Indexed Annuities Balancing Growth and Security in Retirement

At Heaton Bennett Insurance, we understand the importance of balancing growth and security in retirement planning. Indexed annuities have emerged as a popular option for those seeking this balance.

These financial products offer a unique combination of potential market-linked returns and downside protection. In this post, we’ll explore the ins and outs of indexed annuities and how they might fit into your retirement strategy.

What Are Indexed Annuities?

The Basics of Indexed Annuities

Indexed annuities combine features of traditional fixed annuities with the growth potential of market-linked investments. These financial products have gained popularity among retirees who want to grow their savings while limiting downside risk.

How Indexed Annuities Work

An indexed annuity’s returns link to the performance of a specific market index (such as the S&P 500). Unlike direct stock market investments, these annuities offer a safety net. If the market index declines, your principal remains protected from losses. This protection comes with a trade-off – your potential gains typically face caps or limits through participation rates.

For instance, an indexed annuity with a 7% cap rate would only credit 7% for that period, even if the linked index grows by 10%. Similarly, an 80% participation rate means you’d receive 80% of the index’s gains, up to any applicable cap.

Comparing Annuity Types

Indexed annuities occupy a middle ground between fixed and variable annuities. Fixed Index Annuities offer a guaranteed interest rate, providing stability but potentially lower returns. Variable annuities allow direct investment in mutual funds, offering higher growth potential but also exposing the investor to market losses.

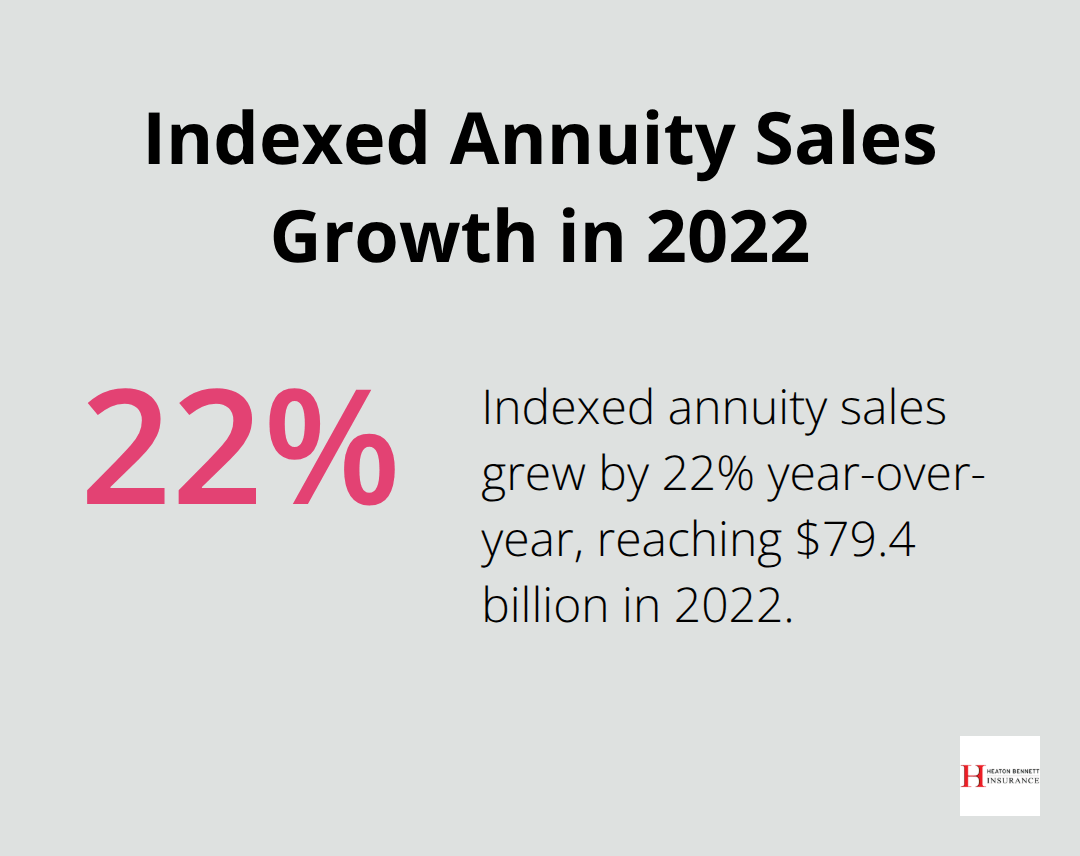

A 2022 LIMRA study revealed that indexed annuity sales grew by 22% year-over-year, reaching $79.4 billion. This growth outpaced both fixed and variable annuities, highlighting their appeal in balancing growth and security.

The Impact of Market Indexes

The choice of market index can significantly affect your annuity’s performance. While the S&P 500 is common, some annuities track other indexes like the Nasdaq-100 or international markets. Understanding how the chosen index has performed historically and how it aligns with your risk tolerance and financial goals is essential.

Some insurers use proprietary indexes, which can complicate performance comparisons. Always request detailed explanations of how these indexes work and their historical performance data before making a decision.

As we move forward to explore the advantages of indexed annuities, you’ll gain a clearer picture of how these financial products can fit into your retirement strategy. The next section will shed light on the potential benefits and why many retirees find indexed annuities an attractive option for their portfolios.

Why Indexed Annuities Attract Retirees

Growth Potential with a Safety Net

Indexed annuities offer higher returns compared to traditional fixed annuities. These financial products allow investors to participate in market gains without direct market risk exposure. A 2023 report by the Insured Retirement Institute revealed that indexed annuities have outperformed fixed annuities by an average of 1.5% to 2% annually over the past decade.

However, potential gains come with limitations. Most indexed annuities have caps on returns (typically ranging from 3% to 9%, depending on market conditions and the specific product). Understanding these caps is essential for evaluating their impact on overall retirement strategy.

Protection Against Market Downturns

The downside protection of indexed annuities provides significant peace of mind for retirees. If the linked market index experiences a downturn, the principal investment remains protected. This means the annuity’s value won’t decrease even in years of poor market performance.

A study by Allianz Life Insurance Company found that 72% of Americans worry about a major recession impacting their retirement savings. Indexed annuities address this concern by offering a buffer against market losses, making them attractive to risk-averse investors.

Tax Benefits for Long-Term Growth

Indexed annuities offer tax advantages that boost long-term growth. The earnings within an indexed annuity grow tax-deferred, meaning taxes on gains aren’t paid until withdrawals begin. This results in more substantial compound growth over time.

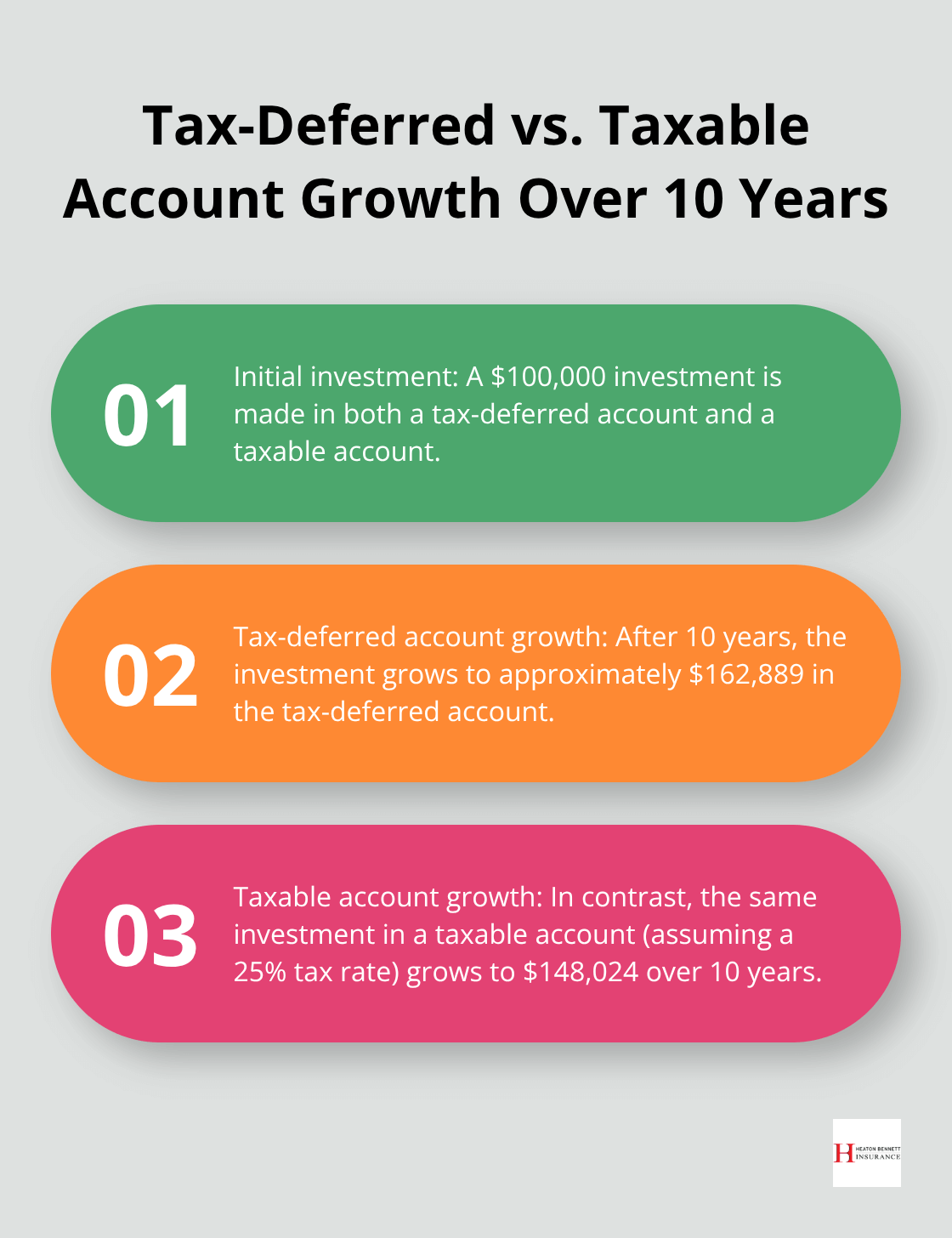

For example, a $100,000 investment growing at 5% annually would be worth approximately $162,889 after 10 years in a tax-deferred account, compared to $148,024 in a taxable account (assuming a 25% tax rate). This difference can be significant, especially for those in higher tax brackets or those planning for a long retirement.

Guaranteed Income Options

Many indexed annuities offer guaranteed income options, which provide a stable income stream in retirement. These options allow annuity holders to convert their accumulated value into regular payments, either for a specific period or for life.

A recent survey by the Employee Benefit Research Institute found that 82% of workers express concern about having enough money in retirement. Guaranteed income options in indexed annuities can help address this concern by providing a predictable income stream, regardless of market performance.

While indexed annuities offer numerous advantages, they’re not suitable for everyone. The next section will explore important considerations and potential drawbacks to keep in mind when evaluating these financial products.

What Are the Risks of Indexed Annuities?

Complex Fee Structures

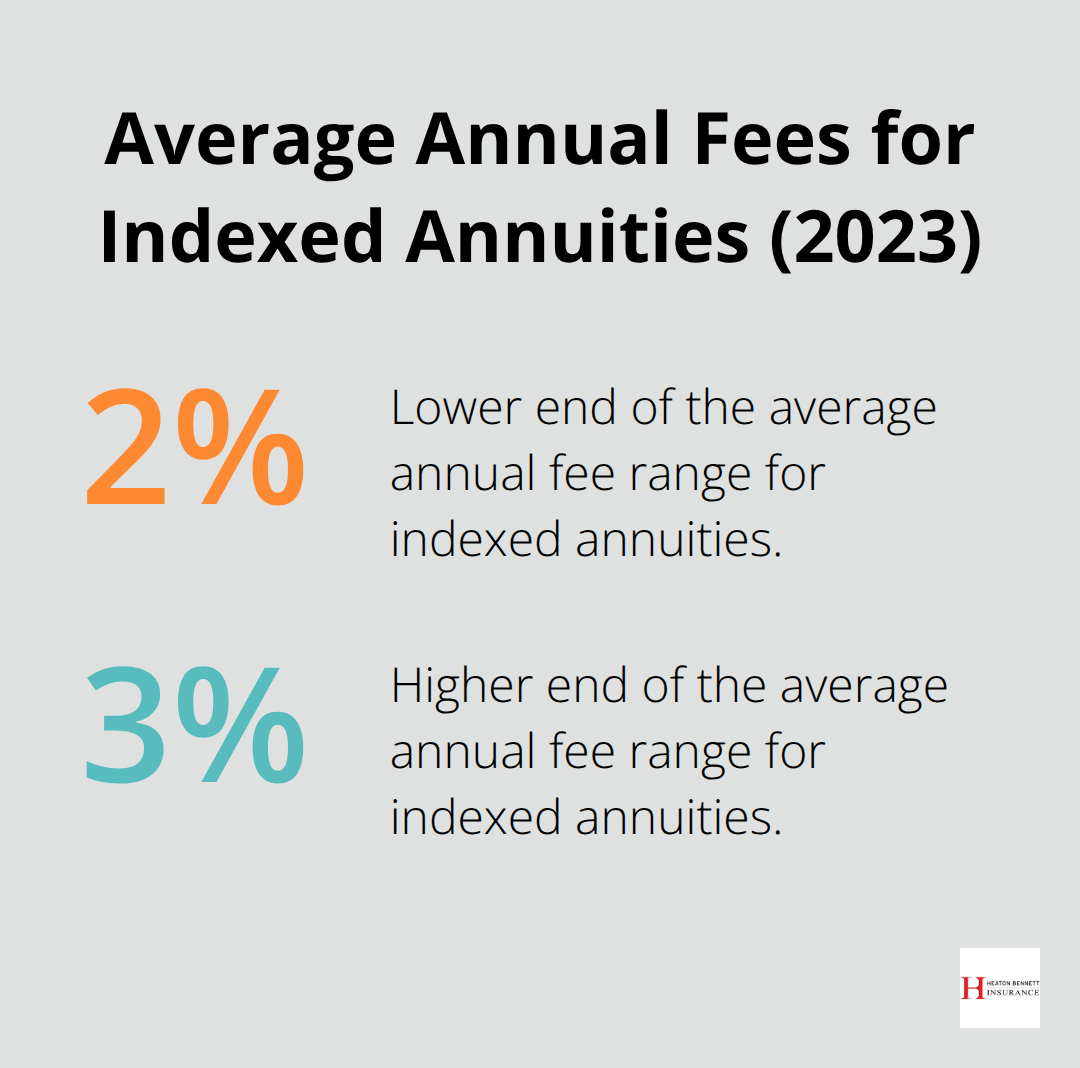

Indexed annuities often have intricate fee structures that challenge investors. These include mortality and expense charges, administrative fees, and rider costs. A 2023 study by the National Association of Insurance Commissioners revealed that the average annual fee for indexed annuities ranges from 2% to 3% of the contract value. These fees can significantly impact overall returns, especially in low-yield environments.

Limited Upside Potential

While indexed annuities protect against market downturns, they also restrict potential gains. Caps and participation rates limit how much you benefit from market upswings. For instance, an annuity with a 6% cap would only credit 6% even if the linked index grows by 10%. A 70% participation rate means you receive only 70% of the index’s gains.

The LIMRA Secure Retirement Institute reports that the average cap rate for indexed annuities in 2023 was 5.5% (down from 6.2% in 2020). This decline emphasizes how these limitations affect long-term financial goals.

Liquidity Constraints

Indexed annuities are long-term investments, and early access to your money can prove costly. Surrender charges, which typically decrease over time, can range from 7% to 20% of the withdrawal amount in the early years of the contract. These charges can significantly erode your principal if you need unexpected access to funds.

Moreover, withdrawals before age 59½ may incur a 10% federal tax penalty (on top of regular income taxes). This lack of liquidity can create problems for investors who need access to their funds for emergencies or other financial opportunities.

Suitability Concerns

Indexed annuities don’t suit all investors. They work best for individuals with a long-term investment horizon who don’t need immediate access to their funds. A 2022 survey by the Insured Retirement Institute found that indexed annuities are most popular among investors aged 55-70, with at least $100,000 in investable assets.

Younger investors or those with shorter-term financial goals may find the long surrender periods and potential penalties restrictive. Similarly, individuals who can tolerate more risk and seek higher returns might find the growth limitations frustrating.

Market Volatility Impact

While indexed annuities offer protection against market losses, they can still be affected by market volatility. In periods of high volatility, insurance companies may lower cap rates or participation rates to manage their risk. This can result in lower potential returns for annuity holders, even in years when the market performs well.

Final Thoughts

Indexed annuities offer a unique blend of growth potential and downside protection for retirees. These financial products allow participation in market gains while safeguarding principal during market downturns. The tax-deferred growth and guaranteed income options enhance their appeal for long-term retirement planning.

Professional guidance proves essential when considering indexed annuities due to their complexities. At Heaton Bennett Insurance, we help clients navigate retirement planning intricacies. Our team provides personalized advice on how indexed annuities might fit into your comprehensive retirement strategy.

Indexed annuities can play a valuable role in a well-rounded retirement portfolio. They provide a middle ground between fixed annuities’ stability and variable annuities’ growth potential. Your decision to include indexed annuities should stem from a thorough understanding of your financial situation, goals, and risk tolerance (which we can help you assess).