Group AD&D Insurance An Often Overlooked Employee Benefit

Most employers focus on health insurance and retirement plans when designing benefit packages. Yet Group AD&D insurance often gets pushed aside despite offering significant value at minimal cost.

We at Heaton Bennett Insurance see this oversight repeatedly across industries. This additional layer of protection can strengthen your entire benefits strategy while addressing gaps that traditional life insurance leaves behind.

How Does Group AD&D Insurance Actually Work

Group AD&D insurance operates differently from traditional life insurance in three fundamental ways. Standard life insurance pays benefits for death from any cause, whether illness, natural causes, or accidents. AD&D insurance only pays when death or injury results from covered accidents like car crashes, falls, or workplace incidents. The Centers for Disease Control and Prevention reports accidents as the third leading cause of death in the United States, which makes this targeted coverage more relevant than many employers realize.

Coverage Amounts Follow Clear Formulas

Most group AD&D plans tie benefit amounts directly to employee salaries. Basic employer-paid coverage typically equals one to two times annual salary, while voluntary employee-paid options can reach five to ten times salary. A $50,000 annual earner might receive $100,000 in basic AD&D coverage automatically, with options to purchase additional protection up to $500,000. Dismemberment benefits follow percentage schedules: loss of both hands pays 100% of the benefit, single limb loss pays 50%, and loss of sight in one eye typically pays 25%. These predetermined amounts eliminate guesswork during claims processing.

Integration Creates Maximum Value

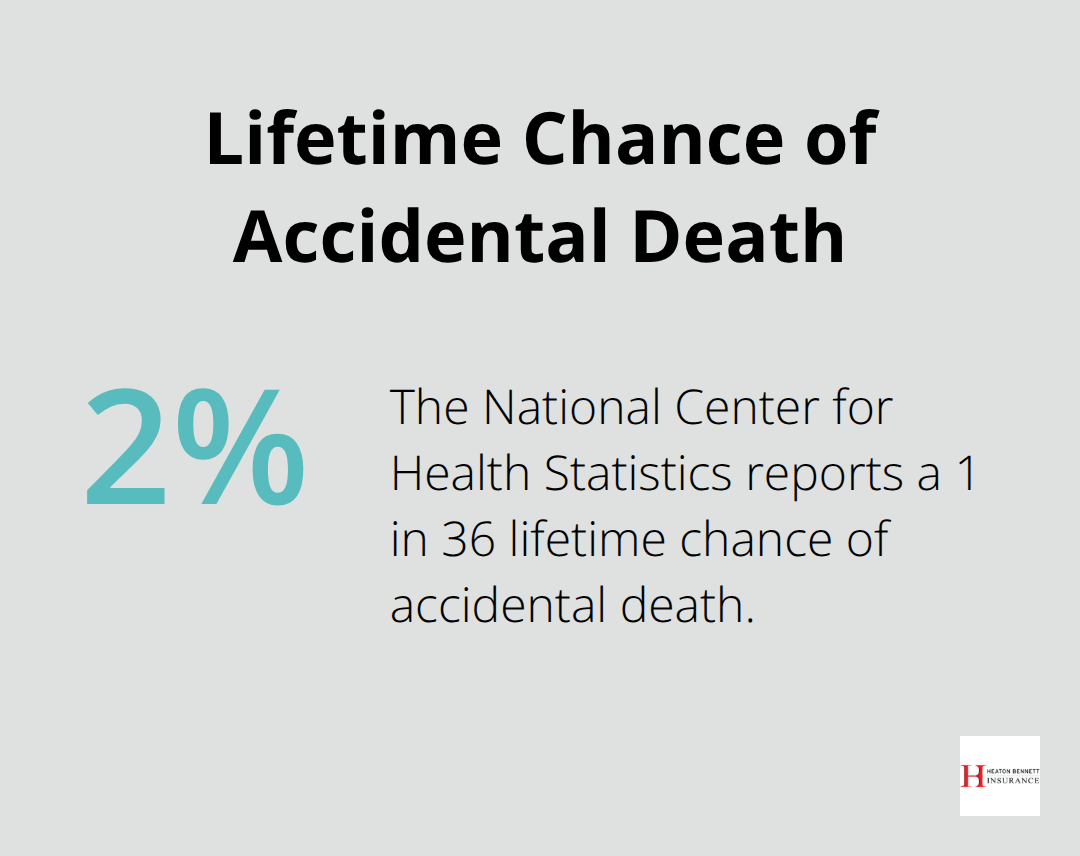

Smart employers bundle AD&D with life insurance rather than offer it standalone. This approach reduces administrative costs while it provides employees comprehensive accident protection. Business travel accident riders add extra coverage during work-related trips, often doubling or tripling the base benefit amount. The National Center for Health Statistics shows a 1 in 36 lifetime chance of accidental death (making this supplemental coverage a practical addition that addresses specific risks standard life insurance handles equally with all other causes).

Administrative Simplicity Drives Adoption

Group AD&D requires minimal underwriting compared to traditional life insurance. Most plans accept all eligible employees without medical exams or health questionnaires. This streamlined approach reduces enrollment complexity and speeds up implementation. Payroll deduction systems handle premium collection automatically, while simplified claim forms expedite benefit payments to families during difficult times.

The cost-effectiveness of group AD&D becomes even more apparent when employers examine the broader financial impact on their benefits strategy.

Why Group AD&D Makes Financial Sense for Employers

Premium Costs Stay Remarkably Low

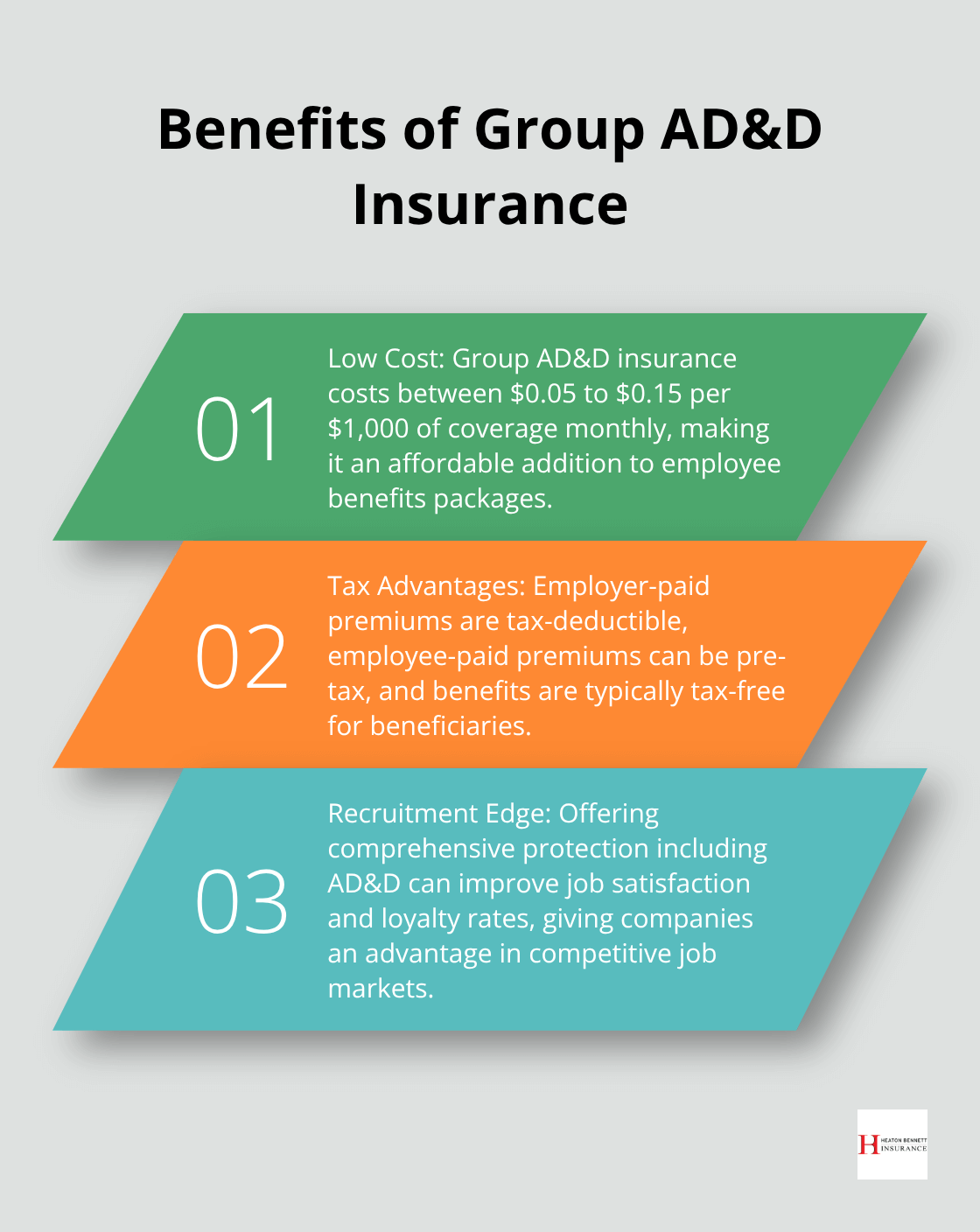

Group AD&D insurance delivers exceptional value at minimal expense. Employer-paid basic coverage typically costs between $0.05 to $0.15 per $1,000 of coverage monthly. A company that provides $50,000 AD&D coverage for 100 employees pays roughly $250 to $750 per month total. This represents less than 2% of most health insurance budgets while it adds meaningful protection. Voluntary employee-paid options cost even less for employers since workers fund their own additional coverage through payroll deduction.

Tax Advantages Benefit Everyone

Employer-paid AD&D premiums qualify as tax-deductible business expenses, which reduces overall benefit costs. Employee-paid premiums come from pre-tax dollars when employers process them through Section 125 cafeteria plans (this lowers taxable income for workers). Benefits paid to beneficiaries arrive tax-free, unlike retirement account distributions or other financial instruments. The IRS treats AD&D coverage under $50,000 as non-taxable income for employees, which eliminates phantom income issues that plague higher life insurance amounts.

Recruitment Edge Over Competitors

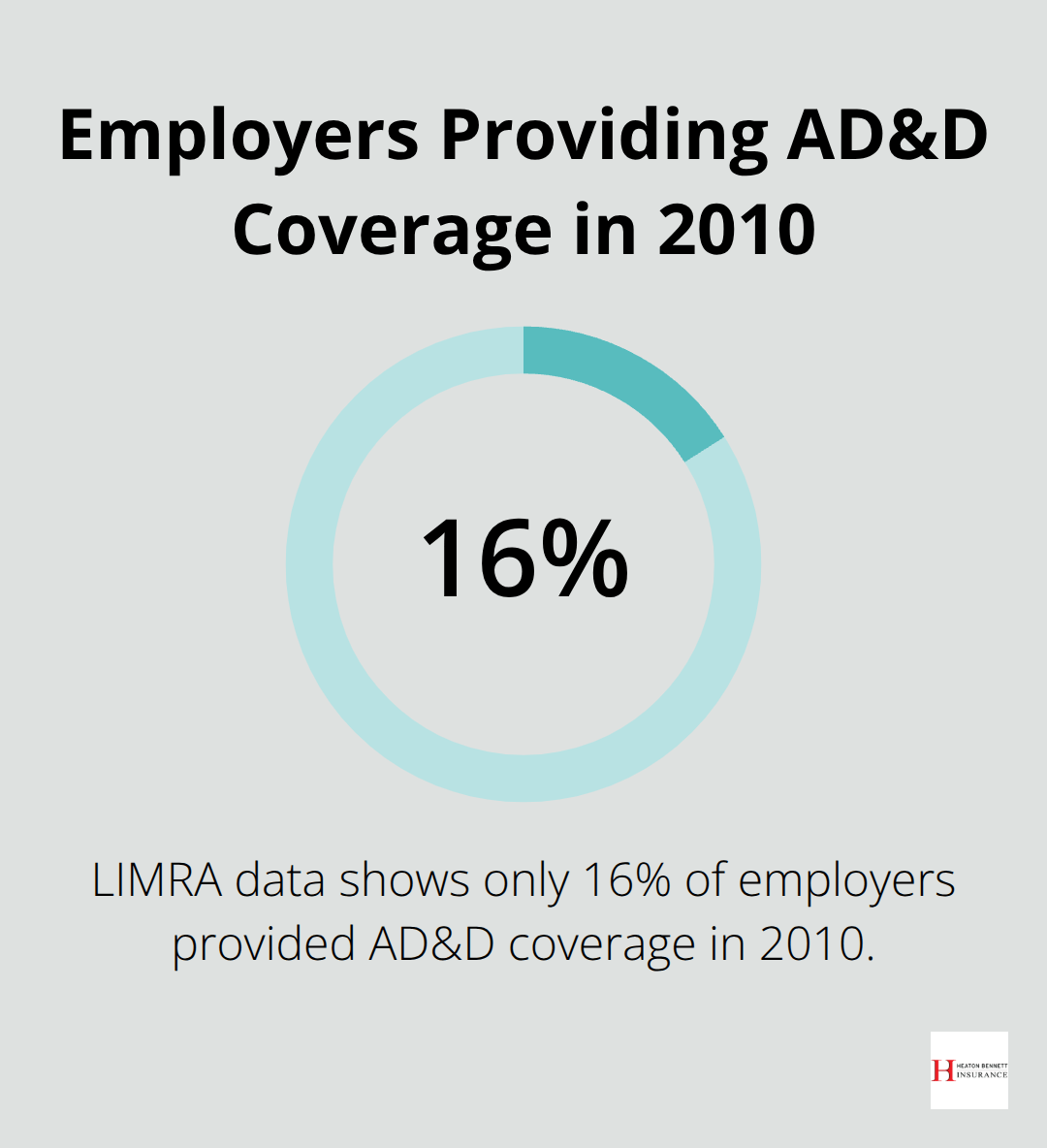

PwC research from 2023 identifies finances as the primary daily stress source for American adults. Companies that offer comprehensive protection including AD&D address these concerns directly. LIMRA data shows only 16% of employers provided AD&D coverage in 2010, which creates differentiation opportunities for forward-thinking companies. MetLife studies demonstrate that employees with supplemental benefits report higher job satisfaction and loyalty rates. Workers increasingly evaluate total compensation packages rather than salary alone (this makes comprehensive benefits packages essential for attracting quality candidates in competitive markets).

Administrative Simplicity Reduces Overhead

Group AD&D requires minimal administrative burden compared to traditional insurance products. Most carriers handle enrollment through existing payroll systems without additional software requirements. Claims processing follows standardized procedures that reduce HR department workload during difficult situations. Automated premium collection through payroll deduction eliminates billing complications and late payment issues that plague other benefit programs.

The specific features and coverage limitations of group AD&D plans determine how effectively this benefit protects employees while it controls costs for employers.

Key Features and Considerations

Group AD&D insurance comes with specific limitations that employers must understand before implementation. Standard AD&D policies exclude deaths from natural causes, suicide, drug overdoses, and injuries sustained during criminal activities. High-risk recreational activities like skydiving, mountaineering, or professional sports typically fall outside coverage boundaries. Workers in dangerous occupations such as firefighting, law enforcement, or military service may face eligibility restrictions or higher premiums. Most policies also exclude injuries that occur while under the influence of drugs or alcohol (which can affect a significant portion of accident claims).

Coverage Exclusions Affect Claims

The exclusion list varies between carriers but follows predictable patterns. Deaths from medical conditions, heart attacks, or strokes receive no benefits regardless of circumstances. War-related injuries and acts of terrorism typically fall outside standard coverage. Some policies exclude deaths that occur during the commission of felonies or while the insured person violates laws. Aviation exclusions often apply to private aircraft but not commercial flights. Employers should review exclusion lists carefully since these limitations directly impact the value employees receive from their coverage.

Portability Protects Employee Investments

The strongest group AD&D plans offer portability features that allow employees to maintain coverage after they leave the company. This conversion option typically requires employees to continue premium payments directly to the insurance carrier within 31 days of termination. Portable coverage amounts usually mirror the group benefit levels, though some carriers reduce maximums for individual policies. Employees who develop health conditions during employment particularly benefit from portability since they can maintain accident coverage without medical underwriting.

Integration Maximizes Existing Benefits

Smart benefit design combines AD&D with existing life insurance rather than treats it as a separate product. This bundled approach reduces administrative costs and eliminates coverage gaps between different policies. Many carriers offer AD&D riders on group life insurance that cost 20-30% less than standalone policies. The combination also simplifies claims processing since beneficiaries work with a single carrier for both accident and natural death benefits (streamlining what can be a complex process during difficult times).

Plan Customization Options

Employers can tailor AD&D coverage to match their workforce demographics and risk profiles. Construction companies might emphasize higher benefit amounts due to workplace accident risks. Office-based businesses may focus on travel accident riders for employees who frequently travel for work. Some plans allow employees to purchase coverage for spouses and children at reduced rates. Flexible benefit structures let workers choose coverage levels that match their individual financial needs and family situations.

Final Thoughts

Group AD&D insurance represents one of the most cost-effective ways to strengthen employee benefits while it addresses financial protection gaps. The numbers speak clearly: premiums cost as little as $0.05 per $1,000 of coverage monthly, yet provide meaningful protection against the third leading cause of death in America. This combination of low cost and targeted coverage creates exceptional value for both employers and employees.

Companies must evaluate their current benefit structure and identify protection gaps when they implement group AD&D coverage. They should review workforce demographics, travel patterns, and industry-specific accident risks while they compare carrier options for coverage amounts, exclusions, and portability features. Most importantly, employers need to examine how AD&D integrates with life insurance to maximize administrative efficiency and employee value (which creates the strongest overall protection strategy).

Companies that offer comprehensive benefits including group AD&D report higher employee satisfaction and retention rates. Workers gain peace of mind when they know their families have financial protection against unexpected accidents, while employers differentiate themselves in competitive talent markets. We at Heaton Bennett Insurance help Austin businesses navigate these complex benefit decisions through our comprehensive approach to group insurance solutions.