policy. Certain features (pools, trampolines, dogs) can increase your liability risk.

Explore Optional Coverages

Flood insurance is essential for many homeowners. The National Flood Insurance Program states that one inch of floodwater can cause up to $25,000 in damage. Standard policies exclude flood coverage.

Earthquake coverage warrants consideration, especially in prone areas. The California Earthquake Authority reports only 13% of California homeowners have this coverage, leaving many at risk.

Sewer backup coverage, often overlooked, can prevent costly repairs. The Civil Engineering Research Foundation estimates sewer backups increase at about 3% annually.

Work with an Independent Agent

Navigating these choices can challenge new homeowners. An independent agent can access multiple carriers, compare options, and find optimal coverage at competitive rates.

A thorough needs assessment will help you avoid over or underinsurance. Clear explanations of policy details will enable informed decisions.

The right coverage balances protection and cost. Proper guidance can secure comprehensive coverage that provides peace of mind for new homeowners.

Final Thoughts

Buying home insurance for the first time requires understanding coverage basics, premium factors, and policy selection. Your home’s location, age, and construction materials significantly impact insurance costs. Safety measures and a good credit score can reduce premiums. We recommend an annual policy review to ensure adequate and cost-effective coverage as your needs change.

At Heaton Bennett Insurance, we guide first-time buyers through home insurance complexities. Our independent agents access multiple carriers to find tailored coverage options. We use a comprehensive “Security Snapshot” process to assess requirements and provide personalized recommendations (this approach sets us apart from many other agencies).

We offer standard homeowners policies and specialized coverage for high-value items or natural disasters. Our team strives to provide peace of mind by ensuring proper protection for your new home and belongings. Contact us for expert advice and support in securing the right home insurance policy for your needs.