Do Nannies Need Workers Compensation Insurance?

At Heaton Bennett Insurance, we often field questions about nanny workers compensation insurance. Many families are unsure whether they need this coverage for their childcare providers.

The answer isn’t always straightforward, as it depends on various factors including state laws and employment arrangements.

In this post, we’ll explore the ins and outs of workers’ compensation for nannies, helping you make an informed decision for your family and your caregiver.

What Is Workers Compensation Insurance?

The Foundation of Workplace Safety

Workers compensation insurance forms a critical safety net for employers and employees alike. This insurance covers medical expenses and lost wages for workers who suffer injuries or illnesses due to their job. In most states, it’s not optional-it’s a legal requirement for employers.

Coverage in Action

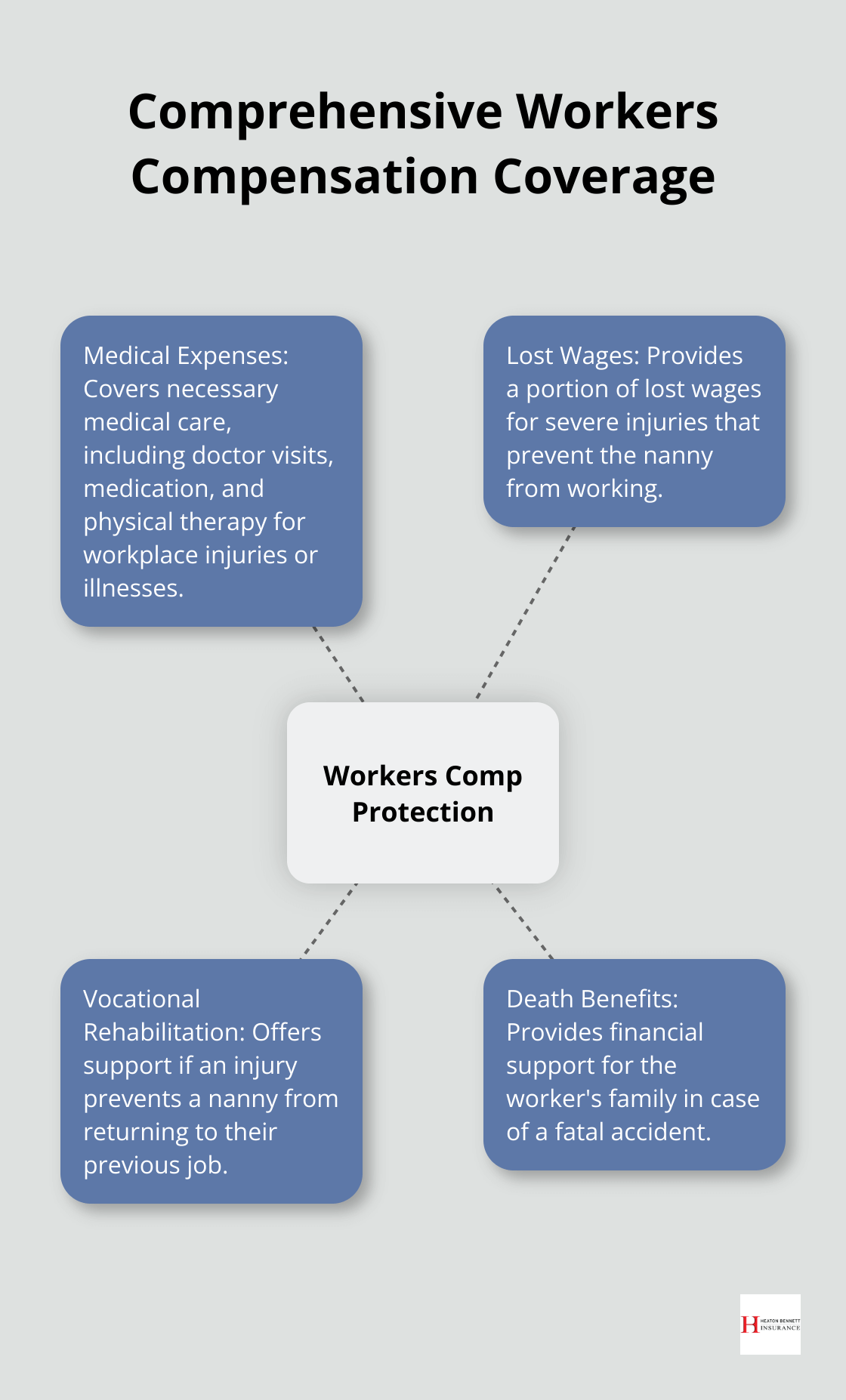

When a nanny experiences a workplace accident (such as slipping on a wet floor or injuring their back while lifting a child), workers comp steps in. It pays for necessary medical care, including doctor visits, medication, and physical therapy. For severe injuries that prevent the nanny from working, it also provides a portion of their lost wages.

The National Safety Council reports that the average workers compensation claim in 2020 amounted to $41,353. This substantial sum underscores the importance of proper coverage, as most families can’t afford such unexpected costs out-of-pocket.

State-Specific Regulations

Each state sets its own rules for workers compensation. For instance:

- California requires coverage if you pay a nanny more than $100 in a calendar quarter.

- Texas doesn’t mandate it for household employees.

It’s essential to check your state’s specific laws. Non-compliance can result in fines, penalties, and (in some cases) criminal charges.

Comprehensive Protection

Workers comp extends beyond basic medical coverage. It can include:

- Vocational rehabilitation (if an injury prevents a nanny from returning to their previous job)

- Death benefits for the worker’s family (in case of a fatal accident)

For nannies, this coverage provides peace of mind. They can focus on childcare without worrying about potential workplace injuries.

The Employer’s Perspective

From an employer’s standpoint, workers comp offers protection against potential lawsuits related to workplace injuries. It creates a safer work environment and demonstrates a commitment to your employees’ well-being.

As we move forward, let’s examine how these general principles of workers compensation apply specifically to nannies and the families who employ them.

Do Nannies Need Workers Comp?

Employment Status: A Key Factor

The need for workers compensation insurance for nannies primarily depends on their employment status. Full-time nannies who work regular hours typically require coverage. For example, if a nanny works 40 hours a week, most states will classify them as a full-time employee, necessitating coverage.

Part-time or occasional nannies might fall under different rules. In Texas, household employers don’t need to carry workers comp for any domestic workers. However, California requires coverage if you pay a nanny more than $100 in a calendar quarter.

State Laws: A Patchwork of Regulations

State regulations dictate your obligations as an employer. Here are some examples:

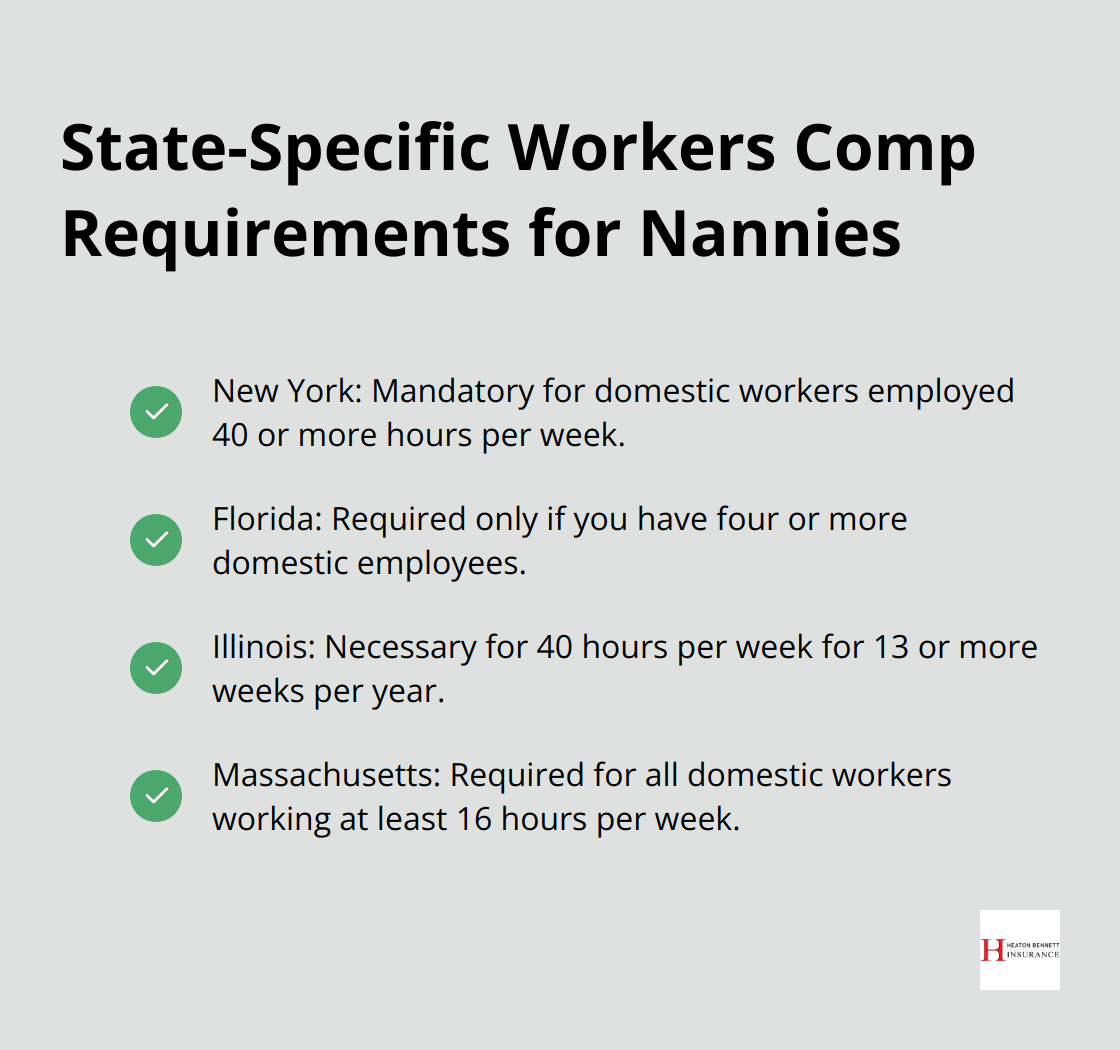

- New York mandates coverage for domestic workers employed 40 or more hours per week.

- Florida only requires it if you have four or more domestic employees.

- Illinois sets the threshold at 40 hours per week for 13 or more weeks per year.

- Massachusetts requires coverage for all domestic workers working at least 16 hours per week.

These variations highlight the importance of checking your specific state laws. An experienced insurance agent can help you navigate these state-specific requirements to ensure compliance.

Financial Implications: Weighing the Costs

The cost of workers comp might seem significant, but consider the potential financial impact of not having it. The National Council on Compensation Insurance reports that the average cost for workers comp for domestic employees is about $0.75 per $100 of payroll.

Now, compare this to the potential out-of-pocket costs of a workplace injury. A simple slip and fall could result in thousands of dollars in medical bills and lost wages. Without coverage, you’d be personally liable for these expenses.

Legal Protection: Shielding Yourself from Lawsuits

Workers compensation insurance provides legal protection for employers. When an employee accepts workers comp benefits, they generally waive their right to sue their employer for the injury. This can save you from potentially costly legal battles and settlements.

Employee Benefits: Attracting and Retaining Quality Nannies

Offering workers compensation can make you a more attractive employer to high-quality nannies. It shows that you value their well-being and are committed to providing a safe work environment. This can lead to better retention rates and a more stable childcare situation for your family.

As we move forward, let’s examine the pros and cons of providing workers compensation for nannies, weighing the benefits against the potential drawbacks.

The Hidden Costs of Skipping Nanny Workers Comp

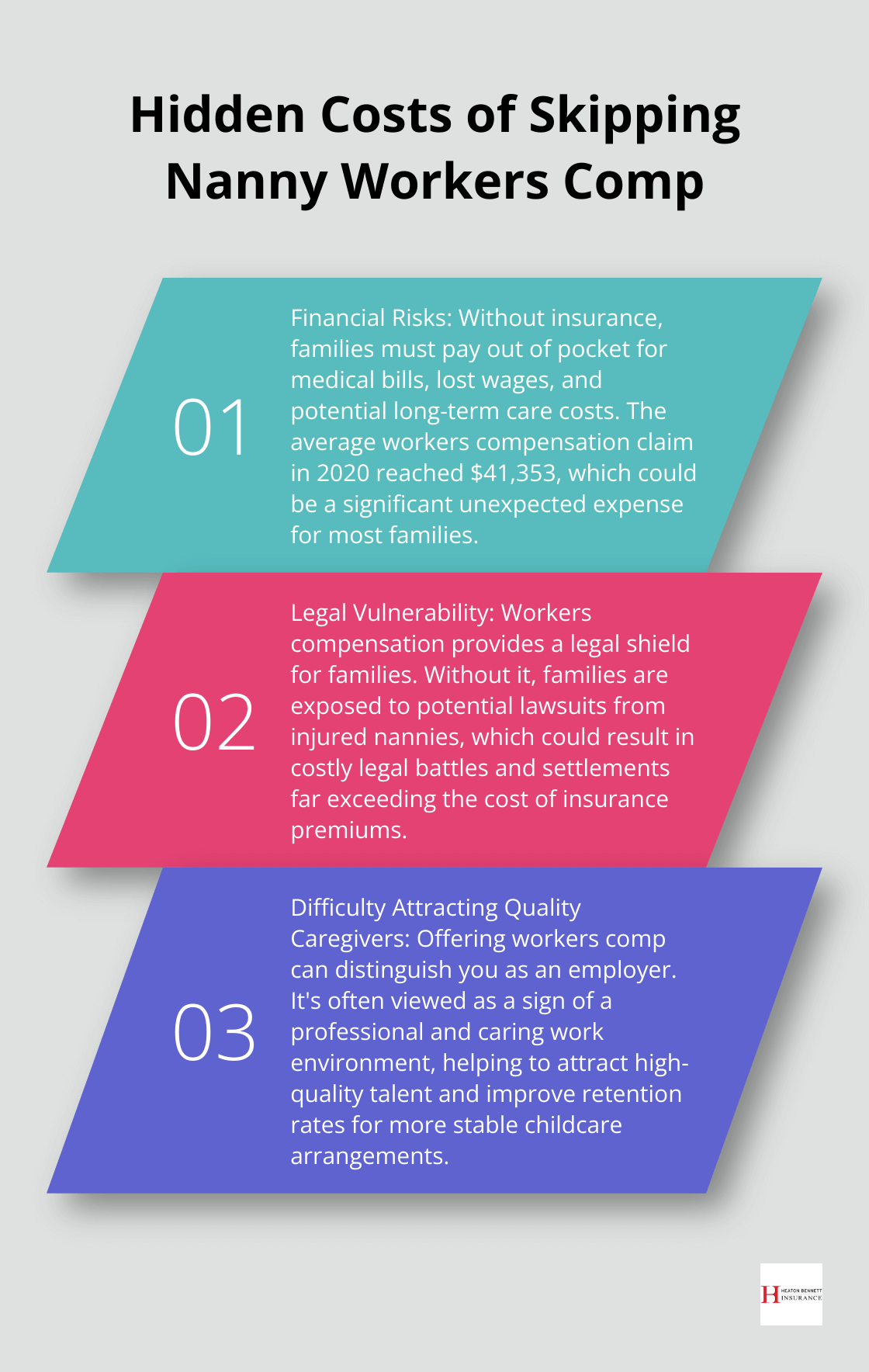

The cost of a workplace injury can shock many families. The National Safety Council reports that the average workers compensation claim in 2020 reached $41,353. Without insurance, families must pay medical bills, lost wages, and potential long-term care costs out of pocket. A simple fall or back injury could result in thousands of dollars in unexpected expenses.

Financial Risks of Uninsured Workplace Injuries

The cost of a workplace injury can shock many families. The National Safety Council reports that the average workers compensation claim in 2020 reached $41,353. Without insurance, families must pay medical bills, lost wages, and potential long-term care costs out of pocket. A simple fall or back injury could result in thousands of dollars in unexpected expenses.

Legal Vulnerability for Families

Workers compensation provides a powerful legal shield. When nannies accept these benefits, they typically waive their right to sue the family for the injury. This protection can save families from expensive legal battles and potential settlements that could far exceed the cost of insurance premiums.

Attracting Top-Tier Caregivers

Offering workers comp can distinguish you as an employer. Nannies often view this benefit as a sign of a professional and caring work environment. It can help you attract high-quality talent and improve retention rates, which leads to more stable childcare arrangements for your family.

The Actual Cost of Coverage

While the expense of workers comp might appear daunting, it’s often more affordable than families expect. The National Council on Compensation Insurance reports that the average cost for domestic employees is about $0.75 per $100 of payroll. For a nanny earning $30,000 annually, that’s roughly $225 per year (a small price for comprehensive protection).

Positive Impact on Working Relationships

Providing workers comp can foster a positive employer-employee relationship. It shows that you value your nanny’s well-being and commit to their safety. This can result in increased job satisfaction, loyalty, and a more harmonious household (benefits that extend far beyond the financial aspects).

Final Thoughts

Nanny workers compensation insurance protects both families and caregivers from financial and legal risks. This coverage offers peace of mind and demonstrates a commitment to your nanny’s well-being. The modest cost of premiums pales in comparison to the potential out-of-pocket expenses of a workplace injury (which can exceed $40,000).

We at Heaton Bennett Insurance recommend considering workers compensation insurance for your nanny, even if your state doesn’t mandate it. This insurance creates a safer, more secure environment for everyone involved. It also helps attract and retain high-quality caregivers, fostering a positive working relationship.

If you need guidance on your insurance options, our team at Heaton Bennett Insurance can help. We specialize in tailored insurance solutions for families and businesses in Austin, Texas. Our experts will ensure you have the right coverage without unnecessary extras, allowing you to focus on what matters most: the care and well-being of your children.