Professional Liability Insurance for Consultants A Must-Have

Consulting businesses face mounting liability risks as client expectations rise and regulatory scrutiny intensifies. Professional liability insurance for consultants has become essential protection against costly lawsuits and claims.

We at Heaton Bennett Insurance see consultants paying devastating amounts for uninsured errors and omissions claims. The right coverage protects your reputation and financial stability when clients challenge your professional advice.

What Professional Liability Insurance Covers for Consultants

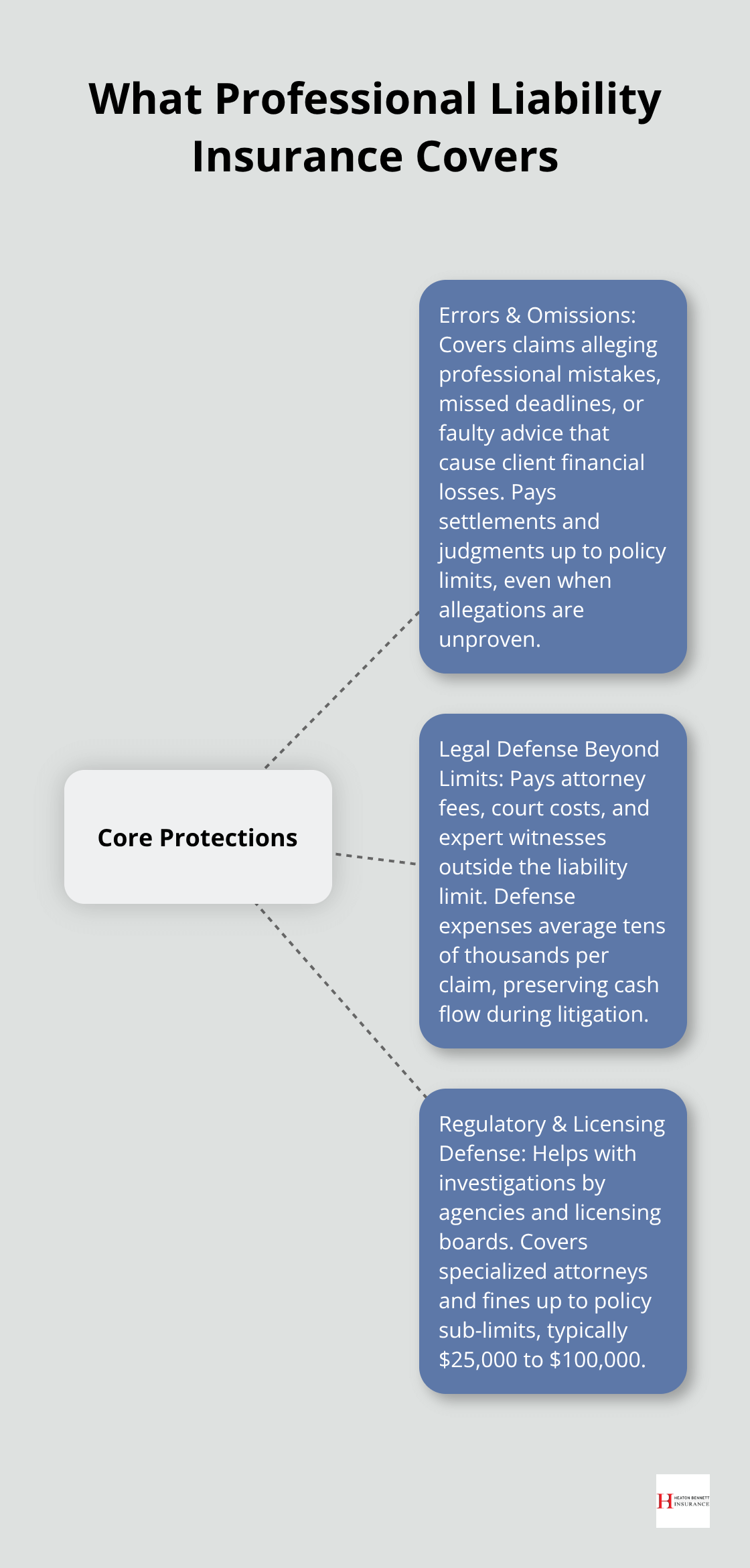

Professional liability insurance shields consultants from three major financial threats that destroy businesses within months. The coverage handles errors and omissions claims when clients suffer losses from your advice or services, with standard policies covering settlements and judgments up to your policy limits. Most consultants select coverage between $1 million and $2 million per occurrence, though technology and healthcare consultants often require higher limits due to greater exposure risks.

Errors and Omissions Protection That Saves Businesses

The insurance protects against claims of professional negligence, missed deadlines, and faulty advice that cause client financial losses. When a marketing consultant’s campaign strategy fails to deliver promised results, this coverage pays for resulting lawsuits and damages. IT consultants face protection when software recommendations create security vulnerabilities or system failures. The coverage applies regardless of whether you actually made an error-it protects against allegations of professional mistakes that clients believe caused their losses.

Legal Defense Coverage Beyond Policy Limits

The insurance covers all legal defense expenses, including attorney fees, court costs, and expert witness fees, even when claims prove baseless. According to The Hartford, defense costs alone average $75,000 to $150,000 per claim, regardless of outcome. This coverage operates outside your policy limits (meaning a $1 million policy still provides full defense cost coverage on top of the limit). Consultants spend their entire business savings on legal fees within months of receiving lawsuit papers without this protection.

Regulatory Investigation and Licensing Defense

Professional liability policies now include regulatory investigation coverage, protecting consultants when government agencies or licensing boards investigate their work. This coverage pays for attorneys who specialize in regulatory defense and covers fines up to policy sub-limits, typically $25,000 to $100,000. Management consultants face increased scrutiny from labor departments, while IT consultants deal with data protection investigations. The coverage extends to licensing board proceedings that could suspend or revoke professional credentials.

These comprehensive protections become even more valuable when you consider the specific risks that consultants face in today’s litigious business environment.

Why Consultants Face Catastrophic Losses Without Professional Liability Coverage

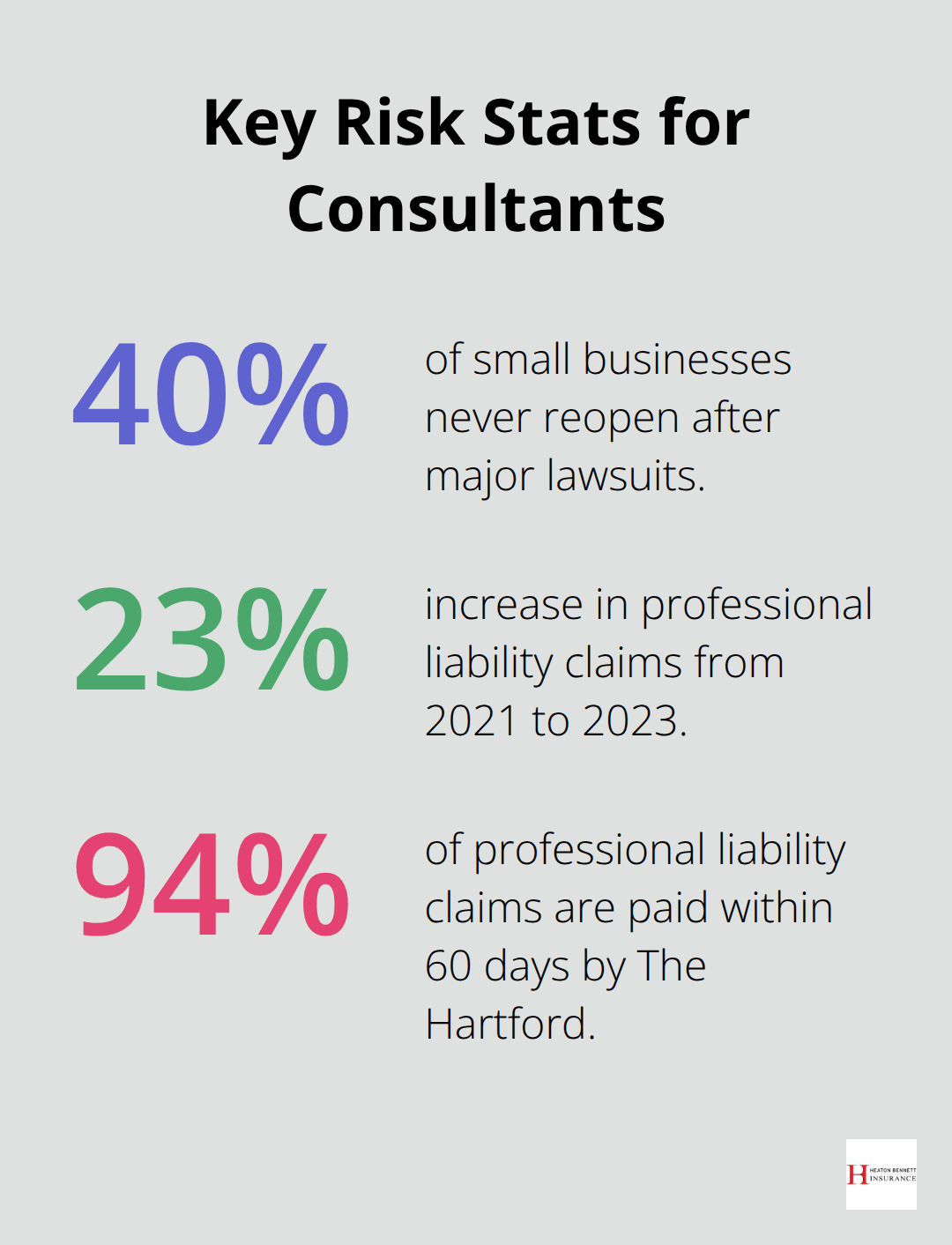

Consultants who operate without professional liability insurance face financial ruin from claims that average $43,000 according to industry data, with 40% of small businesses never reopening after major lawsuits. Client expectations have shifted dramatically since 2020, with businesses now holding consultants responsible for implementation failures, market changes, and even third-party vendor issues beyond the consultant’s direct control. Management consultants face the highest claim frequency, with 1 in 8 receiving formal complaints annually, while IT consultants deal with the most expensive claims that average $127,000 per incident when data breaches or system failures occur.

Client Demands Create Unlimited Liability Exposure

Modern clients demand guarantees that consultants cannot realistically provide, which creates dangerous liability gaps that destroy businesses overnight. Marketing consultants now face lawsuits when campaigns fail to generate promised ROI, despite market conditions that change after strategy development. HR consultants get sued for discrimination claims that stem from hiring recommendations made months earlier. The Allied Market Research data shows professional liability claims increased 23% from 2021 to 2023, with settlement amounts that grow faster than inflation rates. Clients increasingly view consultants as insurance policies for their business decisions rather than advisory service providers.

Technology Consultants Face the Steepest Financial Exposure

Technology consultants encounter the most severe financial threats, with cybersecurity incidents that generate average claims of $847,000 when client data gets compromised through recommended systems or processes. These claims often exceed the personal assets of most consulting firms (particularly solo practitioners and small partnerships). Healthcare consulting claims average $234,000 due to regulatory compliance failures, while financial consulting errors result in median settlements of $156,000 according to recent carrier surveys. The financial impact extends beyond immediate settlements to include reputation damage that destroys future business opportunities.

Long-Tail Claims Create Years of Financial Uncertainty

Construction and engineering consultants deal with the longest-tail claims, often facing lawsuits 3-5 years after project completion when structural issues emerge or environmental problems surface. These delayed claims catch consultants off-guard when they lack adequate liability coverage or have switched carriers without proper tail coverage. Professional liability claims can surface up to six years after service delivery in some states, which means consultants face ongoing exposure long after completing projects and receiving final payments.

These mounting risks make the selection of appropriate professional liability coverage more complex than many consultants realize, requiring careful consideration of multiple policy features and carrier capabilities.

Key Factors When Choosing Professional Liability Insurance

Professional liability insurance selection demands specific decisions about coverage limits, deductibles, and carrier capabilities that directly impact your financial protection when claims arise. Most consultants make costly mistakes by choosing inadequate limits or working with carriers that deny legitimate claims, which leaves them exposed to the same financial devastation they sought to avoid.

Coverage Limits Must Match Your Actual Exposure Risk

Standard $1 million per occurrence limits fall dangerously short for most consulting practices, particularly when technology errors or data breaches generate claims that average $847,000 according to recent carrier data. IT consultants need minimum $2 million limits, while management consultants who handle major corporate restructuring require $5 million coverage due to the scale of potential client losses. Healthcare consultants face regulatory fines that can reach $1.7 million per HIPAA violation, which makes $3 million limits the practical minimum. Aggregate limits should equal at least double your per-occurrence coverage since multiple claims often cluster together when market conditions deteriorate or when systematic errors affect multiple clients simultaneously.

Deductible Selection Balances Premium Costs Against Cash Flow Risk

Higher deductibles reduce premium costs but create dangerous cash flow problems when claims hit your business during slow revenue periods. Technology consultants benefit from $25,000 deductibles that cut premiums by 35% while they maintain manageable out-of-pocket exposure, but solo practitioners should limit deductibles to $10,000 maximum to avoid bankruptcy from defense costs alone. Management consultants who handle Fortune 500 clients can justify $50,000 deductibles due to higher fee structures, while newer consulting practices need $5,000 deductibles maximum since they lack sufficient cash reserves for larger exposures.

Carrier Financial Strength Determines Whether Claims Get Paid

Work exclusively with carriers rated A- or higher by AM Best, since lower-rated insurers often become insolvent when major claim cycles hit the industry. The Hartford maintains an A+ rating and pays 94% of professional liability claims within 60 days, while smaller regional carriers frequently delay payments for 6-12 months through unnecessary investigations. Claims processing speed matters because legal defense costs accumulate rapidly, and delayed reimbursements force consultants to drain business accounts or take expensive loans to cover attorney fees during litigation.

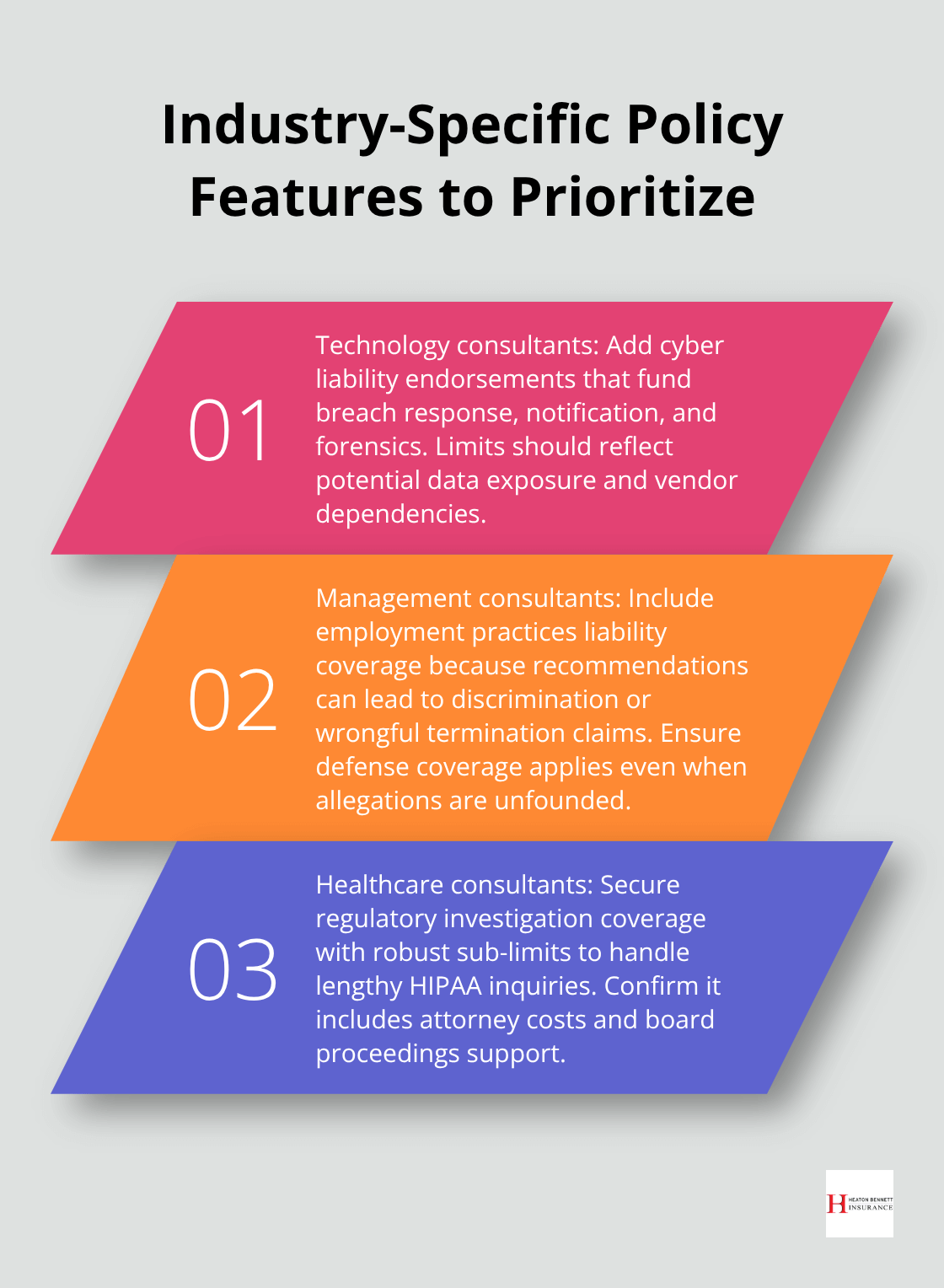

Policy Features That Address Industry-Specific Risks

Technology consultants need cyber liability endorsements that cover data breach response costs (averaging $4.45 million per incident according to IBM’s 2023 Cost of Data Breach Report). Management consultants require employment practices liability coverage since their recommendations often trigger discrimination lawsuits against client companies. Healthcare consultants must secure regulatory investigation coverage with minimum $100,000 sub-limits to handle HIPAA compliance investigations that can last 18 months.

These benefits create a foundation for smart plan selection, which requires careful evaluation of different insurance plan types and their specific features.

Final Thoughts

Professional liability insurance for consultants shifts from optional expense to business survival necessity when you face the financial devastation that uninsured claims create. This coverage transfers catastrophic financial exposure to insurance carriers while it protects your business reputation through professional claims handling and legal defense coordination. The protection provides immediate risk management benefits that preserve your consulting practice when disputes arise.

The long-term financial protection value extends far beyond claim payments to maintain client relationships during disputes and preserve business credit ratings when lawsuits surface. Consultants with proper coverage avoid personal bankruptcy from defense costs (which average $75,000 to $150,000 per incident according to The Hartford). Corporate clients now require proof of coverage before they sign consulting agreements, which makes the insurance essential for business development.

Appropriate coverage requires work with experienced independent agents who understand consulting industry risks and can access multiple carrier options. We at Heaton Bennett Insurance provide tailored insurance solutions that help consultants navigate complex coverage decisions. Request quotes from multiple carriers, compare coverage features beyond premium costs, and select policies that address your specific consulting discipline risks.