Nonprofit Property Coverage: Safeguarding Assets and Programs

Nonprofits operate with limited budgets and stretched resources, making every asset count. Standard commercial insurance often leaves critical gaps that leave your organization vulnerable to significant financial loss.

At Heaton Bennett Insurance, we understand that nonprofit property coverage requires a different approach than typical business policies. This guide walks you through the specialized protections your organization actually needs.

Why Nonprofits Face Different Property Risks

Nonprofits hold assets that standard commercial policies simply don’t account for. A youth center stores sound equipment, tables, and stage gear worth thousands. A food bank maintains freezers filled with inventory, plus vehicles for distribution. A community theater owns lighting rigs, costumes, and sets that represent years of work. When a break-in or fire strikes, these organizations lose not just physical items but the ability to serve their communities. Standard commercial property insurance treats these assets like typical business inventory, applying generic limits and exclusions that leave nonprofits dangerously underprotected.

Theft and vandalism affect nonprofits disproportionately. Break-ins cost between $5,000 and $15,000 in repairs plus losses and disrupted programs, according to property insurance data. Yet many nonprofits discover too late that their policies exclude volunteer-operated facilities, seasonal equipment stored off-site, or items in transit to events. Nonprofit property coverage averages about $141 per month, suggesting affordable protection exists, but only if you match coverage to actual assets and activities.

Seasonal Equipment and Off-Site Exposures

Nonprofits operate differently than traditional businesses. A mentorship organization might store donated computers and learning materials in a rented warehouse during off-season months. An arts nonprofit ships instruments and artwork to satellite locations or community events. Standard commercial policies often exclude property in transit or stored at temporary locations, leaving these items vulnerable.

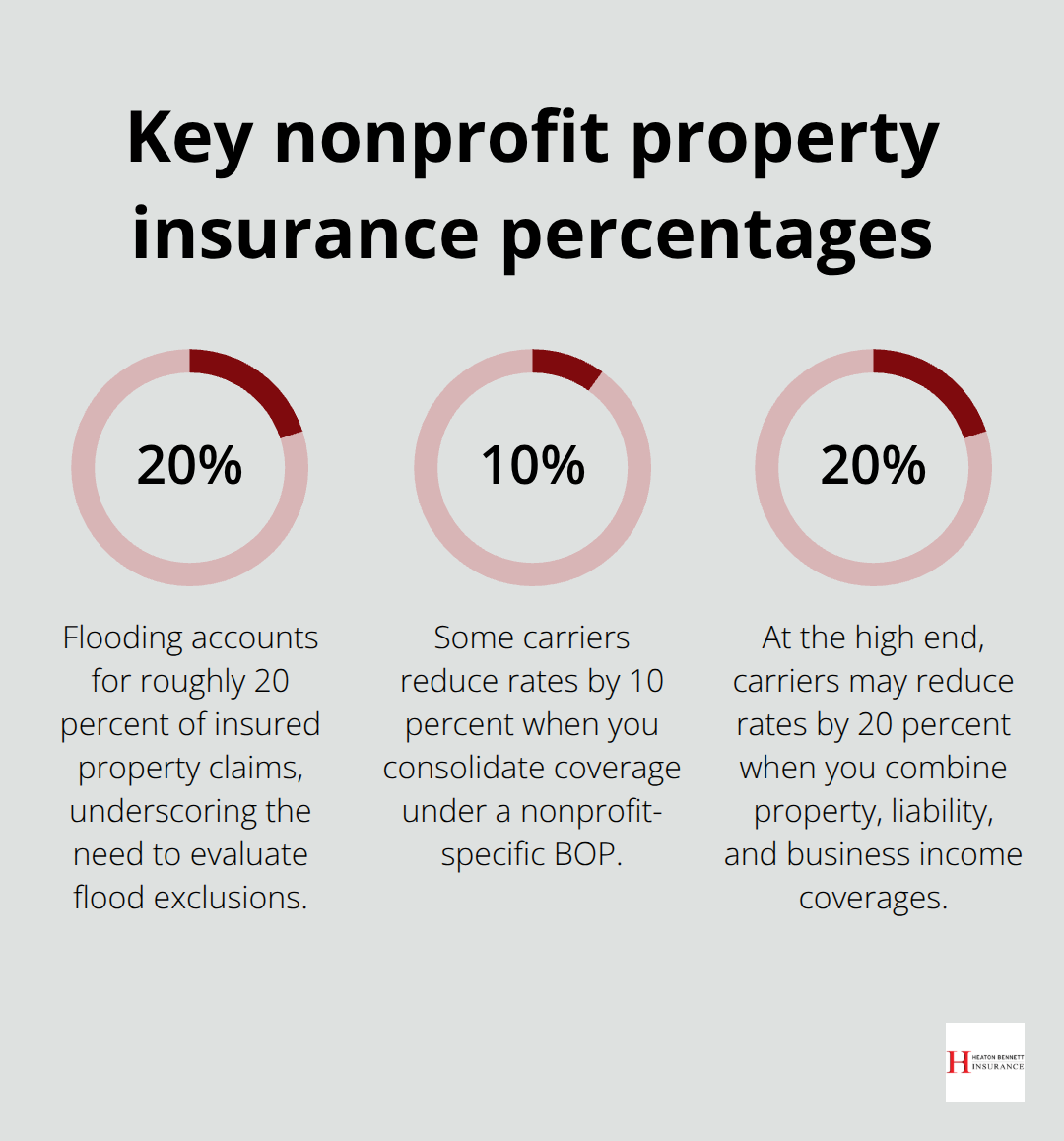

Flooding accounts for roughly 20 percent of insured property claims, yet many nonprofit policies include flood exclusions that require separate coverage. Similarly, equipment used at outdoor events or partner facilities frequently falls outside standard policy boundaries. You need coverage that explicitly addresses where your assets actually live throughout the year, not just what sits in your main office building.

The Gap Between Liability and Property Protection

Many nonprofits hold general liability insurance to protect against injury claims but overlook property coverage entirely. These are separate protections serving different purposes. Liability shields your organization when someone gets hurt at your event or claims damage to their belongings. Property coverage protects your own buildings, contents, and revenue streams when fire, theft, or weather strikes.

A liability claim from damaged third-party property can exceed $50,000, yet your organization still faces its own asset losses if property coverage doesn’t exist. Nonprofits need both working together. When you pair property coverage with business income insurance, you protect not just equipment but also ongoing expenses like rent, utilities, and payroll while operations resume after a loss. This dual approach prevents one disaster from forcing program cuts or staff layoffs.

An insurance provider experienced in nonprofit operations helps you address mission-critical assets and the specific ways your organization operates. Understanding these coverage types positions you to evaluate what your nonprofit actually needs.

What Property Coverage Types Does Your Nonprofit Actually Need

Building Coverage: Protecting Your Physical Structure

Building coverage protects the physical structure your nonprofit occupies, whether owned or leased. This includes walls, roofs, foundations, built-in fixtures, and permanent installations like HVAC systems or security equipment. If your nonprofit owns the building, this coverage is non-negotiable. If you lease, your landlord typically requires you to carry it, and your lease agreement specifies coverage limits and replacement-cost requirements.

The Hartford reports nonprofit property policies average about $141 per month, but building coverage costs depend heavily on square footage, age, construction type, and location. A 5,000-square-foot community center in a flood zone pays significantly more than a small office in a low-risk area. Document your building’s year built, square footage, any renovations, and current replacement value before requesting quotes. Underwriters scrutinize these details, and inaccurate information leads to coverage disputes when claims arise.

Many nonprofits underestimate replacement costs by using depreciated values instead of what it actually costs to rebuild today. A 30-year-old building might have a depreciated book value of $200,000 but a true replacement cost of $800,000. This gap creates catastrophic exposure. Get a professional property appraisal or work with an insurance agent who specializes in nonprofits to establish realistic limits.

Contents and Equipment: Protecting What’s Inside

Contents and equipment coverage handles everything inside your building that isn’t permanently attached. For a food bank, this means freezers, refrigeration units, packaging equipment, and inventory. For a youth center, it covers computers, donated furniture, sports equipment, and art supplies. For a theater, it protects lighting rigs, sound systems, costumes, and set pieces.

This coverage extends to items stored at satellite locations, in transit to events, or temporarily housed in partner facilities, but only if your policy explicitly includes off-site protection. Many standard commercial policies exclude property away from the main location entirely. Theft and vandalism of contents account for significant losses in the nonprofit sector. Break-ins cost $5,000 to $15,000 in repairs, replacement, and program disruption according to property insurance data. Your coverage should include both theft and vandalism as standard protections.

Scheduled Items and Valuable Collections

Valuable collections-artwork, historical documents, rare books, musical instruments, or donated items of significant value-require specialized protection beyond standard contents coverage. These items need scheduled endorsements that list them individually with specific coverage limits and agreed values. An art nonprofit with a $50,000 painting cannot rely on a standard contents limit of $25,000 per item. Instead, you schedule the painting separately at its appraised value. This approach eliminates depreciation arguments and ensures full recovery if loss occurs.

Walk through your facilities and document every owned asset, capturing replacement costs rather than current book values. Create a detailed inventory spreadsheet organized by location and category. Include acquisition dates, condition, and current replacement cost for high-value items. This inventory becomes your roadmap for coverage decisions and your defense during claim investigations. With your asset list in hand, you’re ready to evaluate which coverage types align with your nonprofit’s actual operations and risk profile.

How to Cut Nonprofit Property Insurance Costs Without Cutting Coverage

Bundle Coverage Types for Immediate Savings

Nonprofits save money when they combine different coverage types under one policy. A Business Owner’s Policy, or BOP, merges general liability, commercial property, and business income coverage into a single package. The Hartford data shows nonprofit customers using a BOP pay roughly $70 per month on average, or about $836 annually, though costs vary by organization size, location, staffing, and coverage limits. That bundled approach costs considerably less than purchasing each coverage type separately from different carriers. When you request quotes, ask carriers whether they offer nonprofit-specific BOPs with volume discounts for combining property, liability, and business income. Some carriers reduce rates by 10 to 20 percent when you consolidate coverage, and that savings compounds annually. Layering additional coverages like commercial auto, cyber liability, or sexual abuse and molestation insurance onto an existing policy typically costs less than standalone policies. An insurance professional who understands nonprofit operations can identify which coverages genuinely reduce your total cost of risk rather than simply adding premium.

Invest in Property Maintenance and Risk Assessment

Risk mitigation lowers your insurance costs because carriers reward organizations that prevent losses. Conduct a formal property risk assessment at least annually, documenting the condition of your building’s roof, HVAC systems, electrical wiring, plumbing, and fire suppression equipment. Deferred maintenance transforms small issues into catastrophic losses and signals poor governance to underwriters. Many nonprofits underestimate property coverage by insuring buildings at depreciated value rather than replacement cost, meaning after a fire they receive far less than needed to rebuild. A nonprofit that invests $5,000 in roof repairs and HVAC maintenance often qualifies for lower premiums than one that postpones these investments and files claims later. Document every safety improvement with photos and maintenance records because underwriters scrutinize these details during renewal.

Strengthen Physical Security and Governance

Implement theft and vandalism prevention measures like improved lighting, security cameras, alarm systems, and controlled access to high-value storage areas. These physical controls reduce claim frequency and demonstrate organizational competence to insurers. Nonprofits with strong governance practices-including written risk management policies, staff training on asset protection, and clear vendor liability terms in contracts-attract better rates and coverage terms from specialized carriers. Work with an insurance agency experienced in nonprofits to leverage insurer risk advisory and claims advocacy services that lower your total cost of risk rather than simply transferring premium from one carrier to another.

Final Thoughts

Nonprofit property coverage protects the physical assets that enable your organization to serve its community. Without it, a single fire, theft, or weather event can force program cuts, staff layoffs, or worse. The organizations that thrive after loss are those that invested in proper coverage before disaster struck.

Your nonprofit holds assets worth far more than standard commercial policies protect-sound equipment, vehicles, computers, inventory, and specialized materials represent years of donor investment and organizational capacity. When you document these assets accurately and match coverage limits to replacement costs, you eliminate the gap between what you own and what your policy actually covers. Building coverage protects your physical structure, contents and equipment coverage protects what’s inside, and business income coverage protects your ability to pay staff and rent while operations resume.

Start by walking through your facilities and documenting every asset with current replacement values, then request quotes from multiple carriers who understand nonprofit operations. We at Heaton Bennett Insurance work with multiple carriers to tailor nonprofit property coverage that fits your mission and budget. Contact us to evaluate your current coverage and identify gaps before loss occurs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.