Nonprofit Insurance Needs: Aligning Coverages With Your Mission

Nonprofits operate under constant pressure to do more with less, which makes nonprofit insurance needs often overlooked until a crisis hits. The right coverage protects your organization, your board, and your ability to serve your community.

At Heaton Bennett Insurance, we’ve seen firsthand how the wrong insurance gaps can derail a nonprofit’s mission. This guide walks you through the coverages that actually matter for your organization.

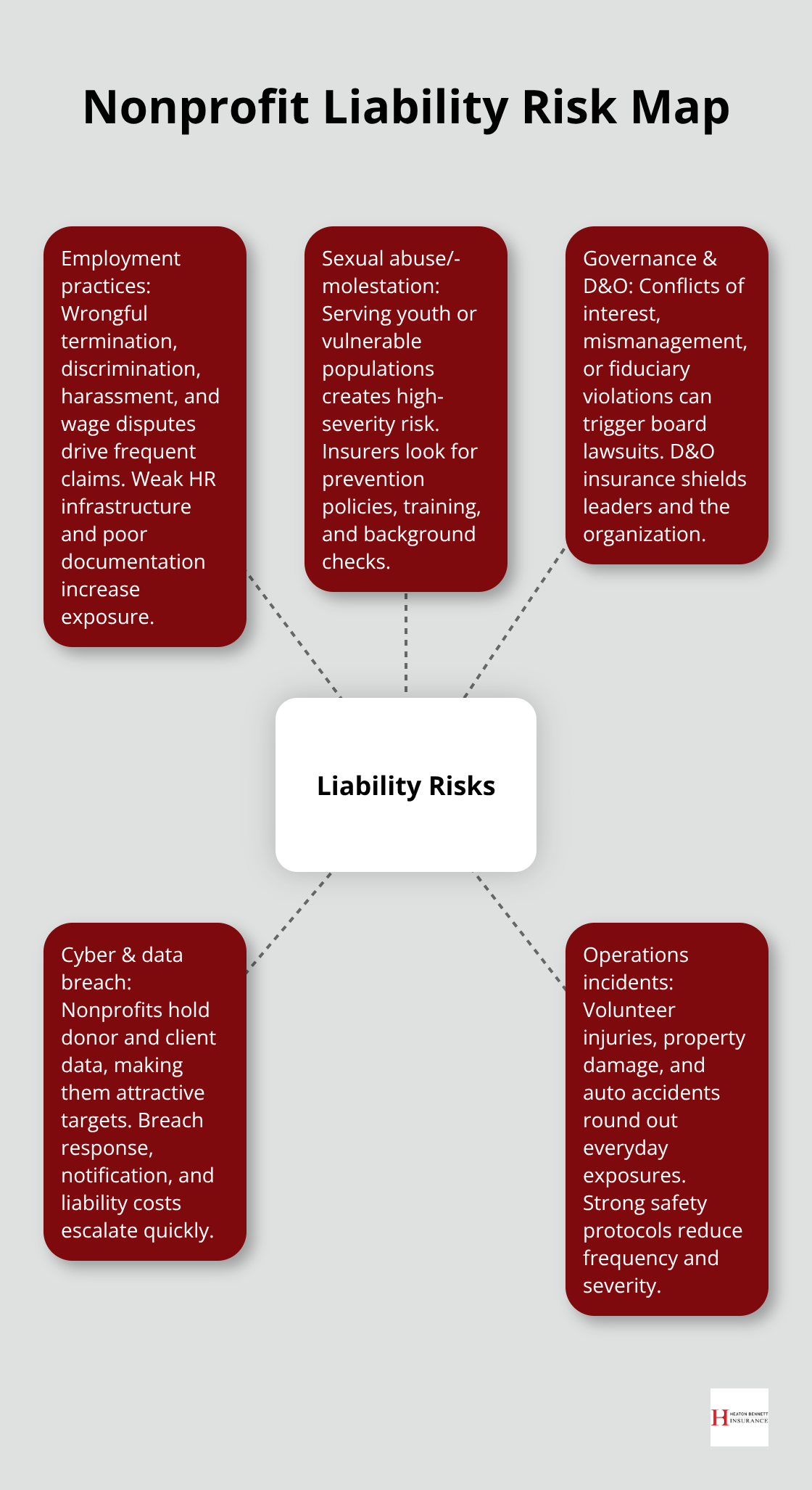

What Liability Risks Actually Threaten Your Nonprofit

Employment Practices Liability Demands Immediate Attention

Nonprofits face employment liability exposures that for-profit businesses rarely encounter. The Alera Group’s 2023 Property and Casualty Market Outlook found that harassment, wrongful termination, and wage disputes are increasingly common and costly for nonprofit employers. Underwriters now scrutinize hiring procedures, personnel documentation, and termination processes more closely than ever before. Most nonprofits lack the HR infrastructure that larger employers maintain, making wrongful termination and discrimination claims more likely. Without proper documentation of hiring decisions, performance management, and termination procedures, a nonprofit becomes an easy target for employment claims.

Employment practices liability insurance has become essential because it protects your organization when these situations arise.

Sexual Abuse Coverage Faces Rising Costs and Restrictions

Sexual abuse and molestation coverage has become harder to obtain at affordable rates, particularly for organizations serving vulnerable populations. The size and severity of abuse verdicts has risen dramatically-the Boy Scouts of America settlement illustrates how a single claim can threaten an organization’s financial stability and reputation. If your nonprofit works with youth or vulnerable populations, this risk demands immediate attention. The Philadelphia Insurance Companies emphasizes that organizations serving vulnerable populations need a documented child sexual abuse prevention program with leadership support, written policies, employee and volunteer training, and thorough background checks. Insurance underwriters now evaluate whether these safeguards exist before pricing coverage.

Governance, Data Breaches, and Operational Exposures

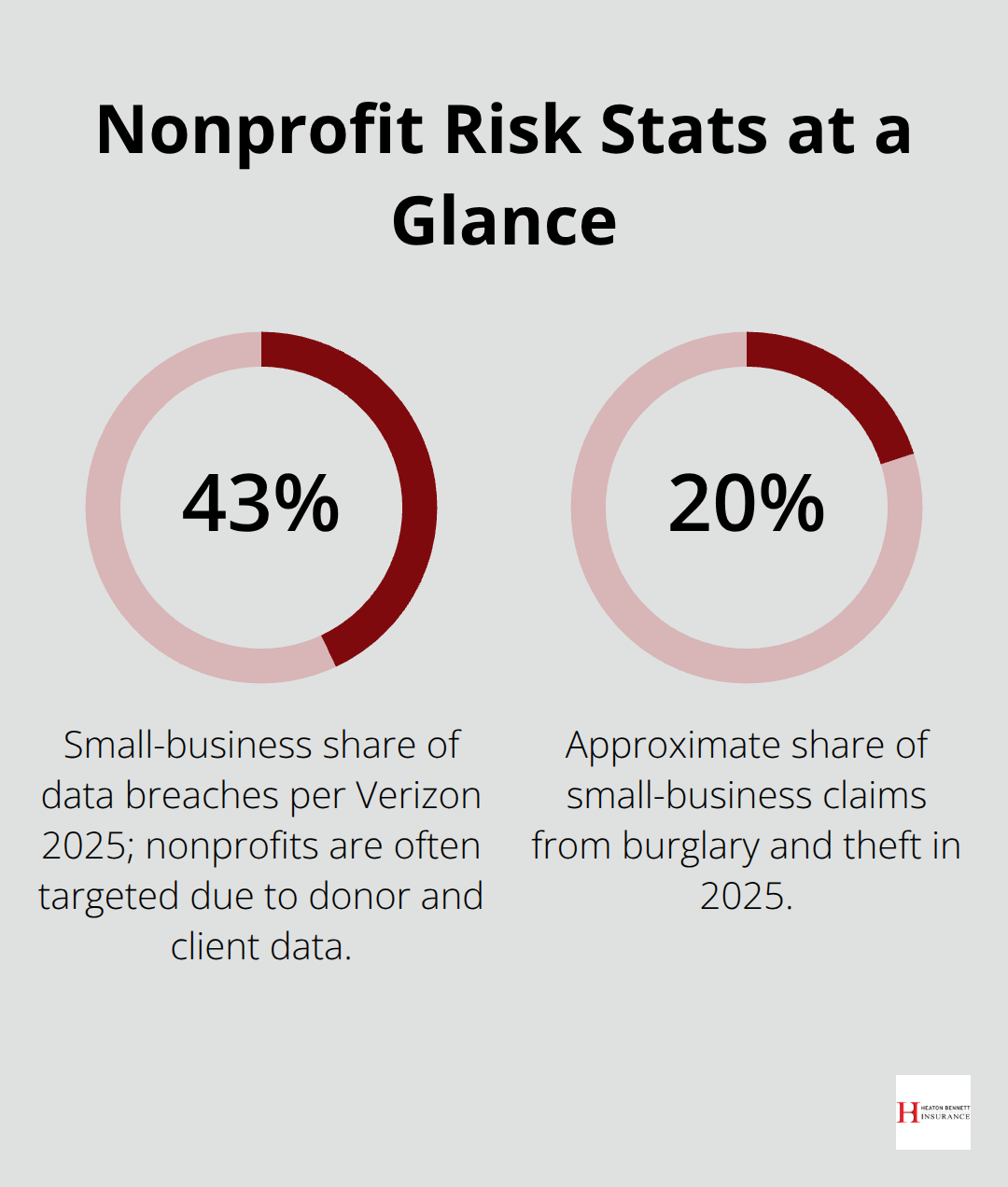

Governance and compliance failures create significant exposure. Mismanagement of funds, self-dealing, conflicts of interest, and tax-exempt status violations trigger board liability claims that directors and officers insurance must cover. Data breaches represent another critical exposure-the Verizon 2025 Data Breach Investigations Report found that 43% of data breaches impacted small businesses, and nonprofits holding donor information, client records, and employee data are frequent cyberattack targets. Volunteer-related incidents, property damage claims, and auto accidents involving nonprofit vehicles round out the exposure landscape.

Compliance Obligations Shape Your Coverage Requirements

State laws, contracts with funding partners, and venue requirements often mandate specific insurance minimums. Many grant agreements require general liability with minimum limits of one million dollars or higher. Landlords frequently demand proof of coverage before allowing nonprofits to occupy space. Venue operators hosting nonprofit events require liability certificates before events proceed. Tax-exempt status itself carries compliance burdens-maintaining 501(c)(3) status requires proper governance documentation, conflict-of-interest policies, and financial controls that directors and officers insurance helps protect. These external requirements force nonprofits to build coverage around what stakeholders demand, not just what feels adequate internally.

Understanding these liability exposures and compliance obligations reveals why a one-size-fits-all insurance approach fails most nonprofits. The next section examines the specific coverages that address these risks and how to evaluate which ones matter most for your organization’s operations.

Core Coverages That Protect Mission and Assets

General Liability and Board Protection Form Your Foundation

General liability insurance forms the foundation of nonprofit protection, covering third-party claims for bodily injury, personal injury, or property damage that arise from your organization’s activities. Most grant agreements require minimum limits of one million dollars, and landlords or venue operators will demand proof before allowing your nonprofit to operate. General liability alone, however, leaves your board and executive leadership exposed. Directors and officers insurance protects board members and senior staff from personal liability when governance decisions go wrong. Mismanagement of funds, conflicts of interest, or alleged violations of fiduciary duty can trigger costly litigation. The Hartford estimates that a basic Business Owner’s Policy, which bundles general liability with property coverage, costs nonprofits around seventy dollars per month on average, though actual premiums vary significantly by industry, location, and employee count.

Property Coverage Shields Physical Assets From Loss

Commercial property insurance protects buildings, equipment, computers, and inventory your nonprofit owns or leases. Burglary and theft accounted for roughly twenty percent of small-business claims in 2025, making this protection essential for any organization with physical assets. A single theft or fire can halt operations and drain reserves that should support your mission. Property coverage helps your organization recover quickly and maintain continuity when disaster strikes.

Cyber Liability Addresses Data Breach Threats

Cyber liability has become equally critical for nonprofits. The Verizon 2025 Data Breach Investigations Report found that 43 percent of data breaches impacted small businesses, and nonprofits holding donor information, client records, and employee data are frequent targets. Cyber coverage helps your organization respond to breaches, cover notification costs, and manage liability from compromised data. Without this protection, a breach can expose your donors and clients while creating legal and financial exposure for your nonprofit.

Employment and Volunteer Liability Protects Against HR Claims

Volunteer and employment practices liability insurance protects against wrongful termination, discrimination, harassment, and wage disputes-exposures that plague nonprofits lacking formal HR infrastructure. Underwriters scrutinize hiring documentation, personnel files, and termination procedures closely because nonprofits often lack the procedural safeguards larger employers maintain, making claims more likely. These three coverage areas-general liability paired with directors and officers protection, property and cyber combined, and volunteer or employment practices liability-form the practical backbone of nonprofit insurance.

Evaluating Coverage Limits for Your Organization

A single incident can drain reserves, jeopardize mission funding, and expose individual leaders to personal liability. The question becomes not whether to purchase these coverages, but how to select limits and options that match your nonprofit’s specific operations. The next section walks you through assessing your organization’s unique risk profile and choosing coverages that align with your mission rather than following a generic template.

How to Match Coverage to Your Nonprofit’s Actual Operations

Start With an Honest Inventory of Your Activities

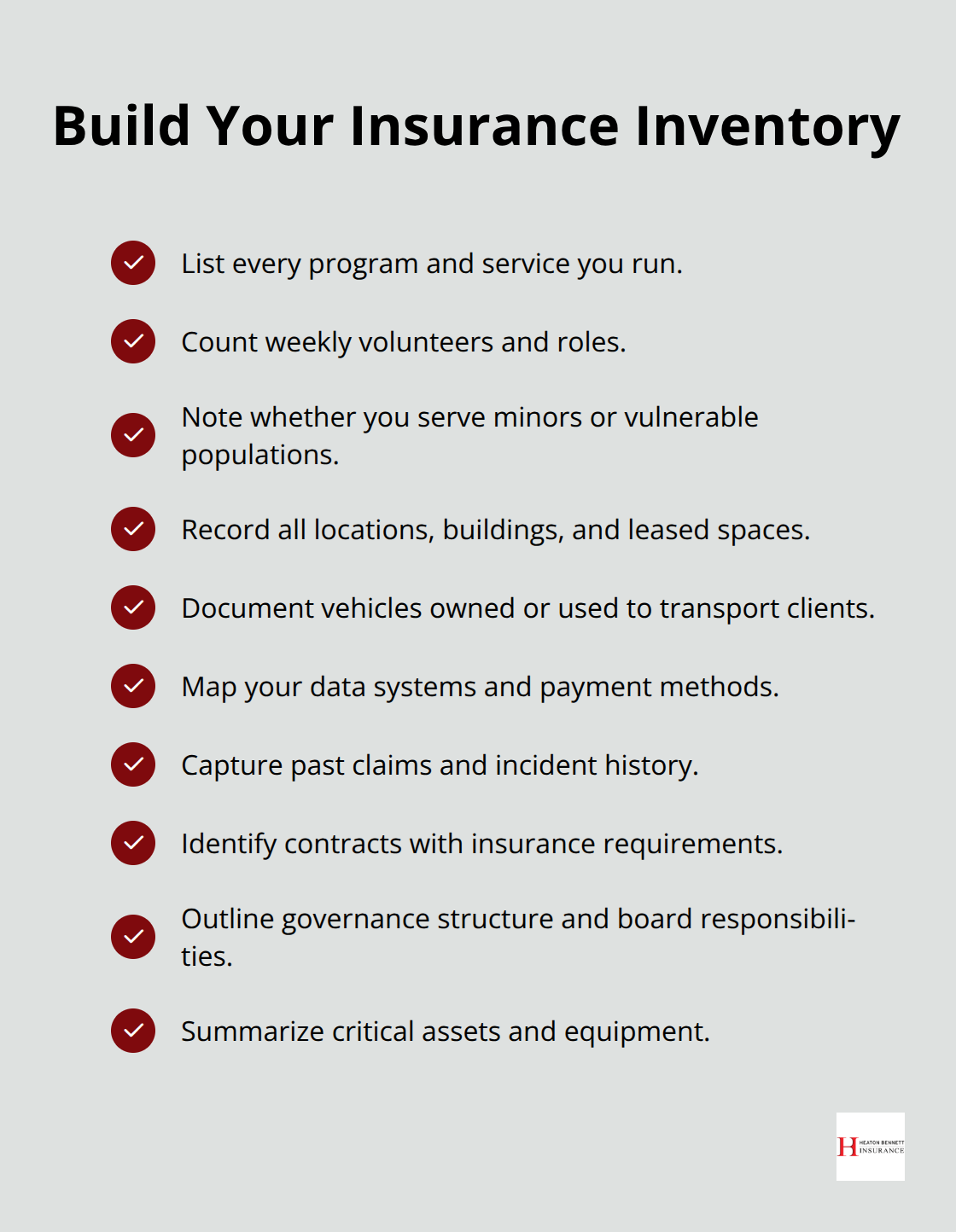

Your nonprofit’s operations differ fundamentally from other nonprofits, which means insurance decisions should start with mapping what you actually do, not what a generic template suggests. A youth mentoring organization faces different exposures than a food bank, which faces different risks than a community health clinic. The Alera Group’s 2023 Property and Casualty Market Outlook emphasizes that underwriters are drawn to organizations that can articulate a compelling mission and demonstrate strong risk controls and positive loss histories.

Your first step is conducting an honest assessment of your activities, the people you serve, the assets you own, and the liabilities embedded in your daily operations. Write down every program you run, every volunteer activity, every building you occupy, and every vehicle you operate. Include details like how many volunteers work each week, whether you serve minors or vulnerable populations, whether you transport clients, and what payment systems you use. This inventory becomes the foundation for selecting coverage limits and options that actually protect your mission rather than leaving dangerous gaps.

Understand Your Risk Profile Before Selecting Limits

Once you understand your exposures, cost management demands a different approach than simply shopping for the lowest premium. The Hartford estimates nonprofits pay roughly seventy dollars monthly for basic coverage, but actual costs vary dramatically based on your risk profile, geographic location, and the limits you select. Rather than cutting limits to reduce premiums, negotiate coverage options that fit your budget without sacrificing protection.

For example, increasing your general liability deductible from one thousand to five thousand dollars can lower premiums substantially while keeping limits intact for serious claims. Some nonprofits benefit from bundling coverages into a Business Owner’s Policy instead of purchasing separate policies, which often costs less than buying coverage piecemeal.

Avoid the False Savings of Underinsurance

The critical mistake is selecting coverage limits based on budget constraints alone. If your nonprofit operates in a state where juries award substantial damages, or if you serve vulnerable populations where abuse claims carry enormous verdicts, underinsuring creates false savings that evaporate the moment a claim arrives. A nonprofit-focused insurance partner understands these nuances and helps you prioritize coverages that matter most for your specific operations, then identifies cost efficiencies without compromising protection.

Partner With an Agency That Understands Nonprofits

Work with an agency that takes time to understand your programs, your governance structure, and your risk tolerance before recommending coverage rather than accepting generic quotes that treat your nonprofit like any other small business. An experienced partner asks detailed questions about your operations, your volunteer structure, and your service population before proposing solutions.

Final Thoughts

Nonprofit insurance needs vary dramatically based on your specific programs, the populations you serve, the assets you own, and your geographic location. General liability, directors and officers insurance, property protection, cyber liability, and employment practices coverage form the practical backbone that protects your organization, your board, and your mission when claims arrive. Without comprehensive protection, a single incident can drain reserves meant for programs, damage your reputation, and distract leadership from the work that matters.

Proper insurance lets your nonprofit focus on mission instead of worrying about financial catastrophe. When a volunteer gets injured, when a data breach exposes donor information, or when a governance dispute triggers litigation, comprehensive coverage absorbs the financial blow and keeps your organization moving forward. The right approach starts with understanding your actual operations, not accepting a one-size-fits-all quote that treats your nonprofit like any other small business.

At Heaton Bennett Insurance, we work with multiple carriers to build tailored coverage that matches your mission and your budget. We take time to understand your programs, your governance structure, and your risk profile before recommending solutions that address your nonprofit insurance needs. Connect with us today to build coverage aligned with your mission.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.