Construction Contractor Insurance: Coverage for Building Projects

Construction projects face real financial risks. One accident, weather delay, or property damage claim can derail your entire operation and drain your budget.

At Heaton Bennett Insurance, we know that construction contractor insurance isn’t optional-it’s the foundation of a sustainable business. The right coverage protects your assets, your team, and your bottom line.

Essential Coverage Types for Contractors

General Liability: Your First Line of Defense

General liability insurance stands as the most fundamental protection you need, and it’s non-negotiable. This coverage protects you when a third party claims bodily injury or property damage from your work. According to the National Safety Council, the average cost of a workplace injury claim in 2022 was $40,000-a figure that shows why third-party liability exposure matters tremendously. Most states require minimum general liability limits around $1 million per occurrence before you can bid on projects. Median monthly costs run about $80, making this one of your cheapest defenses against catastrophic financial loss.

The policy covers injuries from falling debris, damage to nearby properties, and personal injury claims from your operations. Without it, a single accident drains your business reserves and potentially forces closure.

Workers’ Compensation: Protecting Your Team and Your Business

Workers’ compensation coverage is legally mandatory in Massachusetts if you have employees, and it’s your second critical layer of protection. This coverage pays medical expenses, lost wages, disability benefits, and employer liability claims when your team gets injured on the job. Median monthly costs sit around $254, though high-risk trades like roofing pay substantially more. The policy protects both your workers and your business from the financial impact of on-site injuries.

Builder’s Risk and Additional Property Coverage

Builder’s risk insurance protects the actual structure, materials, temporary structures, and debris removal during construction. This policy typically costs between 1% and 5% of total project value, with basic policies starting around $375. It covers soft costs like additional loan interest and legal fees when weather or other events delay your project. Many project owners or lenders require builder’s risk before work begins, making it essential for winning bids.

Inland marine coverage insures tools, equipment, and materials in transit or stored off-site, costing roughly $14 per month and filling critical gaps that builder’s risk alone cannot cover. Commercial auto insurance protects company vehicles used to transport supplies and equipment, running about $173 monthly and providing essential liability protection for accidents. Professional liability insurance shields you from design errors and omissions claims, costing around $74 monthly depending on your service scope.

These coverages work together to address the real risks that destroy construction businesses every year. The next section examines the specific claims and risk factors that make this protection indispensable.

What Really Causes Construction Claims

On-Site Injuries: The Silent Profit Killer

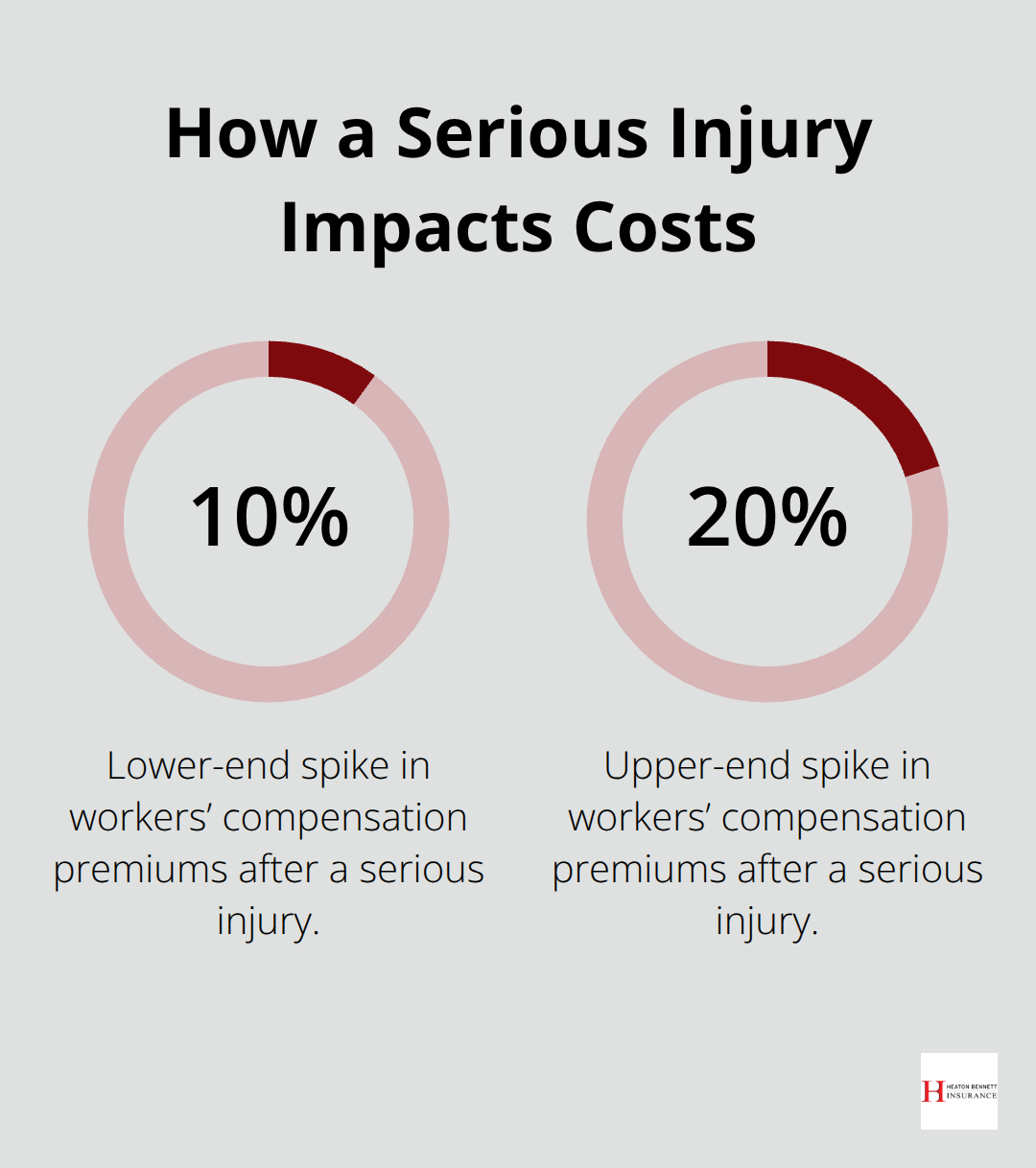

On-site injuries represent the single largest claim driver in construction, and the numbers are brutal. The National Safety Council reported that the average workplace injury claim cost $40,000 in 2022, but that figure masks the true financial damage. A serious injury spikes your workers’ compensation premiums by 10 to 20 percent for years, destroys your safety record with insurance carriers, and forces you to turn down profitable projects because underwriters won’t touch your account.

Falls, electrocution, and caught-between incidents dominate OSHA’s Focus Four hazards, yet many contractors treat safety as a compliance checkbox rather than a profit protector.

The reality cuts sharper: contractors with documented safety programs and regular training reduce injury frequency and qualify for better premium rates. If you don’t track near-misses, conduct daily toolbox talks, or maintain detailed safety records, you leave money on the table and expose your business to preventable claims that follow you for years.

Third-Party Liability: When Your Work Damages Others’ Property

Third-party property damage and liability claims strike differently but hit just as hard. A falling beam that damages a neighboring structure, a concrete truck that tears up a client’s driveway, or debris that injures a passerby creates immediate legal exposure and exhausts your general liability limits fast. These incidents happen without warning and demand immediate legal defense, which your general liability policy covers-but only if your limits match the severity of the claim.

Weather Delays and Material Loss: Hidden Margin Destroyers

Weather-related delays compound this risk in ways many contractors underestimate. The construction industry in 2023 faced roughly $12 billion in material theft and damage, and severe weather accounts for a substantial portion of that loss. When a spring storm delays your project by three weeks, builder’s risk coverage pays those soft costs like additional loan interest and extended financing fees that drain profits silently. Without it, weather delays become pure losses absorbed directly from your margin.

Location and Trade-Specific Risks Shape Your Coverage Needs

Coastal projects face higher wind and hail exposure, urban sites attract more theft and vandalism, and winter projects in cold climates demand different risk strategies than summer work. The contractors who win bids consistently and protect their margins don’t just buy insurance-they map project-specific risks upfront, identify which coverage gaps matter most for their location and trade, and structure their policies to address the exact exposures their work creates. Understanding these location-based and trade-specific exposures positions you to select the right coverage limits and endorsements before you bid on your next project.

Selecting Insurance That Matches Your Project Reality

Map Your Actual Project Exposures First

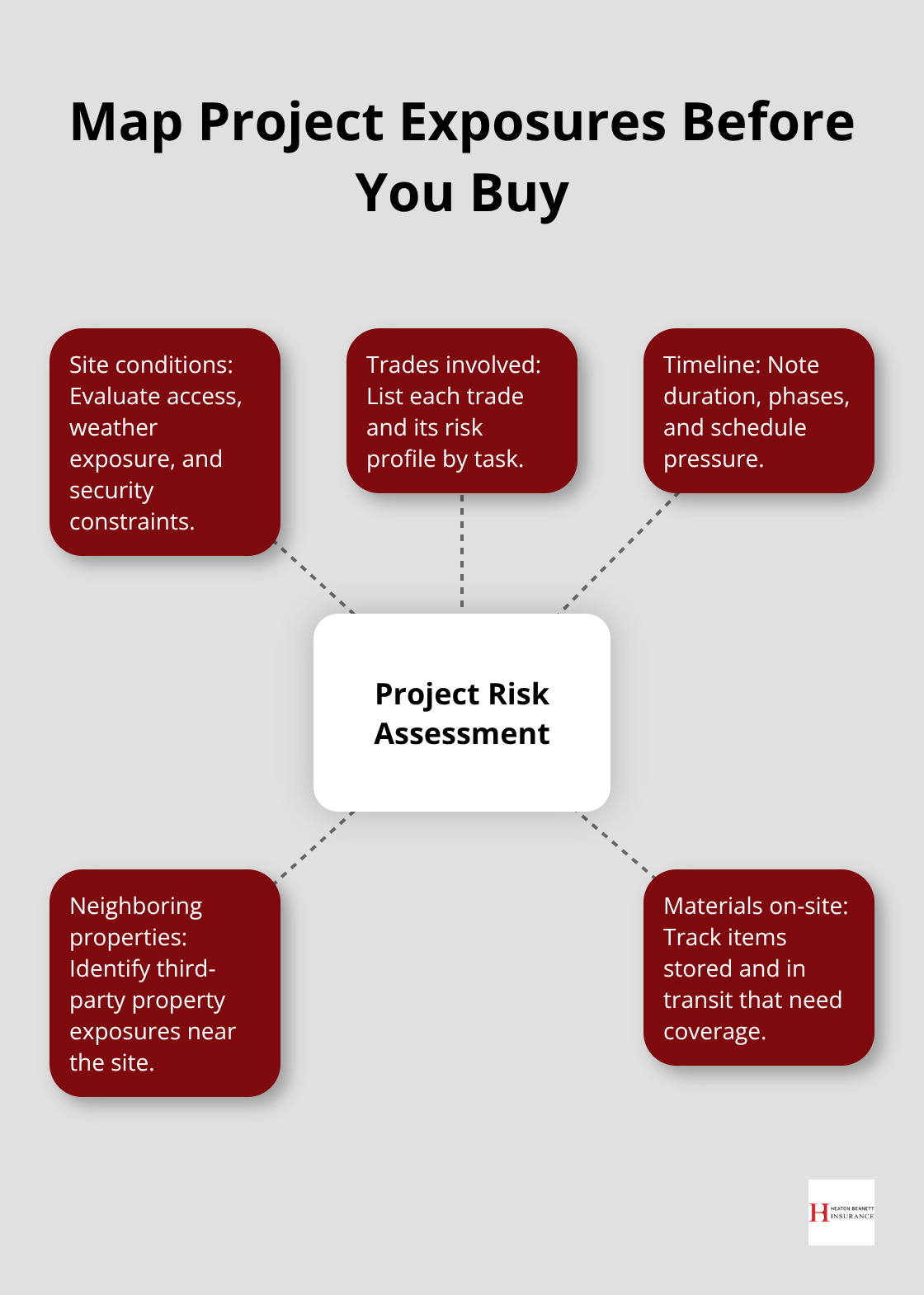

Start with your next project site and identify the specific exposures that will actually cost you money. A residential renovation in an urban neighborhood faces theft and vandalism risks that a rural commercial project never touches. A coastal project demands higher wind coverage limits than inland work. A roofing job creates different liability exposures than concrete finishing. Too many contractors purchase generic coverage packages designed for every project and overpay for protection they don’t need while leaving critical gaps uncovered. The National Safety Council data showing $40,000 average injury claims and the construction industry’s $12 billion in 2023 material theft and damage losses prove that one-size-fits-all insurance fails when real claims arrive.

Document the site conditions, the trades involved, the timeline, the neighboring properties at risk, and the materials you’ll store on-site. This assessment takes two hours and drives every coverage decision that follows. A builder’s risk policy written for a six-month project costs far less than one covering eighteen months, and the premium difference matters when you’re bidding tight margins.

Tailor Coverage Limits to Your Trade and Project Type

Professional liability limits that work for design-build contractors won’t protect architects handling complex specifications. Workers’ compensation rates spike dramatically for roofing and fall-protection trades compared to office-based work. Your project profile determines what you actually need to purchase. A $1 million general liability limit sounds standard until a third-party claim reaches $1.5 million and your business absorbs the excess.

Higher deductibles lower your monthly premiums substantially, but only if you can actually cover those deductibles when a claim arrives. Commercial auto coverage should include hired and non-owned vehicle protection if your team drives client vehicles or rents equipment transport trucks, exposing you to liability gaps without proper endorsements. Inland marine coverage for tools and equipment in transit prevents devastating losses when a truck carrying $50,000 in specialized equipment gets stolen between job sites.

Compare Multiple Quotes and Scrutinize Policy Details

Comparing quotes from multiple carriers reveals how dramatically coverage scope and price vary across insurers. Most contractors stop after requesting three quotes when they should push to five or six. AM Best ratings of A- or better signal financial strength and reliable claims handling when you need it most, yet many agents never mention this metric.

Request specific limits that match your project risk rather than accepting default minimums, and scrutinize what each policy excludes because those gaps become your financial responsibility. An independent agent who works with construction contractors understands these nuances far better than a generalist agent selling auto insurance to residential customers.

Start the Insurance Conversation Early in Your Project Timeline

Timing matters significantly: builder’s risk coverage becomes difficult and expensive to obtain after a project reaches 30 percent completion. Start the insurance conversation during the permitting phase rather than waiting until you break ground. The right agent asks hard questions about your operations, your claims history, your safety programs, and your growth plans before recommending limits and deductibles. This approach prevents costly coverage gaps and ensures your protection matches the real risks your projects face.

Final Thoughts

Construction contractor insurance protects your business from the financial devastation that follows a single accident, weather delay, or property damage claim. General liability, workers’ compensation, and builder’s risk coverage form the foundation of a sustainable operation, but the real protection comes from matching your coverage to the specific risks your projects face. A $40,000 average injury claim, $12 billion in annual material theft and damage, and the constant threat of weather delays prove that generic insurance packages fail when claims arrive.

The contractors who win bids consistently and protect their margins do not treat construction contractor insurance as a compliance requirement. They map project-specific exposures upfront, tailor coverage limits to their trade and location, and start the insurance conversation during the permitting phase rather than scrambling at the last minute. They understand that higher deductibles lower premiums, that AM Best ratings signal financial strength, and that inland marine coverage prevents devastating losses when equipment disappears between job sites.

Your next project starts with a conversation about the real exposures you face. Contact Heaton Bennett Insurance to discuss how construction contractor insurance protects your business and positions you to bid confidently on larger, more profitable work.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.