Term Group Life Insurance A Smart Choice for Small Businesses?

Small businesses face tough decisions when choosing employee benefits that balance cost with value. Term group life insurance has emerged as a popular option, offering affordable coverage for entire teams.

We at Heaton Bennett Insurance see many business owners weighing this choice carefully. The question isn’t just about cost-it’s about finding the right fit for your company’s unique needs and employee expectations.

What Does Term Group Life Insurance Actually Cover

Term group life insurance pays a death benefit to employees’ beneficiaries when the insured person dies during the policy term. Most policies cover death from any cause, including illness, accidents, and natural causes, with some exclusions for suicide within the first two years.

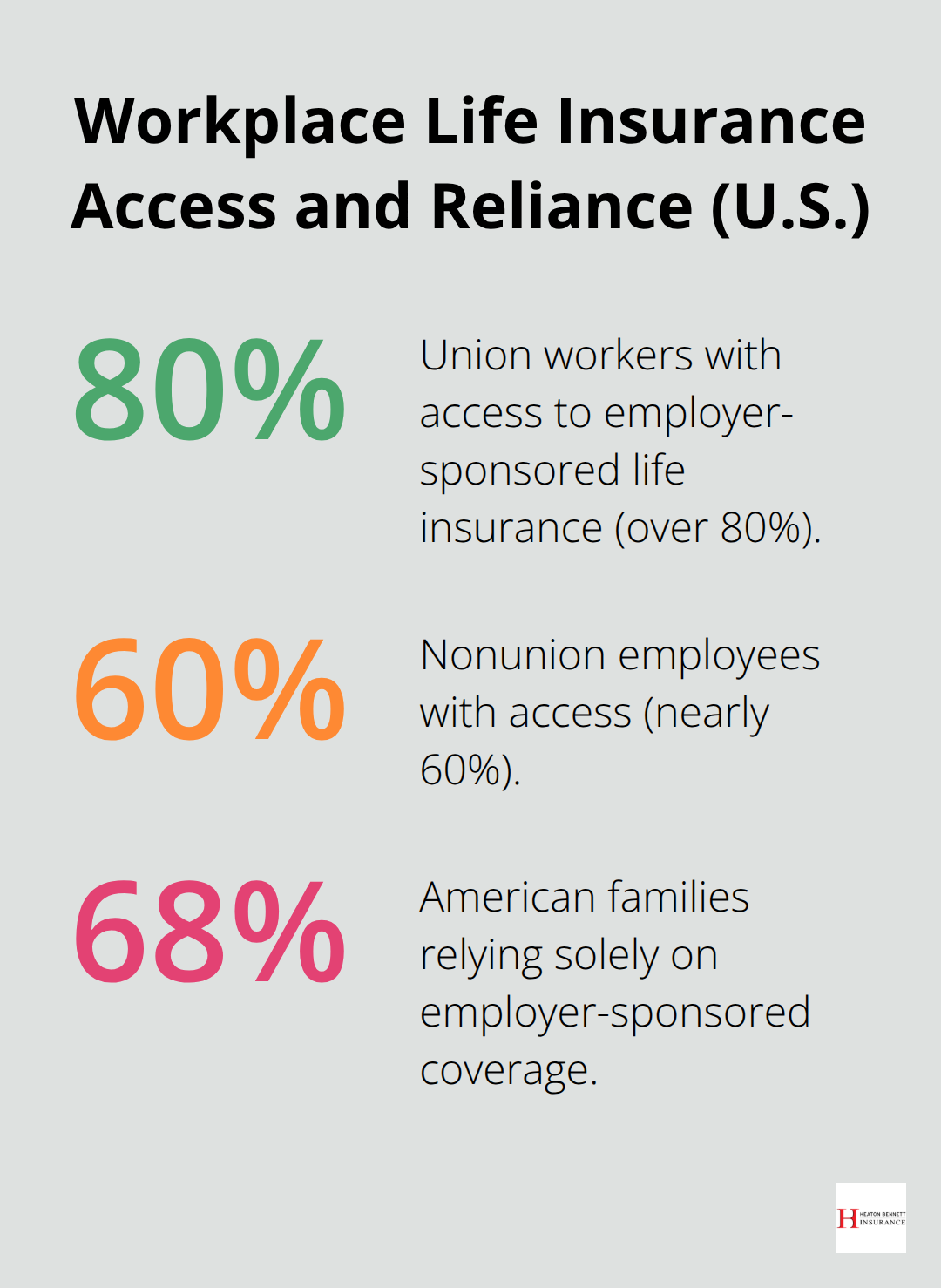

The Society for Human Resource Management reports that over 80% of union workers and nearly 60% of nonunion employees have access to employer-sponsored life insurance. Coverage amounts typically range from one to three times an employee’s annual salary, though the National Association of Insurance Commissioners found that 68% of American families rely solely on this often inadequate coverage.

How Group Policies Differ from Individual Coverage

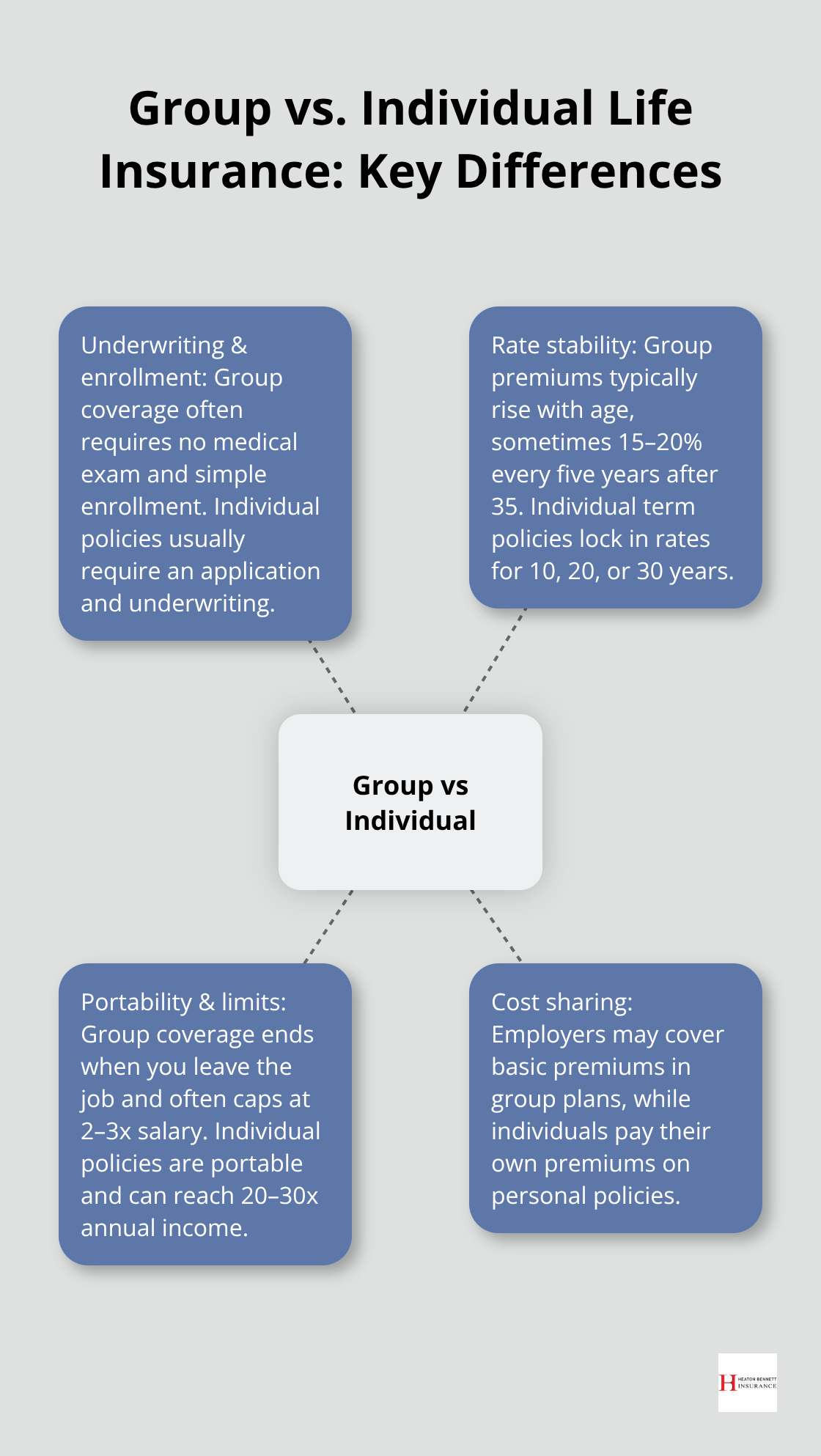

Group life insurance operates fundamentally differently from individual policies. Employees receive coverage without medical exams, but premiums increase with age rather than remain fixed. The Insurance Information Institute notes that group premiums can rise 15-20% every five years after age 35, while individual term policies lock in rates for 10, 20, or 30 years.

Group policies terminate when employees leave, which creates dangerous coverage gaps that COBRA continuation rarely addresses since it costs 102% of total premiums. Individual policies offer portability and higher coverage limits (reaching 20-30 times annual income) compared to group policies’ typical 2-3 times salary cap.

Standard Coverage Terms and Limitations

Most group term policies renew annually with employer-controlled terms and automatic enrollment. Coverage amounts rarely exceed $50,000 in employer-paid benefits due to IRS tax regulations, though employees can often purchase additional coverage through payroll deduction.

The average policy face value in the U.S. was $160,000 in 2015, far below the recommended 10-12 times annual income. Premium structures favor younger employees but become increasingly expensive for workers over 50, whose costs can triple compared to their younger colleagues.

These coverage limitations and cost structures directly impact how small businesses can use group term life insurance as a competitive advantage in their comprehensive employee benefits packages.

Why Term Group Life Insurance Benefits Small Businesses

Term group life insurance delivers immediate financial advantages that make it an exceptional choice for small businesses. A healthy 35-year-old employee can receive $1 million in coverage for approximately $40-60 monthly through individual policies, but group rates run 30% lower due to bulk purchase power. The U.S. Bureau of Labor Statistics shows that businesses can offer this benefit while employers often cover the entire premium cost for basic coverage, which creates essentially free money for employees.

Tax Benefits That Actually Matter

The IRS allows employers to provide up to $50,000 in group life insurance coverage completely tax-free to employees, which creates genuine value without additional tax burden. Employers deduct premium payments as business expenses, which reduces their taxable income while employees receive coverage without the need to report it as taxable compensation. This tax treatment makes group life insurance more valuable than equivalent salary increases, since employees would pay income tax on additional wages but receive the insurance benefit tax-free.

Administrative Simplicity Saves Time and Money

Group enrollment eliminates individual underwriting, medical exams, and complex application processes that drain administrative resources. Employees typically have 30-60 days after they start employment to enroll without health questions, and premiums integrate directly into payroll deduction systems. This streamlined approach contrasts sharply with individual policy management, where each employee would need separate applications, medical evaluations, and payment processing (which can take weeks to complete).

Cost Control Through Predictable Premiums

Small businesses gain budget predictability through group life insurance premium structures that remain stable for the entire group. Employers can forecast annual benefit costs more accurately compared to individual policies where each employee’s health status affects pricing. The bulk purchase approach also provides negotiation leverage with insurance carriers, particularly for businesses with 10 or more employees.

However, these advantages come with trade-offs that business owners must carefully consider before implementation.

What Are the Real Downsides of Group Term Life Insurance

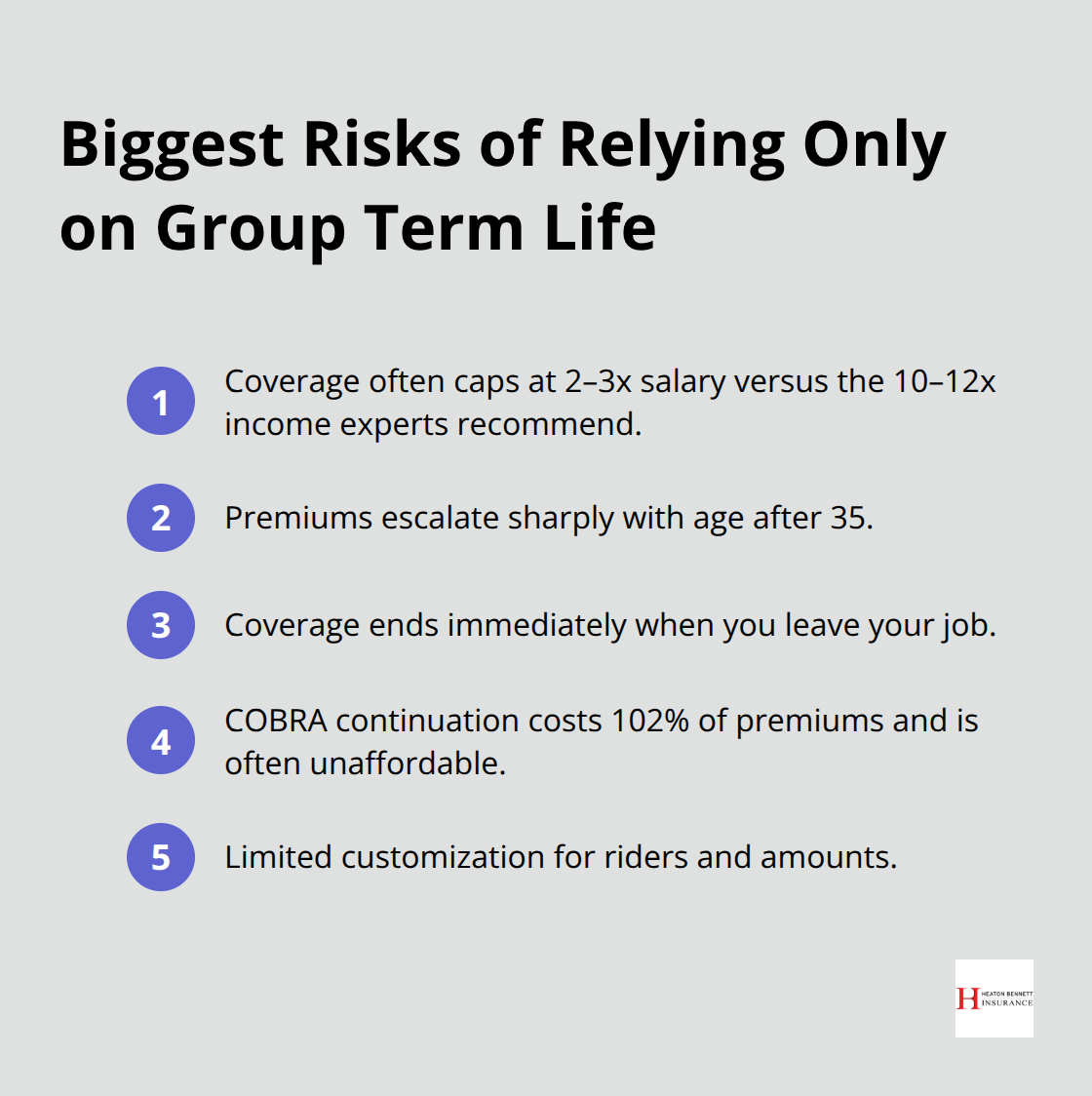

Group term life insurance creates significant coverage gaps that leave employees financially vulnerable. The National Association of Insurance Commissioners found that 68% of American families rely solely on group coverage, yet financial experts recommend 10-12 times annual income while group policies typically cap at 2-3 times salary.

A software engineer who earns $80,000 annually might receive only $160,000-$240,000 in group coverage, which falls $640,000 short of the recommended $800,000-$960,000 protection level. This shortfall becomes critical when mortgage payments, childcare costs, and education expenses demand substantial financial resources after a breadwinner’s death.

Premium Escalation Hits Older Workers Hard

Group life insurance premiums increase dramatically with age and create budget surprises that catch small businesses off guard. The Society for Human Resource Management reports that premiums for employees over 50 can triple compared to younger workers, while the Insurance Information Institute shows group premiums rise 15-20% every five years after age 35. A 45-year-old employee who paid $30 monthly for coverage might face $90 monthly premiums by age 55 (which makes continued participation financially impossible). These costs force businesses to either absorb massive premium increases or watch valuable experienced employees lose coverage when they need it most.

Job Changes Create Dangerous Coverage Gaps

Employees lose all group life insurance protection the moment they leave their job, which creates potentially devastating coverage gaps during career transitions. COBRA continuation costs 102% of total premiums and makes it unaffordable for most people between jobs, and approximately 99% of term policies never pay claims due to lapses or terminations. Workers who change jobs face weeks or months without protection while they secure new employment or navigate individual policy applications that require medical exams and underwriting delays. This vulnerability particularly affects employees with health conditions who may struggle to qualify for individual coverage after they lose group benefits.

Limited Customization Options

Group policies restrict employee choice and prevent workers from tailoring coverage to their specific needs. Employers control all policy terms, benefit amounts, and rider options (such as accidental death coverage or disability waivers). Employees cannot adjust their coverage based on life changes like marriage, home purchases, or children without employer approval. This inflexibility contrasts sharply with individual policies that allow workers to modify coverage amounts, add riders, and update beneficiaries without workplace restrictions.

Final Thoughts

Term group life insurance serves small businesses with younger workforces who need basic coverage at minimal cost. Companies with employees under 35 and limited benefit budgets can provide meaningful protection while they keep expenses predictable. The tax advantages and simplified administration make it particularly attractive for businesses with 10-50 employees who want to compete for talent without complex benefit management.

Businesses with older employees or those who seek comprehensive coverage should consider supplemental options. The premium increases after age 35 and coverage gaps during job transitions create real financial risks that demand attention. Term group policies alone often fall short of the 10-12 times annual income that financial experts recommend.

We at Heaton Bennett Insurance recommend that you evaluate your workforce demographics and long-term benefit strategy before you commit to term group coverage alone (many successful small businesses combine basic group coverage with voluntary individual policy options). This approach gives employees choice while it controls costs. Ready to explore group life insurance options for your business? Contact our team to discuss how term group policies fit into your overall employee benefits strategy and compare multiple carrier options tailored to your specific needs.