Cyber Liability Insurance Safeguarding Your Digital Assets

Cyber attacks cost businesses an average of $4.45 million per incident in 2023, according to IBM’s Cost of a Data Breach Report. Small and medium enterprises face even greater risks, with 60% closing within six months of a major breach.

We at Heaton Bennett Insurance understand that cyber insurance has become essential protection for modern businesses. The right policy can mean the difference between recovery and bankruptcy when digital threats strike.

What Does Cyber Liability Insurance Actually Cover?

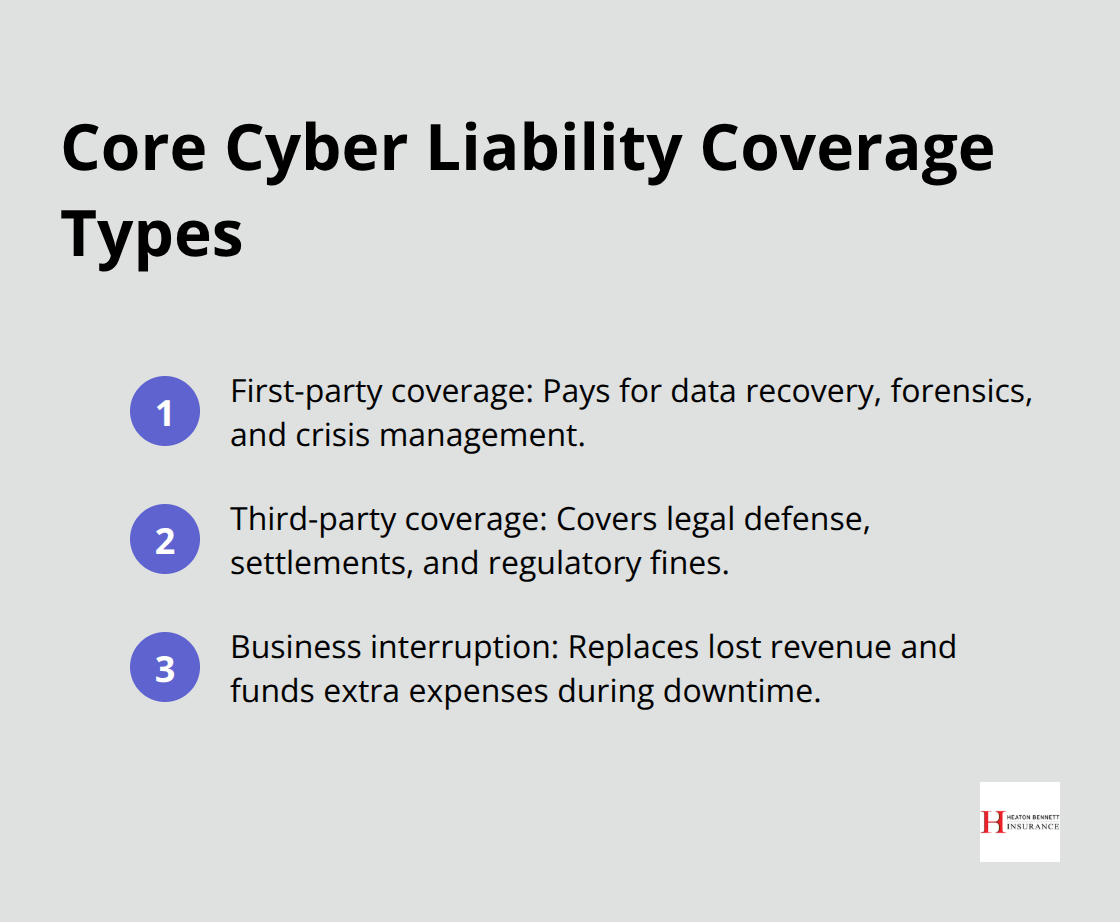

First-Party Protection for Your Direct Losses

First-party coverage protects your business from direct financial losses when cyber incidents hit your systems. This protection covers data recovery costs, which averaged $1.76 million per incident according to IBM’s 2024 report. Your policy pays for forensic investigations to determine how attackers breached your systems, plus the costs of specialists who restore corrupted files and rebuild damaged networks.

Crisis management expenses fall under this coverage, including public relations firms that manage your reputation after a breach. Many policies include credit monitoring services for affected customers (which can cost $50-200 per person annually). The policy also covers notification costs when you must inform customers about compromised data.

Third-Party Claims Protection

Third-party coverage handles lawsuits from customers, vendors, or partners whose data you compromised. Legal defense costs alone can reach $500,000 before any settlement, with regulatory fines that add another layer of expense. The healthcare sector faces particularly steep penalties, with HIPAA violations that cost up to $1.5 million per incident.

This coverage protects against privacy violations, copyright infringement claims, and defamation lawsuits that stem from cyber incidents. Your insurer defends these claims and pays settlements or judgments up to your policy limits.

Business Interruption Coverage

Business interruption protection compensates for lost revenue during system downtime, which affects 95% of cyber incidents according to Ponemon Institute research. This coverage calculates your daily revenue and pays for each day your operations remain offline (typically covering 30-365 days depending on your policy limits).

Manufacturing companies lose an average of $50,000 per hour during ransomware attacks. The coverage also pays for extra expenses you incur to minimize downtime, such as renting temporary equipment or outsourcing critical functions. These comprehensive protections address the most common cyber threats that target businesses across all industries.

What Cyber Threats Target Your Business Daily?

Ransomware Dominates Business Attacks

Ransomware attacks increased 25% in 2024 despite law enforcement actions against major groups, according to cybersecurity firm reports. Manufacturing companies face the highest risk and account for 25.7% of cyber incidents with ransomware involvement in 71% of those cases (based on World Economic Forum data). Healthcare organizations see 21.82% of cyber incidents while hospitality follows at 19.57%.

Attackers typically demand payments between $200,000 and $2 million from mid-sized businesses. The FBI strongly advises against payment since only 65% of companies recover their data even after ransom payment. Instead, maintain offline backups with 24-hour updates and test recovery procedures monthly. Multi-factor authentication blocks 99.9% of automated attacks according to Microsoft security research.

Social Engineering Exploits Human Weakness

Business Email Compromise scams caused $55 billion in losses over the past decade and represent the costliest cyber threat that organizations face. These attacks target finance departments with fake vendor invoices or executive impersonation requests for wire transfers. The average BEC loss reaches $125,000 per incident according to FBI data.

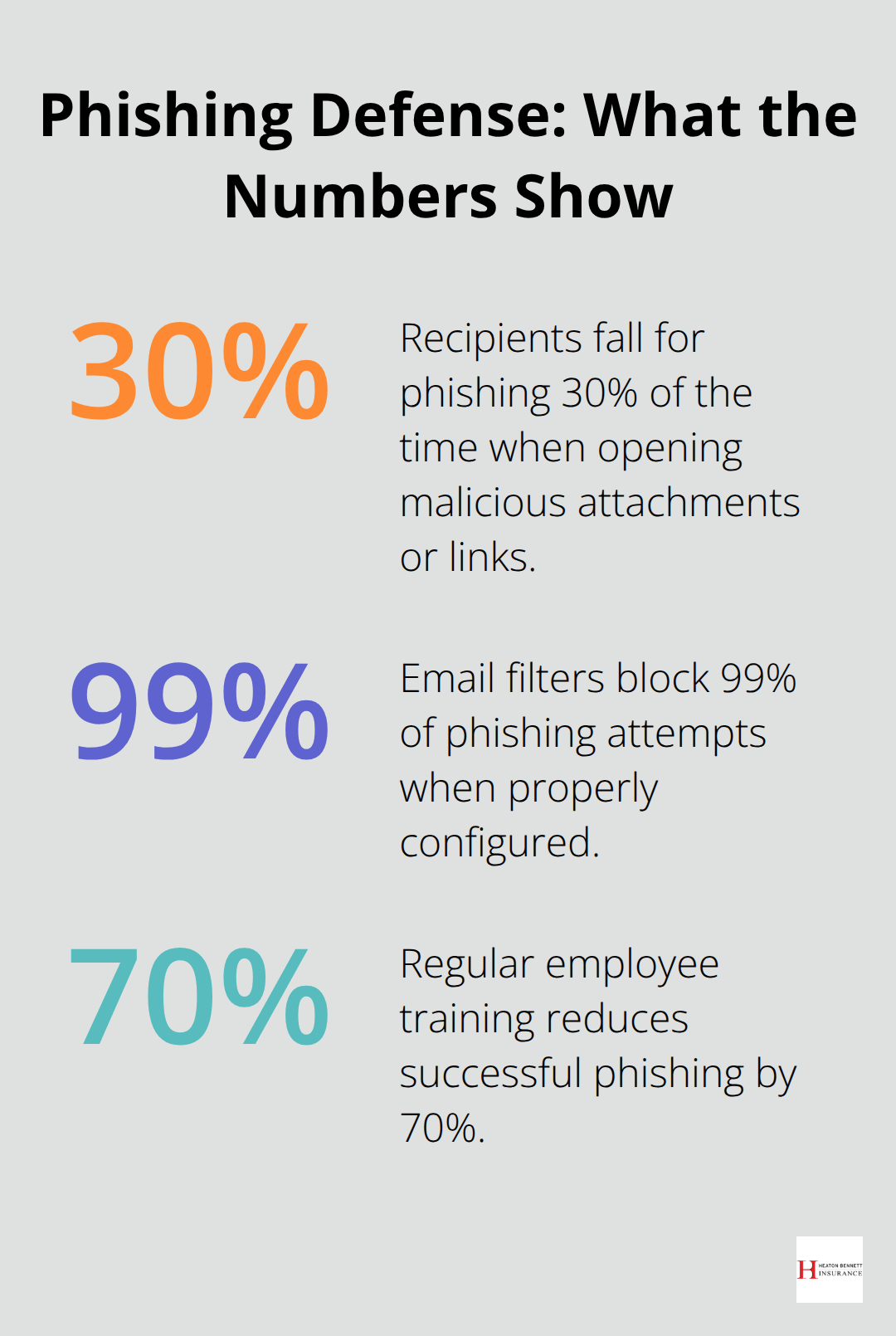

Train employees to verify payment requests through separate communication channels and implement dual approval processes for transfers that exceed $10,000. Phishing emails successfully deceive 30% of recipients who open malicious attachments or click dangerous links. Deploy email filters that block 99% of phishing attempts and conduct monthly simulated attacks to test employee awareness. Companies with regular training programs reduce successful phishing by 70% compared to untrained staff.

Data Breaches Strike Without Warning

Data breaches affect 83% of organizations annually and cost an average of $4.88 million per incident in 2024. Hackers target customer databases, financial records, and intellectual property through vulnerable network entry points. Healthcare data commands premium prices on dark web markets ($250 per record versus $5 for credit card information).

Most breaches stem from weak passwords, unpatched software, or insider threats rather than sophisticated attacks. Implement network segmentation to limit breach scope and monitor user access patterns for unusual activity. Regular vulnerability scans identify security gaps before attackers exploit them, while encryption protects sensitive data even when systems face compromise.

These threats create complex insurance needs that require careful policy selection and comprehensive coverage analysis. Unlike general liability or property insurance that protects against external risks, cyber liability coverage addresses internal vulnerabilities that digital threats exploit.

How Do You Select the Right Cyber Policy?

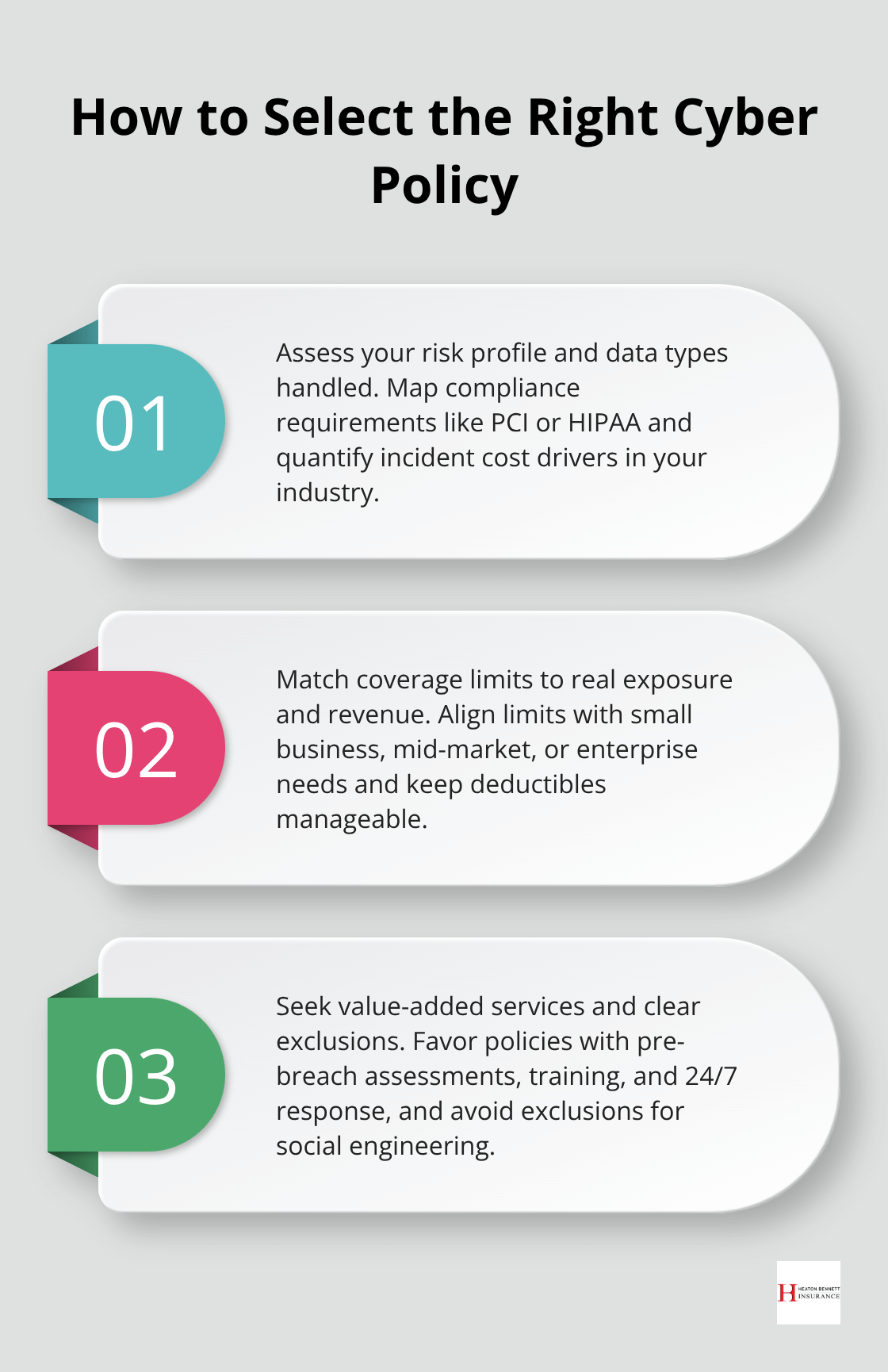

Assess Your Business Risk Profile

Risk assessment drives every cyber insurance decision and starts with data classification. Companies that handle credit card information face Payment Card Industry compliance requirements that cost $10,000-50,000 annually when breached. Healthcare organizations need HIPAA-compliant policies with minimum $2 million coverage limits since violations average $10,000 per compromised record (according to Department of Health and Human Services data). Manufacturing firms require specialized coverage for intellectual property theft, which costs businesses an average of $2.6 million per incident based on Ponemon Institute research.

Match Coverage Limits to Real Exposure

Purchase coverage that equals your annual revenue or $5 million minimum, whichever proves higher. Small businesses with $1-5 million revenue typically need $1-2 million limits, while mid-market companies require $5-10 million protection. Deductibles should not exceed 2% of annual revenue since higher amounts delay recovery efforts. Choose per-claim deductibles over aggregate options because multiple incidents can exhaust your coverage faster.

Evaluate Technology-Specific Needs

Technology companies need errors and omissions coverage that starts at $1 million since software failures cost clients an average of $300,000 per hour in downtime. Software developers face unique liability exposures when their products malfunction or fail to perform as promised. Professional liability protection covers these risks that standard cyber policies often exclude.

Compare Additional Services and Support

Premium policies include 24/7 incident response teams that reduce breach costs by 30% compared to self-managed responses (according to IBM data). Look for policies that provide pre-breach services like vulnerability assessments, employee training programs, and security audits. These services typically cost $50,000-100,000 separately but come included with comprehensive coverage. Avoid policies that exclude social engineering losses since these attacks represent 98% of successful cyber incidents that target businesses. The best way to determine what type of business insurance you should purchase is to ask a licensed agent who can assist you with assessing your specific needs. The best insurers offer legal hotlines, crisis communications support, and regulatory guidance that proves invaluable during actual incidents.

Final Thoughts

Cyber insurance has transformed from optional coverage to business necessity as digital threats multiply and attack costs soar. The global cyber insurance market will reach $29 billion by 2027, which reflects widespread recognition that traditional insurance cannot address modern digital risks. Businesses across all sectors now face sophisticated attacks that traditional policies cannot cover.

Comprehensive protection requires three strategic steps that smart business owners follow. First, conduct thorough risk assessments that identify your specific vulnerabilities and compliance requirements. Second, purchase adequate coverage limits that match your revenue exposure and industry standards (typically 1-2 times annual revenue). Third, select policies with pre-breach services and 24/7 incident response teams that reduce recovery costs by 30%.

We at Heaton Bennett Insurance provide tailored insurance solutions that address your unique cyber risks through our comprehensive assessment process. Our independent agency approach means we compare options across multiple carriers rather than push single-carrier solutions. Cyber attacks will target your business eventually, so adequate protection becomes essential for survival.