Nonprofit Fundraising Insurance: Coverage for Events and Campaigns

Nonprofit fundraising events carry real risks. From liability claims to property damage, one incident can derail your mission and drain resources you need for your cause.

At Heaton Bennett Insurance, we’ve seen how the right nonprofit fundraising insurance protects organizations when things go wrong. This guide walks you through the coverage options that matter most for your events and campaigns.

Real Risks That Drain Nonprofit Resources

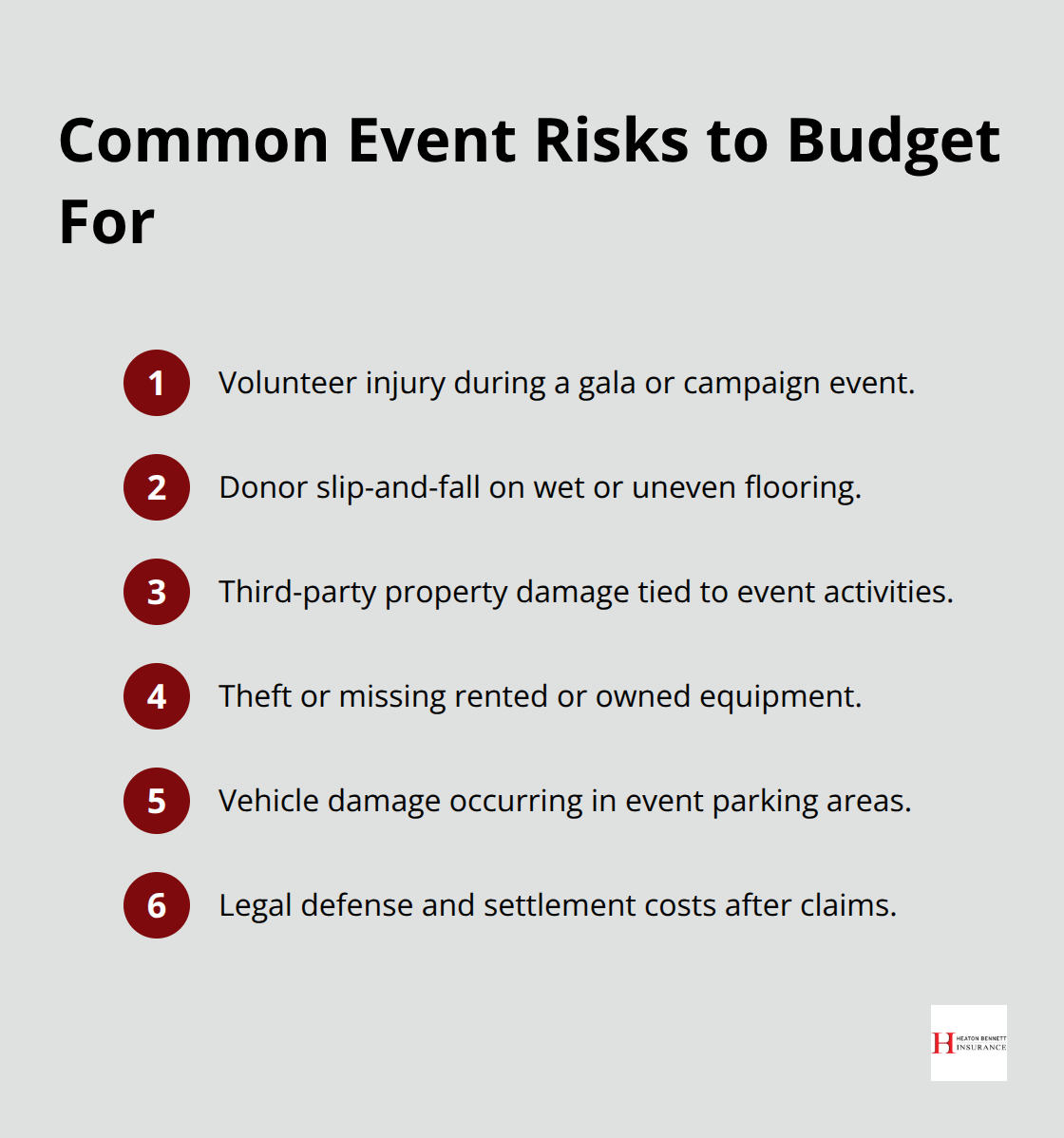

Liability claims hit nonprofits hard because they arrive without warning. A volunteer trips at your gala and breaks their arm. A donor slips on wet flooring during a campaign event. Suddenly you face medical bills, legal fees, and potential settlements that weren’t in your budget.

According to Giving USA 2023, Americans gave $557.16 billion to charity that year, with individuals contributing $374.40 billion. That scale of fundraising activity means thousands of nonprofits host events simultaneously, and statistically, accidents happen. High-profile cases underscore this reality: United Way faced a $12 million wrongful-termination suit, and the Minnesota Attorney General took action against ThinkTechAct Foundation for fund misuse and governance violations. These weren’t small organizations with deep pockets. Without event insurance, your nonprofit absorbs these costs directly, pulling money away from programs that serve your community.

Why Venues and Sponsors Demand Proof of Coverage

Venues require certificates of insurance before they confirm event dates. Sponsors demand additional insured status on your policy. Without proof of coverage, you lose the venue entirely, or worse, you scramble to reschedule weeks before your event. This isn’t theoretical friction-it’s a contractual blocker that derails your fundraising calendar. When you apply for event insurance, you receive a certificate of insurance that serves as proof of coverage, which you can provide immediately to venues and sponsors.

What Coverage Types Protect Your Nonprofit Events

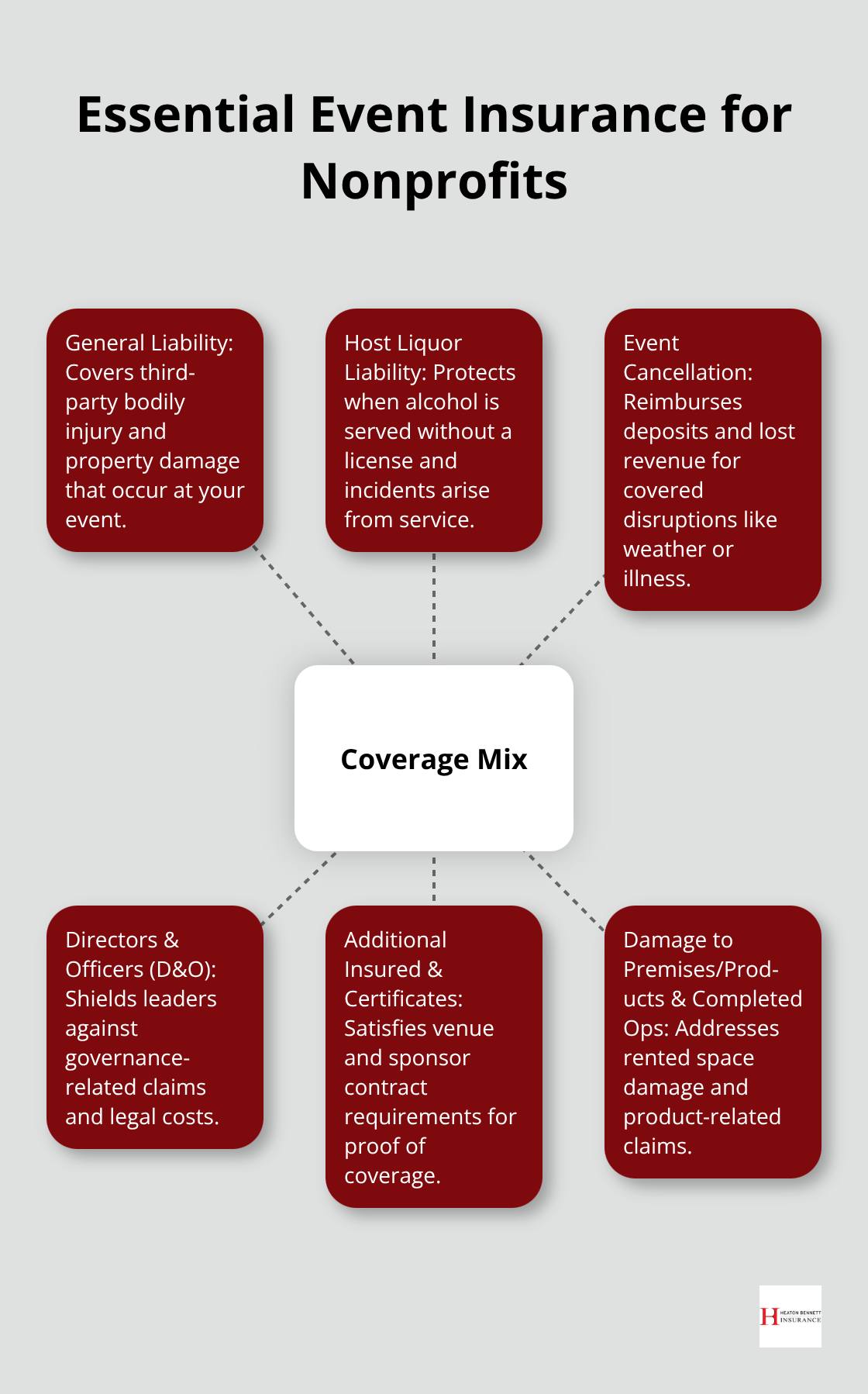

For nonprofit-friendly short-term event insurance, coverage typically includes general liability, bodily injury and property damage protection, personal and advertising injury, products and completed operations, damage to premises rented to you, and host liquor liability if alcohol is served without a license. If your nonprofit hosts a gala with 500 attendees, a concert fundraiser, or a banquet campaign, these coverage types protect you against the specific exposures of that event.

How Theft and Property Damage Expose Your Budget

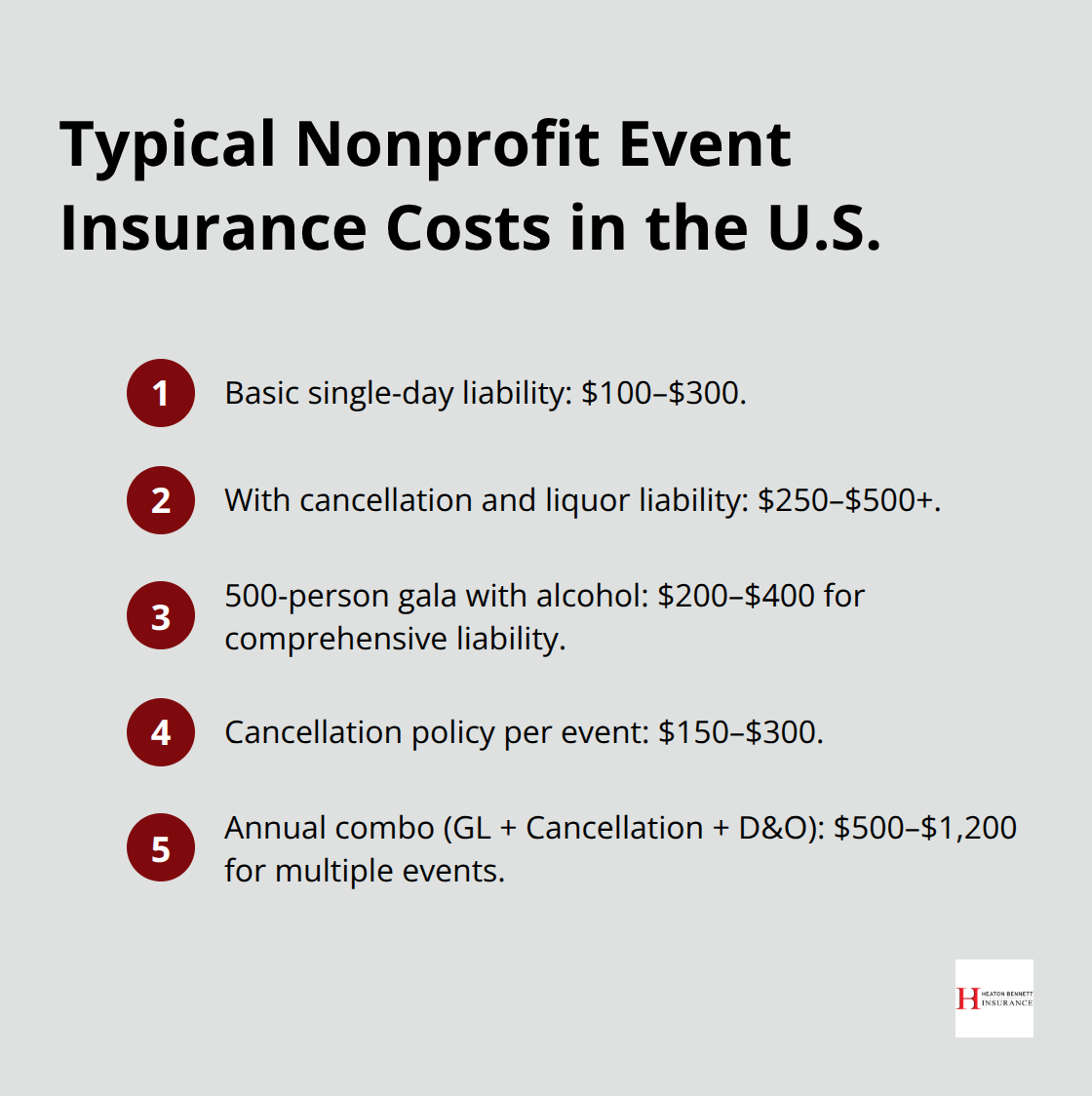

Theft and property damage occur at events regularly. Equipment goes missing, rented furniture gets damaged, or someone’s vehicle gets hit in your parking lot. General liability covers third-party property damage, but damage to items you’ve rented requires explicit coverage in your policy. The cost for a single-day event typically runs $100–$300 for basic liability, though prices climb with larger crowds, alcohol service, and additional insured requirements. For nonprofit budgeting, insurance should account for 1–3 percent of your event budget, which is far less expensive than recovering from an uninsured incident.

Understanding these risks prepares you to select the right coverage for your specific events and campaigns. The next section walks you through the insurance types that address each of these exposures.

Which Coverage Types Actually Protect Your Nonprofit Events

General Liability Forms Your Foundation

General liability insurance covers third-party bodily injury and property damage, but it does not cover everything that can go wrong at your fundraiser. When a donor trips during your gala and sues, general liability responds. When someone’s vehicle gets damaged in your parking lot, general liability pays. However, if a rented tent gets destroyed by wind or your event equipment goes missing, you need explicit coverage for damage to premises rented to you and products liability. The gap between what general liability covers and what actually happens at events is where nonprofits lose significant resources.

For a 500-person gala with alcohol service, you should expect to pay $200–$400 for comprehensive event liability that includes host liquor liability coverage. If your nonprofit requires additional insured status for venues and sponsors-which most do-the cost climbs slightly, but this protection is non-negotiable because contracts demand it and venues will not confirm dates without proof.

Event Cancellation Insurance Prevents Financial Collapse

Event cancellation insurance is where nonprofits make a critical mistake: they skip it entirely. You budget $15,000 for your annual fundraising gala, secure the venue, sell tickets, and three weeks before the event, a severe winter storm forces venue closure or a key speaker cancels due to illness. Without cancellation coverage, you lose ticket revenue and still owe the venue deposit. With cancellation insurance, you recover lost revenue and deposits.

According to NonProfit PRO’s 2026 trends analysis, December accounts for 17–33 percent of annual giving, meaning year-end events carry outsized financial weight. A single canceled holiday fundraiser can cost your organization $10,000 or more in lost revenue plus sunk expenses. Cancellation policies typically cost $150–$300 per event and cover weather, illness, power outages, and venue issues.

Directors and Officers Insurance Shields Your Leadership

Directors and officers insurance protects your board from personal liability when governance decisions go wrong-a wrongful-termination claim against a board member, a discrimination allegation tied to volunteer selection, or a fund misuse accusation. This coverage pays legal defense costs and settlements, protecting both your board and your nonprofit’s reserves.

When combined with employment practices liability insurance, D&O coverage shields your organization from the broad set of claims that arise from leadership decisions around events, campaigns, and staffing. The three-coverage combination of general liability, cancellation insurance, and D&O protection costs $500–$1,200 annually for most nonprofits hosting multiple events, far less than recovering from even one uninsured incident.

Building Your Coverage Strategy

The right insurance mix depends on your event size, activities, and risk profile. A small community fundraiser with 100 attendees and no alcohol requires different coverage than a large gala with 500 guests and a full bar. Your venue may demand specific coverage limits or additional insured status. Sponsors may require proof that their brand receives liability protection during the event. These contractual requirements shape your coverage decisions and affect your premium costs.

Understanding these three core coverage types positions you to assess your specific event risks and select the right limits for your nonprofit’s fundraising calendar.

Selecting the Right Coverage for Your Event

Document Your Event Details First

Start with your event details before comparing policies. You need to record the date, venue, expected attendance, activities, alcohol service, and whether you need additional insured status for the venue or sponsors. This information determines which coverage types you actually need and what price you’ll pay. A 100-person community fundraiser with no alcohol costs far less to insure than a 500-person gala with a full bar and live entertainment.

Insurance companies price based on specific risk factors, so vague applications lead to either overpriced quotes or gaps in coverage when claims arise. Once you have these details locked in, request quotes from insurers with nonprofit experience. According to industry data, basic single-day event liability runs $100–$300, while policies with cancellation coverage and liquor liability climb to $250–$500 or higher depending on guest count and activities.

Compare Premiums, Limits, and Exclusions

Most nonprofits budget 1–3 percent of total event costs for insurance, which is reasonable when you consider that a single uninsured incident can cost thousands. Compare not just premiums but also coverage limits, deductibles, and what each policy excludes. Some policies cap bodily injury at $300,000 while others offer $1 million.

Some exclude outdoor events or specific activities. Read the policy details carefully or work with an agent who understands nonprofit fundraising to translate the fine print into what actually matters for your event. The gap between what you think you have and what the policy actually covers can be substantial.

Meet Venue and Sponsor Requirements

Your venue and sponsors will dictate some coverage requirements, so confirm their demands early. Most venues require general liability with a minimum of $1 million in coverage and want your nonprofit named as the policyholder with the venue listed as additional insured. Sponsors often demand additional insured status as well, which costs slightly more but is non-negotiable because contracts won’t be signed without it.

If alcohol is served, verify that host liquor liability is included in your policy or purchased separately, and confirm that your bartender or caterer is also named as additional insured. Some states restrict host liquor liability availability, so check whether your state allows this coverage or requires different liquor liability terms.

Secure Proper Documentation and Timing

Once you identify all parties who need coverage, work with an insurance agent to ensure everyone is properly named on the certificate of insurance before you provide it to venues and sponsors. Starting the insurance process early-as soon as dates and venues are confirmed-gives you time to address any coverage gaps or contractual requirements without scrambling weeks before your event. This advance planning prevents delays and protects your fundraising calendar from last-minute cancellations due to missing insurance documentation.

Final Thoughts

Nonprofit fundraising insurance protects your mission by removing the financial burden of unexpected incidents at your events and campaigns. When a volunteer gets injured at your gala, when a storm forces you to cancel your annual fundraiser, or when a governance decision triggers a board liability claim, the right coverage absorbs costs that would otherwise drain resources from your programs. Without this protection, a single incident can set your organization back months or years.

Venues won’t confirm dates without proof of coverage, sponsors demand additional insured status, and your board faces personal liability if something goes wrong. Nonprofit fundraising insurance solves these problems simultaneously by satisfying contractual requirements, protecting your leadership, and providing financial stability when accidents happen. The cost remains modest relative to the protection-a comprehensive policy for a single event runs $200–$500, while annual coverage for multiple events typically costs $500–$1,200 (far less than recovering from an uninsured claim or losing a venue due to missing documentation).

We at Heaton Bennett Insurance work with nonprofits to build customized coverage that matches your specific events and campaigns. Contact us to discuss your nonprofit insurance needs and receive a personalized coverage plan that protects your mission.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.