How to Get Small Business Hazard Insurance Coverage

Small business hazard insurance protects your company from unexpected disasters that could destroy your operations overnight. Standard business policies often leave dangerous gaps in coverage.

We at Heaton Bennett Insurance see too many business owners learn this lesson the hard way. The right hazard coverage can mean the difference between recovering from a disaster and closing your doors permanently.

What Does Hazard Insurance Actually Cover

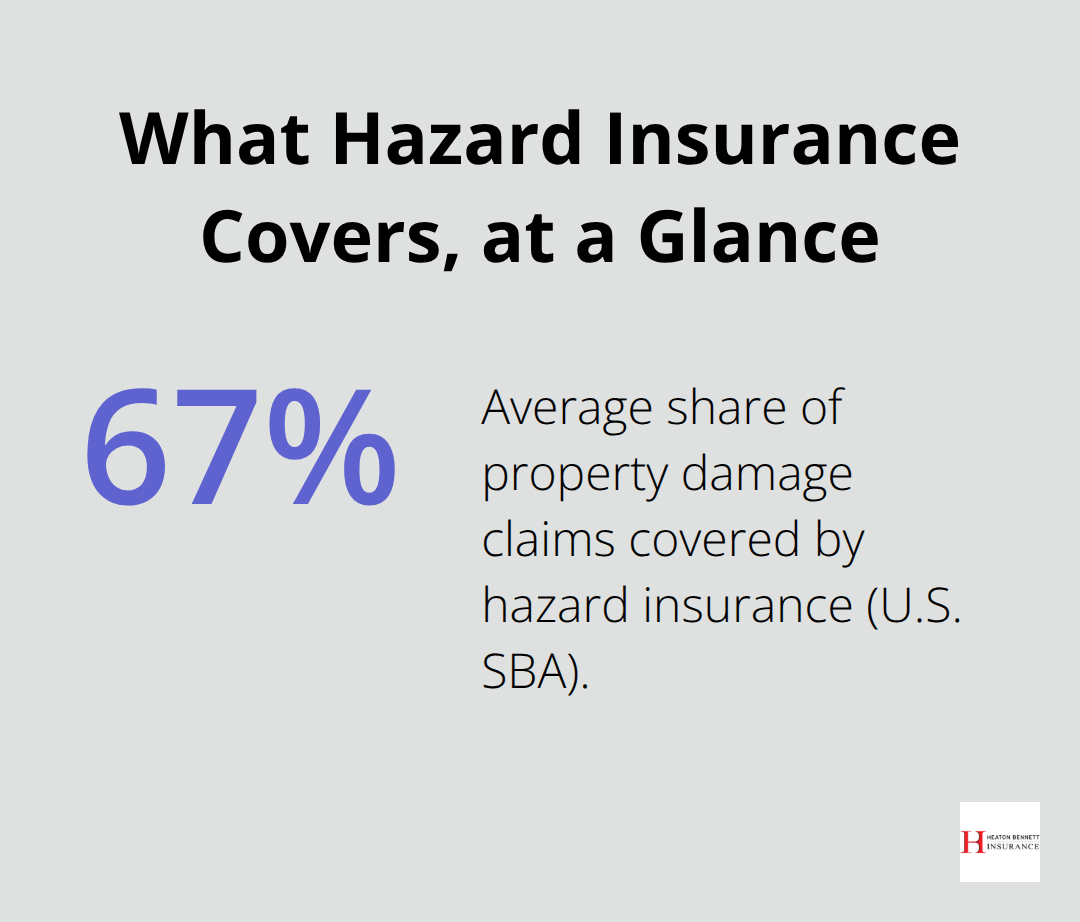

Small business hazard insurance protects your physical property against specific perils that standard policies often exclude or limit. The coverage shields your building, equipment, inventory, and fixtures from fire damage, theft, vandalism, lightning strikes, explosions, and certain weather events like hail or windstorms. According to the U.S. Small Business Administration, hazard insurance covers an average of 67% of property damage claims, which makes it a cornerstone of business protection. The policy typically includes your computers, machinery, furniture, and stock, but excludes earthquakes and floods unless you purchase separate endorsements.

Standard Business Insurance Creates Dangerous Gaps

Most basic business policies provide minimal hazard protection and often cap coverage at $10,000 to $25,000 for equipment and inventory combined. This creates massive exposure for businesses with significant physical assets. Manufacturing facilities face average property damage costs of $180,000 per incident, while retail operations average $85,000 in losses from theft and vandalism annually. Home-based businesses receive only $2,500 in business property coverage under standard homeowners policies (leaving substantial gaps for entrepreneurs with expensive equipment or inventory).

Hazard Insurance Serves a Different Purpose Than General Liability

General liability insurance protects against third-party claims for bodily injury and property damage and averages $42 monthly for small businesses. Hazard insurance protects your own property from direct physical loss, with commercial property coverage that averages $67 monthly. The two serve completely different purposes and both remain essential for comprehensive protection. General liability covers lawsuits from customer injuries, while hazard insurance covers your building when it burns down or equipment when thieves steal it.

Natural Disasters Require Special Attention

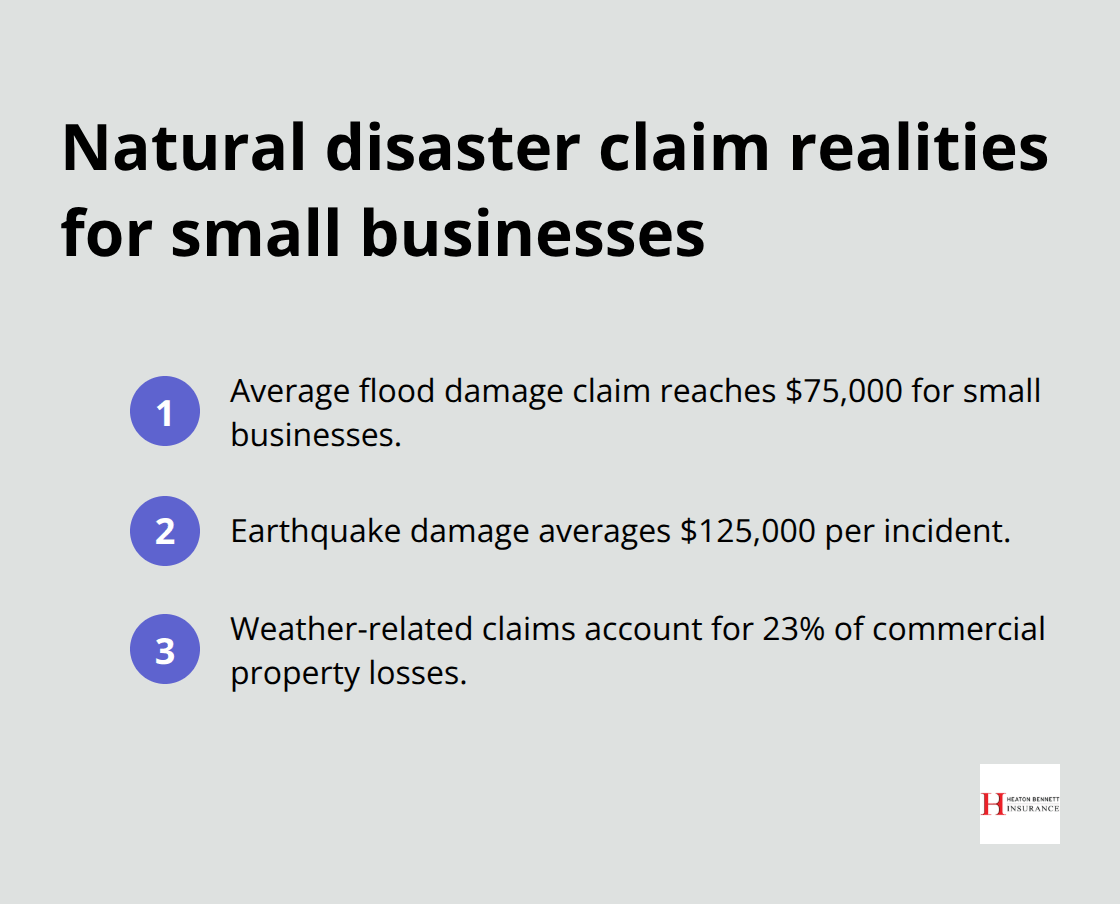

Standard hazard policies exclude major natural disasters like earthquakes, floods, and hurricanes (which require separate endorsements or policies). These exclusions catch many business owners off guard when disaster strikes. The average flood damage claim for small businesses reaches $75,000, while earthquake damage averages $125,000 per incident. Weather-related claims account for 23% of all commercial property losses, yet most businesses operate without adequate natural disaster coverage.

Understanding these coverage gaps helps you identify exactly which hazards threaten your specific business operations and location.

Types of Hazards Your Business Should Prepare For

Natural Disasters Strike Without Warning

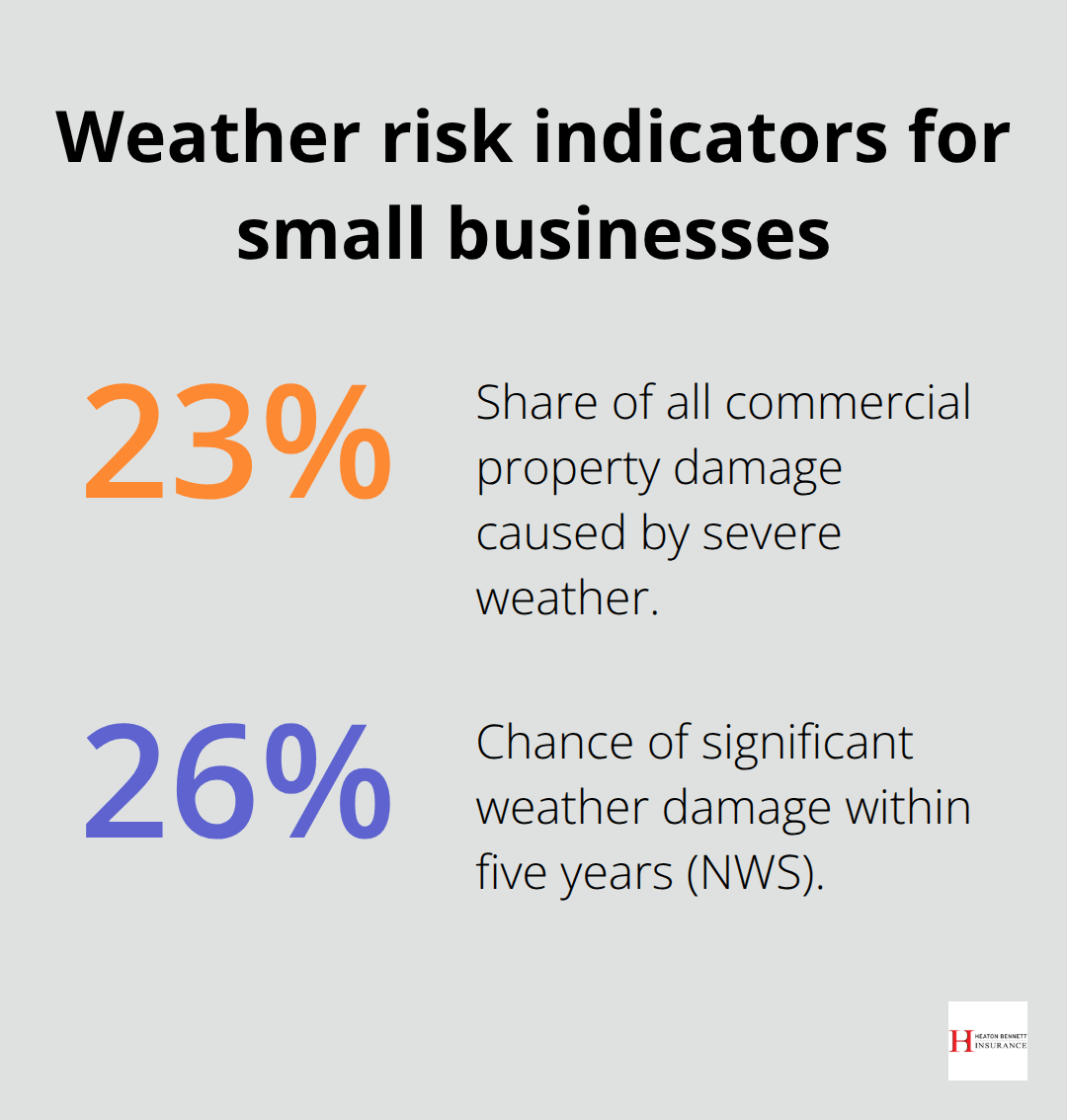

Severe weather causes 23% of all commercial property damage, yet most businesses remain dangerously unprepared. Tornadoes generate average business losses of $195,000 per incident, while hailstorms cause $85,000 in typical damage to commercial roofs and equipment. The National Weather Service reports that businesses face a 26% chance of significant weather damage within any five-year period.

Windstorms destroy signage, break windows, and damage HVAC systems. These events create immediate operational shutdowns that can last weeks. Heavy rainfall floods buildings within minutes and destroys electronics, inventory, and documents. Standard policies exclude water damage from rising water levels, which makes separate flood coverage essential for complete protection.

Fire Represents Your Greatest Single Threat

Fire destroys more small businesses than any other single peril. The National Fire Protection Association reports that commercial fires cause $2.4 billion in annual property damage. Electrical fires start from overloaded circuits, faulty wiring, and aged equipment, then spread rapidly through buildings.

Kitchen fires in restaurants average $165,000 in damages per incident, while manufacturing fires reach $340,000 due to flammable materials and complex machinery. Lightning strikes cause electrical surges that fry computer systems, phone equipment, and manufacturing controls instantly. Fire suppression systems and proper electrical maintenance reduce your premiums while they protect your investment.

Theft and Vandalism Target Vulnerable Businesses

Commercial theft costs small businesses $50 billion annually. Retail operations lose an average of $1,230 per incident (according to the National Retail Federation). Burglars target electronics, inventory, and cash while they often cause additional property damage during break-ins.

Vandalism attacks windows, signage, and building exteriors. These attacks create immediate repair costs and lost business during cleanup periods. Employee theft accounts for 43% of business inventory losses, which makes internal controls essential. Security cameras, alarm systems, and proper lighting significantly reduce both theft frequency and insurance premiums.

The specific risks that threaten your business depend heavily on your industry, location, and operational setup. This makes a customized approach to hazard insurance coverage absolutely essential for adequate protection.

How to Choose the Right Hazard Insurance Policy

Calculate Your True Property Values

Start by calculating your actual property values, not what you paid years ago. Equipment replacement costs rise 4-6% annually, while construction values increase 3-5% according to Marshall & Swift data. Document every asset with photos and current market prices. Manufacturing businesses need coverage that averages $500 per square foot, while retail operations require $200-300 per square foot. Service businesses with minimal equipment need $50-100 per square foot. Location matters tremendously – coastal properties face 40% higher premiums due to hurricane exposure, while earthquake zones add 25-35% to base rates.

Coverage Limits Determine Your Financial Survival

Standard policies offer actual cash value, which pays depreciated amounts that leave you unable to replace damaged property. Replacement cost coverage costs 15-25% more but pays full replacement value without depreciation deductions. Business income coverage replaces lost revenue during repairs and typically costs 10-15% of your property premium. The Insurance Information Institute reports that 40% of businesses never reopen after major property damage (primarily due to inadequate coverage limits). Choose deductibles between $1,000-$5,000 to balance premium savings with manageable out-of-pocket costs.

Independent Agents Access More Options

Independent agents access 15-25 carriers compared to captive agents who sell only one company’s products. This competition drives down your premiums by 20-30% on average. Independent agents also handle claims advocacy when disputes arise, while direct carriers prioritize their company’s interests over yours. Direct online carriers may seem cheaper initially, but they exclude coverage options that independent agents include automatically (creating dangerous gaps that cost far more than premium savings).

Compare Deductibles and Policy Terms

Higher deductibles reduce your monthly premiums but increase your financial exposure during claims. A $5,000 deductible saves 25-40% compared to $1,000 deductibles, but you must have cash reserves to cover the difference. Review policy exclusions carefully – some carriers exclude water damage from roof leaks or limit coverage for electronic equipment. Named perils policies cover only specifically listed hazards, while open perils policies cover everything except listed exclusions.

Final Thoughts

Small business hazard insurance demands immediate action and professional guidance. Document all your business assets with current replacement values, then request quotes from multiple carriers through an independent agent. Review coverage limits carefully and choose replacement cost over actual cash value to avoid devastating gaps during claims.

We at Heaton Bennett Insurance help Austin businesses navigate these complex decisions. As an independent agency, we access multiple carriers to find coverage that matches your specific risks and budget. Our team guides you through policy comparisons and identifies exclusions that could leave you exposed.

The cost of adequate hazard coverage represents a fraction of potential losses from fire, theft, or natural disasters (businesses without proper protection face a 40% chance of permanent closure after major property damage). Schedule a consultation with Heaton Bennett Insurance today to protect your business investment. Your operations depend on the right coverage before disaster strikes, not after.