Workers’ Comp vs Occupational Accident: Which to Choose?

At Heaton Bennett Insurance, we understand the importance of protecting your business and employees. Choosing the right insurance coverage can be a challenging task, especially when it comes to workers’ compensation vs occupational accident insurance.

These two types of coverage serve different purposes and have distinct implications for your business. In this post, we’ll break down the key differences and help you determine which option is best suited for your company’s needs.

What is Workers’ Compensation Insurance?

Definition and Purpose

Workers’ compensation insurance serves as a vital shield for both employees and businesses. This type of insurance provides coverage for employees who suffer work-related injuries or illnesses. It aims to protect both workers and employers from the financial consequences of workplace accidents.

Legal Requirements

In most states, workers’ compensation insurance is not optional-it’s a legal necessity for businesses with employees. The specific requirements vary by state, but generally, if you employ even one person, you must carry this coverage. For instance, Texas allows private employers to choose whether to provide workers’ compensation insurance, while public employers must offer it. It’s essential to verify your state’s specific laws to ensure compliance.

Coverage and Benefits

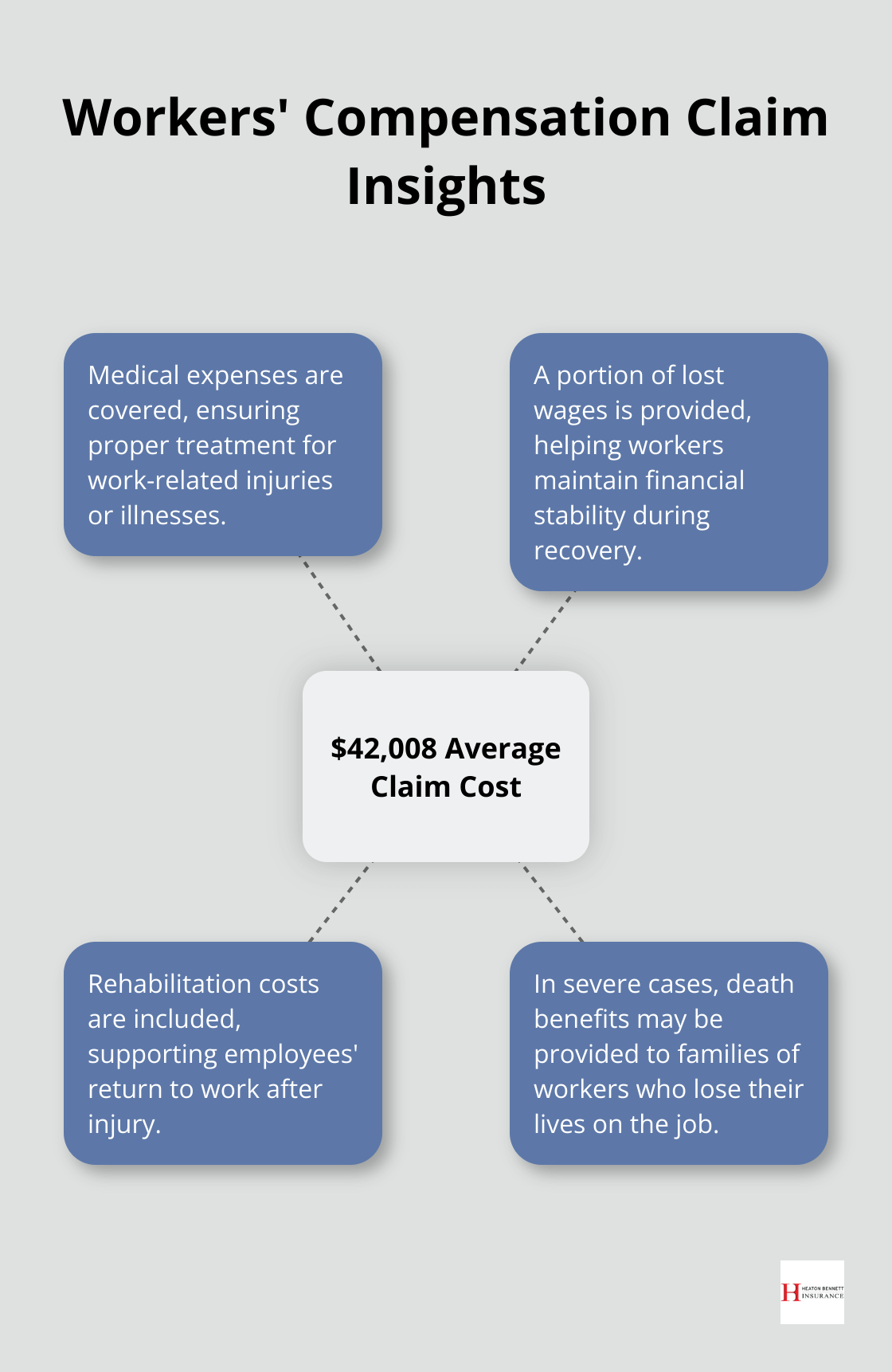

Workers’ compensation typically covers:

- Medical expenses

- A portion of lost wages

- Rehabilitation costs for injured employees

In severe cases, it may also provide death benefits to the families of workers who lose their lives on the job. The National Safety Council reports that the average cost of a workers’ compensation claim in 2019 was $42,008 (highlighting the significant financial protection this insurance offers).

Business Protection

While the primary focus is on employee protection, workers’ comp also shields businesses from potentially devastating lawsuits. In exchange for this coverage, employees typically waive their right to sue their employer for negligence. This trade-off creates a more predictable and manageable system for handling workplace injuries.

Industry Impact

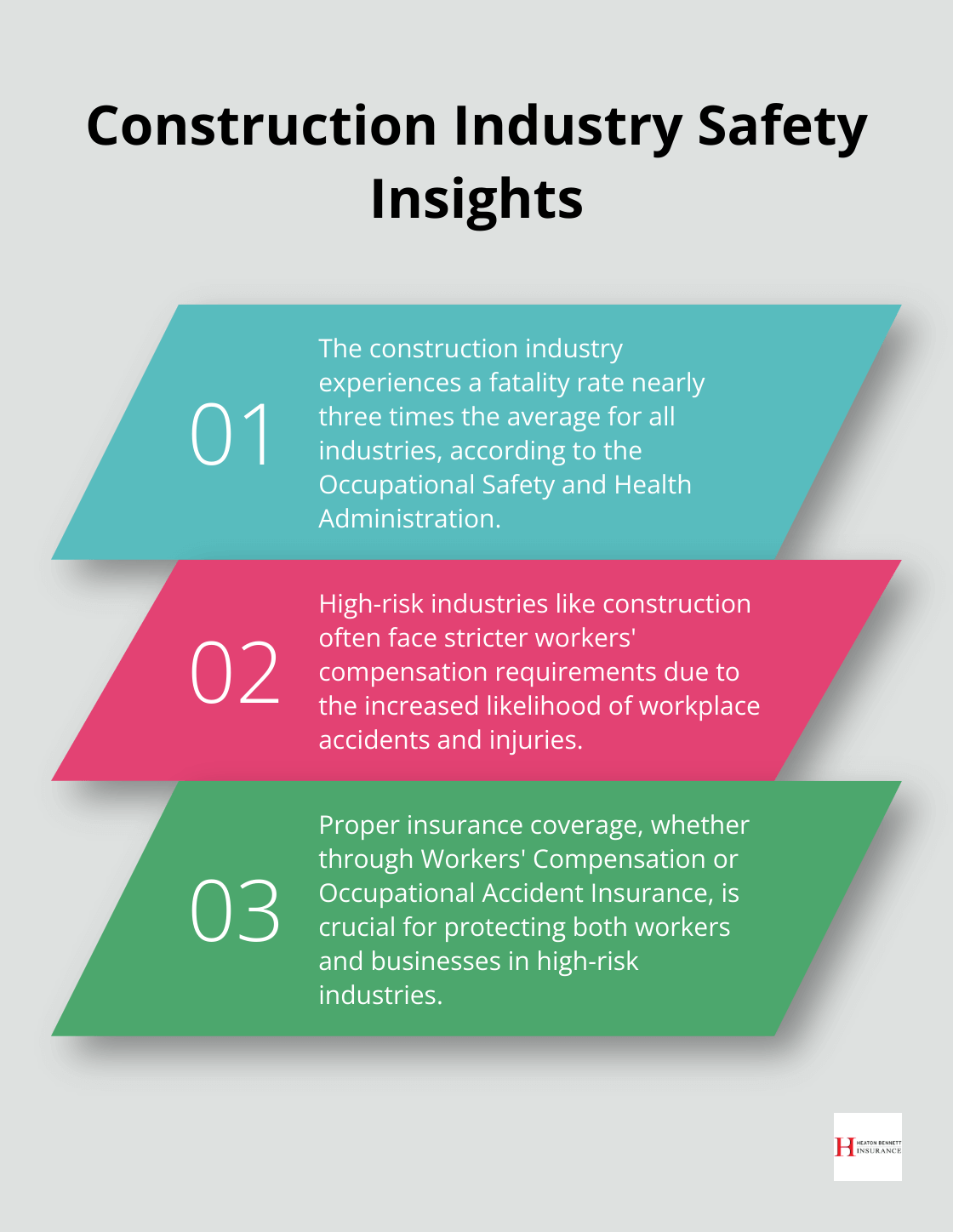

Different industries face varying levels of risk, which can affect workers’ compensation requirements and costs. High-risk industries (such as construction or manufacturing) often face stricter regulations and higher premiums compared to low-risk office environments.

As we move forward, it’s important to understand how workers’ compensation differs from occupational accident insurance. Let’s explore the latter to gain a comprehensive view of your options for protecting your business and employees.

Exploring Occupational Accident Insurance

Definition and Purpose

Occupational Accident Insurance (OAI) provides specialized coverage for independent contractors and self-employed individuals. Unlike Workers’ Compensation, OAI offers a voluntary option for financial protection against work-related injuries or illnesses.

Coverage and Benefits

OAI typically includes:

- Medical expenses

- Disability benefits

- Accidental death and dismemberment benefits

However, OAI usually has lower coverage limits compared to Workers’ Compensation. For instance, while Workers’ Comp often provides unlimited medical benefits, OAI might cap medical coverage at $500,000 or $1,000,000.

Flexibility and Customization

The adaptable nature of OAI allows businesses to customize coverage to their specific needs. This flexibility proves particularly advantageous for industries with unique risk profiles. In the trucking industry, for example, policies can provide coverage on a per-mile basis (aligning with the nature of the work).

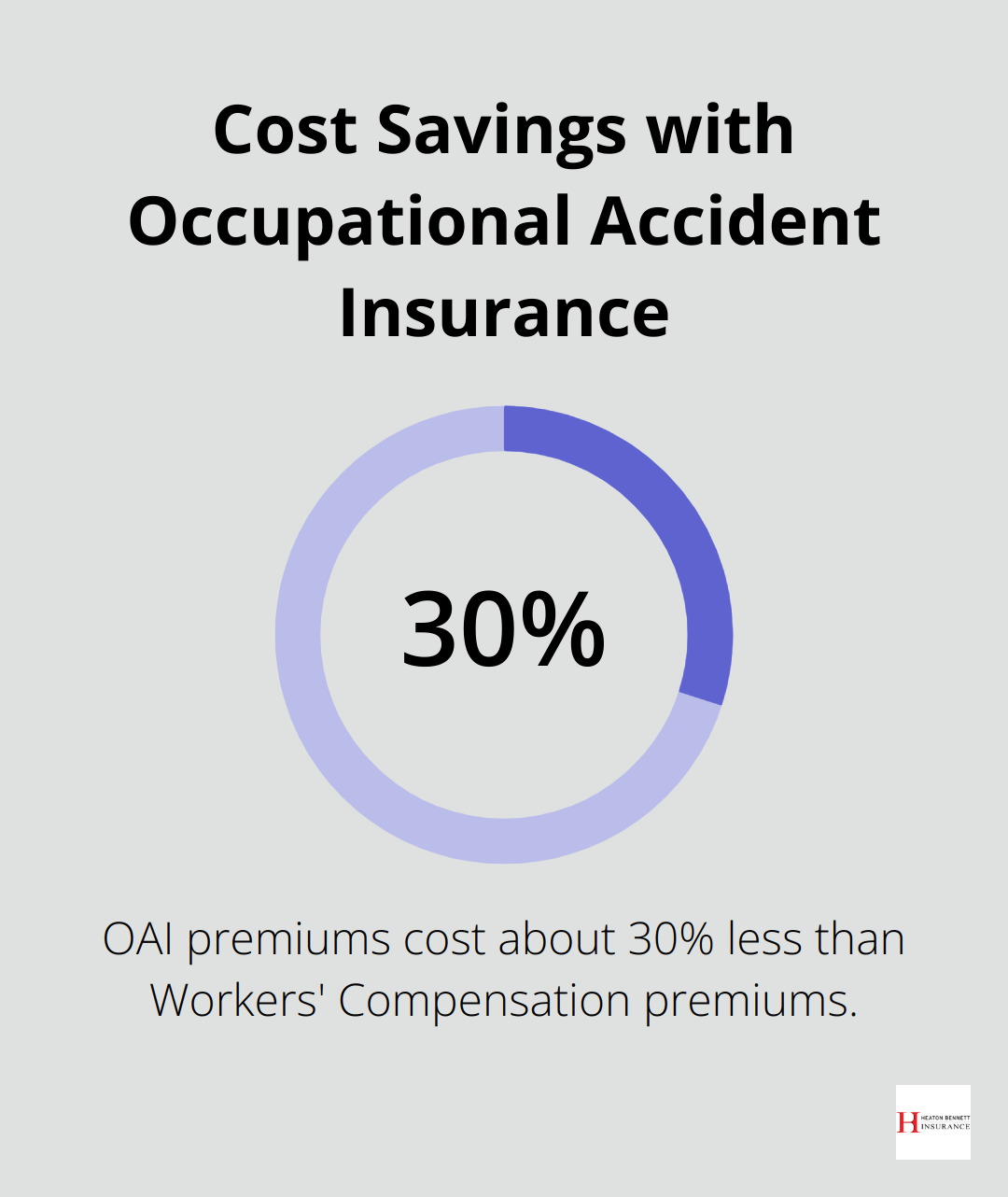

Cost Considerations

One of OAI’s most significant advantages is its cost-effectiveness. On average, OAI premiums cost about 30% less than those for Workers’ Compensation. This can result in substantial savings, especially for businesses with numerous independent contractors.

However, businesses must weigh these savings against potential risks. The lower premiums come with trade-offs in terms of coverage limits and legal protections.

Legal Implications

A critical distinction between OAI and Workers’ Compensation lies in the legal framework. Workers’ Compensation operates on a no-fault system, which generally prevents employees from suing their employers for work-related injuries. OAI doesn’t provide this same level of legal protection.

Under an OAI policy, injured contractors may retain the right to sue for negligence. This potential for litigation is a factor that businesses must carefully consider when choosing between these insurance options.

Evolving Landscape

The landscape of worker classification and insurance requirements continues to change. For example, California’s AB5 law (effective since 2020) has significantly impacted how businesses classify workers. Such changes can affect the applicability and effectiveness of OAI versus Workers’ Compensation.

Insurance professionals must stay informed about these legal developments to provide clients with the most up-to-date information for making insurance decisions. Regular reviews of insurance strategies help ensure alignment with current laws and business needs.

As we move forward, it’s essential to consider various factors when choosing between Workers’ Compensation and Occupational Accident Insurance. Let’s examine these key considerations in the next section.

Making the Right Choice for Your Business

Selecting between Workers’ Compensation and Occupational Accident Insurance significantly impacts your business’s financial health and legal compliance. Here’s what you need to know to make an informed choice.

State-Specific Requirements

You must understand your state’s laws. Texas allows private employers to opt-out of workers’ compensation, while most states mandate it. California’s recent legislation (like AB5) has redefined worker classification, potentially affecting your insurance needs. Always check your state’s current regulations before you decide.

Industry Risk Assessment

Your industry’s risk profile determines the most suitable coverage. High-risk industries like construction or manufacturing often face stricter workers’ compensation requirements and higher premiums. The construction industry experiences a fatality rate nearly three times the average for all industries (according to the Occupational Safety and Health Administration).

Financial Implications

Cost matters, but it shouldn’t be your only consideration. Occupational Accident Insurance typically costs about 30% less than Workers’ Compensation, but it often comes with coverage limits. A typical OAI policy might cap medical benefits at $500,000, while Workers’ Comp usually offers unlimited medical coverage.

Worker Classification

The distinction between employees and independent contractors is important. Misclassifying workers can lead to severe penalties. The IRS estimates that millions of workers are misclassified each year (potentially exposing businesses to significant financial and legal risks).

Coverage Limits and Legal Protection

Workers’ Compensation generally provides broader coverage and stronger legal protection for employers. The “exclusive remedy” provision in most Workers’ Comp policies prevents employees from suing their employers for negligence. OAI doesn’t offer this protection, potentially leaving businesses vulnerable to lawsuits.

If you’re interested in exploring insurance options tailored to your specific needs, consider consulting with an insurance professional who can help you understand your obligations and explore your options.

Final Thoughts

The choice between workers’ compensation and occupational accident insurance impacts your business significantly. Your decision depends on state laws, industry risks, worker classification, and financial considerations. We recommend you assess your business needs thoroughly and understand your legal obligations before making a choice.

Professional guidance can help you navigate this complex decision. At Heaton Bennett Insurance, we offer expert advice tailored to your unique business situation and risk profile. Our team can help you determine the most suitable coverage (workers’ compensation vs occupational accident insurance) for your needs.

Protect your business and workers effectively by making an informed decision about your insurance coverage. Contact insurance professionals who can guide you through this important process. Your choice today will influence your company’s future security and success.