When Is Workers Compensation Insurance Required?

At Heaton Bennett Insurance, we often hear the question: “When do you need workers compensation insurance?” It’s a critical concern for businesses of all sizes.

Workers compensation insurance protects both employers and employees in case of work-related injuries or illnesses. Understanding when this coverage is required can help you stay compliant with the law and protect your business from potential financial risks.

What Is Workers Compensation Insurance?

Definition and Purpose

Workers compensation insurance provides financial protection and medical benefits to employees who suffer job-related injuries or illnesses. This insurance creates a safety net for both employers and employees. It ensures that workers receive necessary medical care and wage replacement if they cannot work due to a work-related incident.

The primary purpose of workers compensation is twofold:

- It protects employees by guaranteeing medical treatment and financial support for work-related injuries or illnesses (regardless of fault).

- It shields employers from potential lawsuits related to workplace injuries.

This system establishes a more stable and predictable environment for all parties involved.

Benefits for Employers and Employees

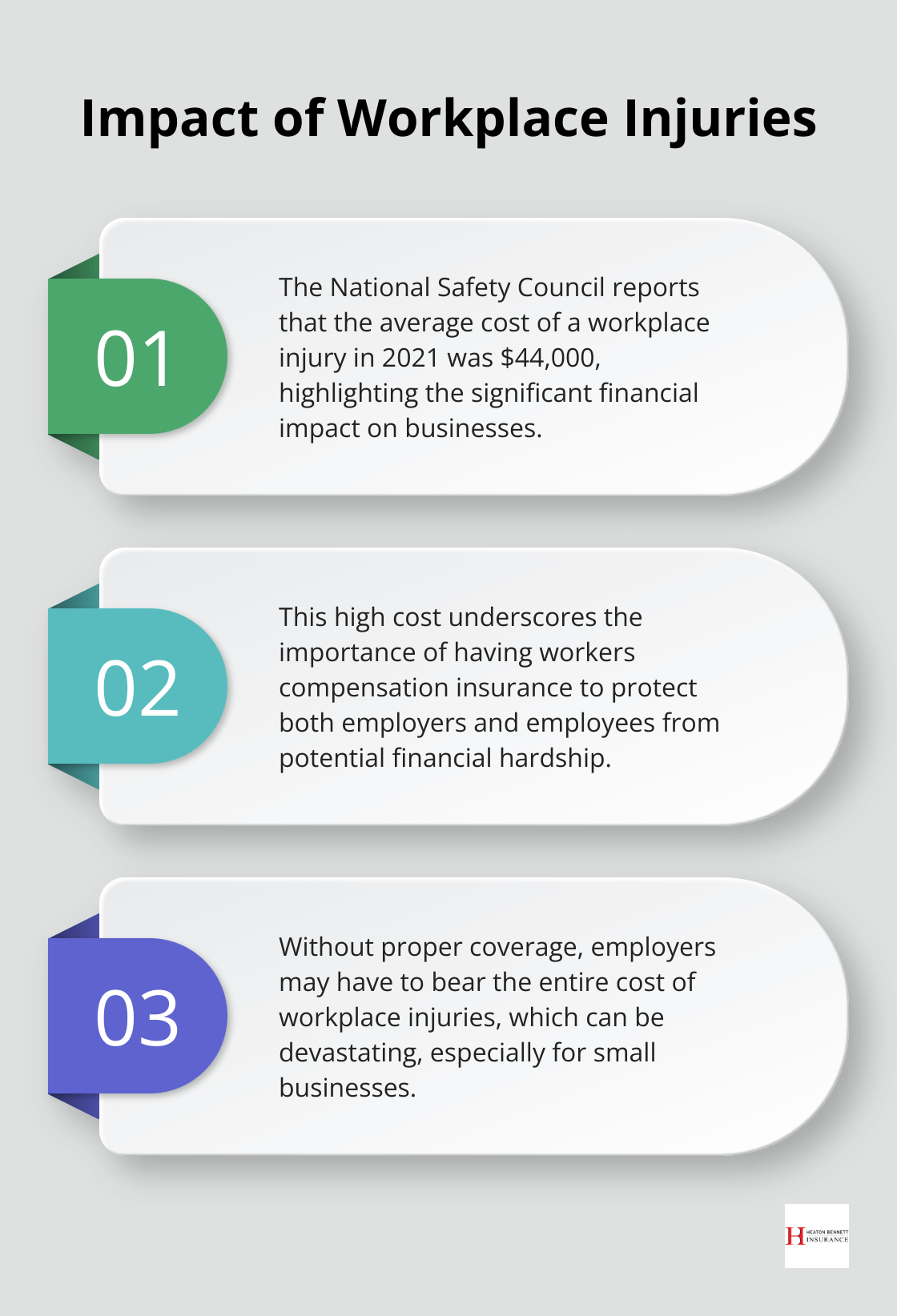

Employees gain peace of mind with workers compensation. They know that if something goes wrong on the job, they will have access to medical care and won’t face financial ruin due to lost wages. The National Safety Council reports that the average cost of a workplace injury in 2021 was $44,000. Workers compensation helps cover these costs, which prevents employees from bearing this substantial financial burden.

For employers, this insurance serves as a critical risk management tool. It protects businesses from potentially devastating lawsuits and helps maintain a productive workforce. The National Academy of Social Insurance reports that workers compensation covered an estimated 142.7 million workers in 2020 (highlighting its widespread importance).

Key Components of Coverage

Workers compensation typically includes several key components:

- Medical benefits: These cover all necessary medical treatment related to the work injury or illness.

- Wage replacement benefits: These provide a portion of lost wages while the employee cannot work.

- Permanent disability benefits: These may be available for long-term or permanent injuries.

- Death benefits: In the most tragic cases, these are provided to the deceased worker’s dependents.

It’s important to note that coverage can vary by state. For example, in Texas (where Heaton Bennett Insurance operates), workers compensation is not mandatory for private employers. However, many businesses still choose to carry it due to its significant benefits.

State-Specific Considerations

Each state has its own workers compensation laws and regulations. These laws determine:

- Which employers must provide coverage

- What injuries and illnesses are covered

- How benefits are calculated and distributed

- The process for filing and resolving claims

Businesses operating in multiple states must comply with the laws in each state where they have employees. This complexity underscores the importance of working with knowledgeable insurance professionals who understand the nuances of workers compensation across different jurisdictions.

As we move forward, it’s essential to understand the legal requirements for workers compensation insurance. Let’s explore the federal and state-specific mandates that govern this critical form of protection.

Who Must Provide Workers Compensation Insurance

State-Specific Mandates

Workers compensation insurance requirements vary significantly across states. Texas (where Heaton Bennett Insurance operates) does not mandate private employers to carry this insurance. However, most states require coverage even for businesses with a single employee.

California enforces workers compensation for all employers, regardless of employee count. New York demands coverage for all for-profit businesses with employees, while non-profits must provide it if they have staff. Florida requires businesses with four or more employees to have coverage, except in construction where all employees must be covered.

Industry-Specific Requirements

Certain industries face stricter regulations due to higher risk factors. Construction stands out as a prime example. Many states, including Florida and New York, mandate construction companies to provide workers compensation insurance for all employees, regardless of company size.

The National Council on Compensation Insurance (NCCI) reports that the construction industry has one of the highest workers compensation claim frequencies (a statistic that underscores the importance of coverage in high-risk sectors).

Small Business Considerations

Small businesses often encounter unique challenges with workers compensation insurance. While some states offer exemptions for very small operations, it’s essential to understand the specific rules in your location.

Illinois automatically excludes sole proprietors and partners from coverage, but they can elect to be included. California, in contrast, requires all businesses to carry workers compensation insurance if they have any employees (even just one).

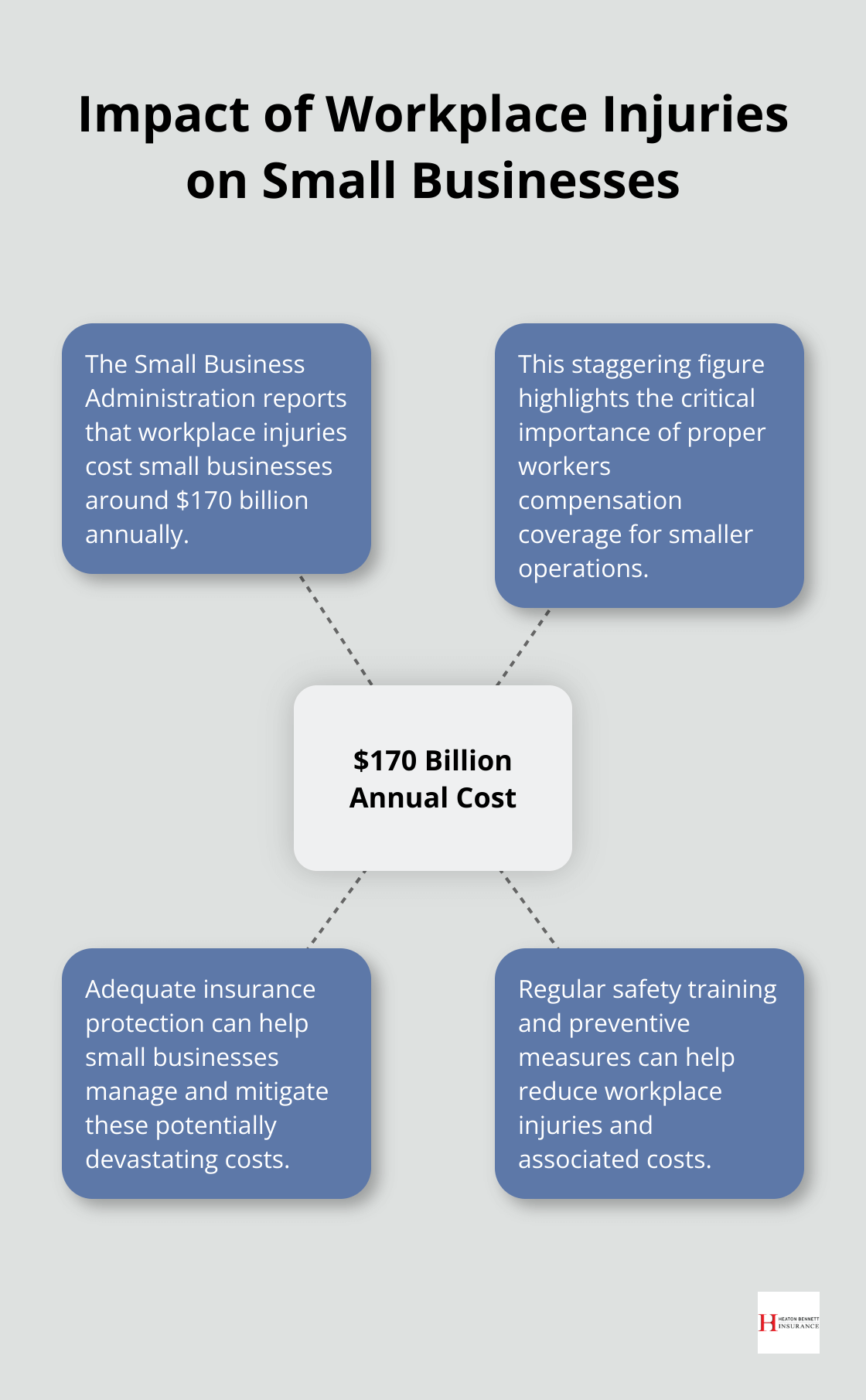

The Small Business Administration reports that workplace injuries cost small businesses around $170 billion annually (a staggering figure that highlights the importance of proper coverage, even for smaller operations).

Navigating Complex Requirements

Understanding these intricate requirements can prove challenging. Working with experienced insurance professionals can provide invaluable assistance. They can help navigate the complexities of workers’ compensation laws and ensure your business remains compliant while protecting both you and your employees.

As we move forward, it’s important to consider exceptions and special cases that may apply to certain businesses or individuals when it comes to workers compensation insurance requirements.

Navigating Workers Comp Exceptions

Small Business Exemptions

Workers compensation insurance requirements vary significantly across states. Texas does not mandate private employers to carry this insurance, regardless of size. This contrasts with other states’ policies. Florida exempts businesses with fewer than four employees (except in construction). California requires all businesses with employees to have coverage, even for one part-time worker.

The National Federation of Independent Business (NFIB) notes that misunderstanding these exemptions often leads to costly penalties for small business owners. It’s essential to check your state’s specific requirements to avoid potential legal issues.

Independent Contractor Considerations

The gig economy has complicated workers compensation requirements. Independent contractors typically don’t receive coverage under a company’s workers compensation insurance. However, the line between employees and contractors isn’t always clear.

The Internal Revenue Service (IRS) uses a 20-factor test to determine worker classification. Misclassifying employees as independent contractors can result in severe penalties. In California, the penalty for willful misclassification ranges from $5,000 to $25,000 per violation.

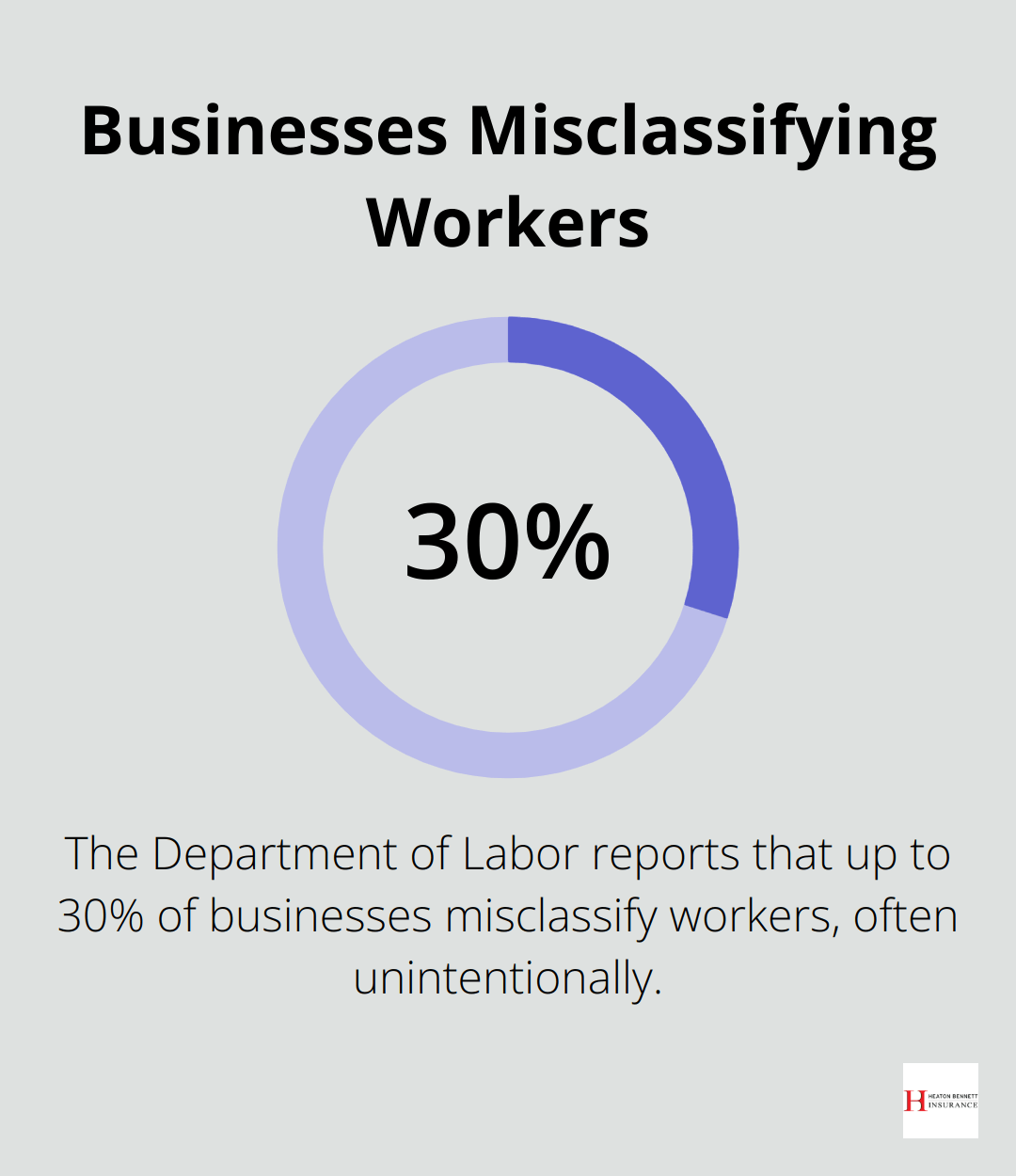

The Department of Labor reports that up to 30% of businesses misclassify workers (often unintentionally). When uncertain about a worker’s status, it’s prudent to consult with a legal professional or consider providing coverage.

Voluntary Coverage Options

Businesses exempt from mandatory workers compensation insurance might still benefit from voluntary coverage. The National Safety Council reports that the average cost of a medically consulted work injury in 2020 was $44,000. Without insurance, employers bear this entire cost.

Voluntary coverage protects businesses from potentially devastating expenses. It also demonstrates a commitment to employee welfare, which can boost morale and attract talent. A study by the Society for Human Resource Management found that 92% of employees rated benefits as important to their overall job satisfaction.

Many business owners find that the protection and peace of mind provided by voluntary coverage justify the additional expense. Regular consultations with insurance professionals (such as those at Heaton Bennett Insurance) can help ensure compliance and adequate protection.

Industry-Specific Exceptions

Certain industries face unique workers compensation requirements. Construction, for example, often has stricter regulations due to higher risk factors. In Florida and New York, construction companies must provide workers compensation insurance for all employees, regardless of company size.

The National Council on Compensation Insurance (NCCI) reports that the construction industry has one of the highest workers compensation claim frequencies. This statistic underscores the importance of coverage in high-risk sectors.

Navigating Changing Regulations

Workers compensation laws evolve constantly. What applies today might change tomorrow. Businesses must stay informed about these changes to maintain compliance and adequate protection. Regular reviews of insurance policies and consultations with professionals can help businesses adapt to new regulations and avoid potential penalties.

Final Thoughts

Workers compensation insurance requirements vary by state, industry, and company size. Most employers must provide this coverage, but even in states like Texas where it’s not mandatory, many businesses choose it for its benefits. The average cost of a workplace injury can reach tens of thousands of dollars, making insurance a vital safeguard for businesses.

Heaton Bennett Insurance specializes in providing tailored insurance solutions for businesses. Our team can guide you through the complexities of workers compensation laws, helping ensure you have the right coverage for your specific needs. We offer personalized service to help you determine when you need workers compensation insurance.

Workers compensation requirements can change, and staying informed is key to maintaining compliance. Regular reviews of your insurance policies and consultations with professionals can help your business adapt to new regulations and avoid potential penalties. In today’s dynamic business environment, having the right insurance coverage protects your company and employees.