Construction Contractor Insurance: A Practical Guide to Protection

Construction sites present real risks-from slip-and-fall accidents to equipment theft. The right construction contractor insurance protects your business from these costly claims and keeps your operations running smoothly.

At Heaton Bennett Insurance, we help contractors understand what coverage they actually need. This guide walks you through the essential policies, common claims to avoid, and how to choose the right protection for your specific projects.

What Coverage Do Construction Contractors Actually Need?

General Liability and Workers’ Compensation Form Your Foundation

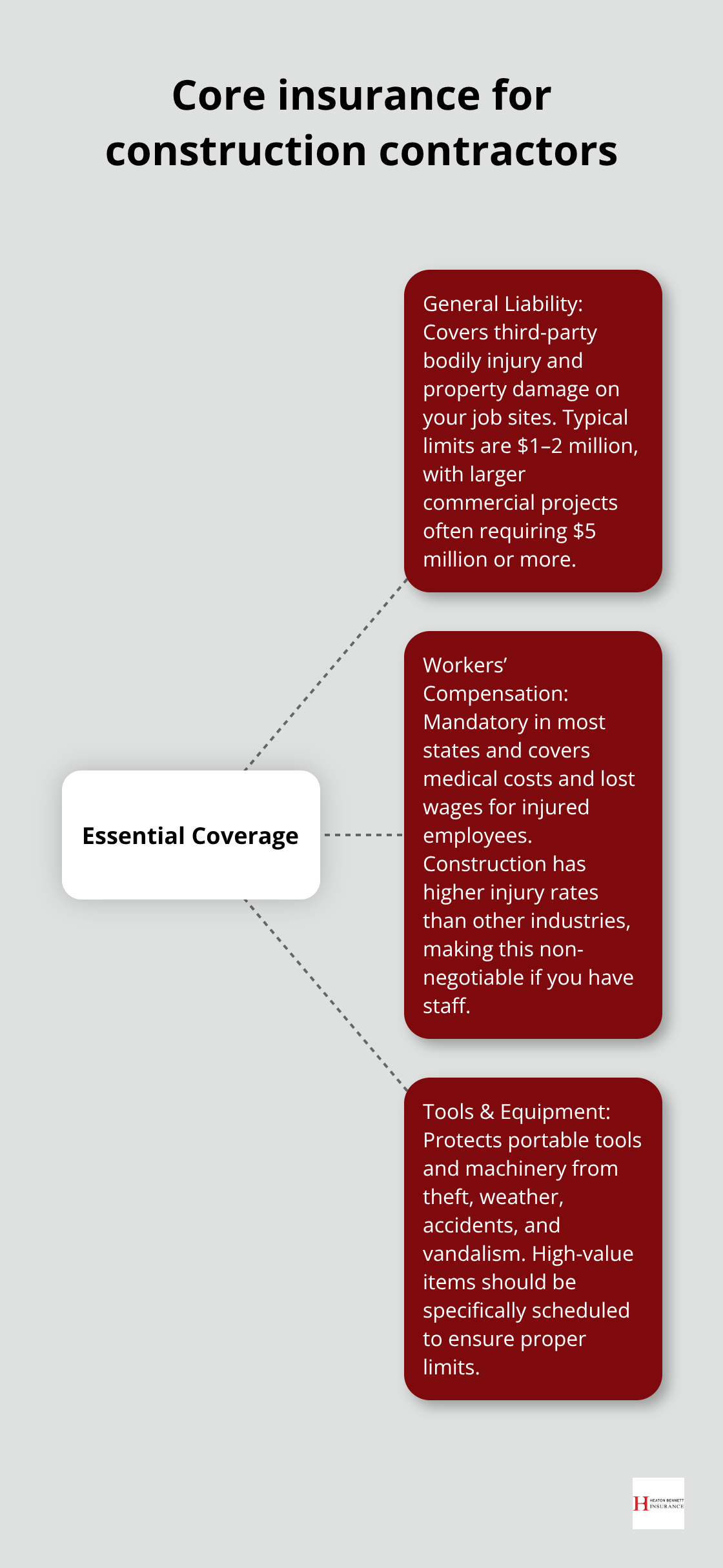

General liability insurance covers bodily injury and property damage claims that occur on your job sites. If a client gets hurt or you accidentally damage their building, this policy pays legal fees and settlements. Most contractors carry $1–2 million in coverage for standard projects, though larger commercial work often requires $5 million or more.

Workers’ compensation is mandatory in all states except Texas and South Carolina, and it covers medical costs and lost wages when your employees get injured. Construction workers face injury rates significantly higher than other industries, making this coverage non-negotiable if you have any staff. The National Safety Council reports that construction accounts for roughly 11% of all workplace deaths despite representing only 6% of the workforce-a stark reality that shows why workers’ comp costs money upfront but protects you from catastrophic financial exposure.

Tools and Equipment Require Specific Coverage

Tools and equipment coverage is where many contractors get blindsided. Job site theft happens regularly, and standard business policies often exclude or severely limit coverage for portable equipment. You need to specifically schedule expensive tools, generators, and machinery on your policy to protect them properly.

Equipment left at a site overnight faces higher theft risk. Some contractors use GPS trackers or secure storage to lower premiums and reduce losses. Property damage from weather, accidents, or vandalism also requires specific coverage limits on your policy. Contractors working on multiple sites simultaneously need to understand that coverage follows the tools themselves, not just the job location.

The Real Cost of Unprotected Assets

Without dedicated equipment protection, a stolen $15,000 compressor or damaged $8,000 air handler becomes your direct loss. The right policy structure means you get back to work faster without absorbing massive replacement costs out of pocket. This layer of protection separates contractors who recover quickly from those who face serious cash flow problems after a loss.

Understanding what coverage you actually need sets the stage for the next critical step: recognizing which claims happen most often and how to prevent them before they drain your resources.

Where Most Construction Claims Actually Come From

Slip-and-Fall Accidents Cost More Than You Think

Slip-and-fall accidents dominate construction insurance claims, and they’re far more expensive than most contractors realize. The Bureau of Labor Statistics reports that falls account for roughly 35% of all construction worker deaths and generate massive workers’ compensation payouts. A single serious fall costs $50,000 to $500,000 in medical bills and lost time, depending on injury severity.

The problem isn’t random-it happens on wet surfaces, uneven ground, scaffolding, and roofs where contractors cut corners on safety protocols. Temperature and weather conditions matter too; wet or icy conditions demand additional precautions and sometimes work stoppage.

Prevention Strategies That Actually Work

You prevent these claims by enforcing site-specific safety plans, requiring harnesses at heights above 6 feet, and maintaining clear walkways free of debris and cords. Daily equipment inspections catch hazards before they cause injuries. OSHA-certified training cuts injury rates by 20% to 30% according to workplace safety research, yet many contractors skip formal safety programs entirely.

Property Damage Claims Hit Harder Than Equipment Theft

Property damage claims from contractor negligence involve third-party property and client relationships, making them far more damaging than equipment theft. Accidentally damaging a client’s existing structure, plumbing system, electrical lines, or finished work during your project creates liability claims that reach six figures.

These claims happen when contractors fail to locate underground utilities before digging, apply incorrect materials, or leave job sites unsecured allowing weather damage to client property. Pre-project utility marking through 811 One-Call services (free in most states) prevents costly mistakes. Written scope agreements that specify what you will and won’t touch protect both parties. Daily site documentation with photos creates a clear record of conditions.

Equipment Theft and Damage Require Layered Protection

Equipment theft and damage losses represent the third major claim category, but contractors can prevent them through scheduled tools on your policy, GPS tracking devices on high-value equipment, and secure overnight storage or locked containers. Theft-resistant locks add another barrier against loss.

Contractors who photograph all tools and equipment before jobs start achieve dramatically faster claim resolution because documentation proves what was on-site. The National Insurance Crime Bureau tracks construction equipment theft as a $300 million annual problem, making prevention strategies worth the upfront investment in security measures and proper coverage limits.

Understanding these three claim categories shows you exactly where your business faces the biggest financial exposure. The next step involves selecting the right coverage limits and policy structure to match your specific operation.

Matching Coverage to Your Actual Risk Profile

Project Type Determines Your Coverage Limits

Your project type determines what coverage limits you genuinely need, and guessing wrong costs you thousands. A residential remodel crew carrying $2 million in general liability might be overinsured while severely underprotected on equipment, whereas a commercial foundation contractor needs $5 million minimum because structural damage claims reach six figures instantly. Start with your past three years of projects and identify which ones generated claims or near-misses. If you’ve never had a property damage claim but lost $40,000 in equipment theft, your priority shifts dramatically toward scheduled tools coverage rather than raising liability limits.

Commercial clients almost always require proof of $1–5 million in liability before signing contracts, so check your client agreements to see what they demand. Residential work typically settles at $1–2 million. Heavy equipment operators and demolition contractors face higher exposure than finish carpenters, so your specific trade matters more than industry averages.

Compare Quotes Across Multiple Carriers

Quotes from different carriers vary wildly because underwriters assess risk differently, making comparison shopping non-negotiable. Request quotes from at least three carriers and ask each one why their premium differs from competitors, because the reasons reveal coverage gaps you might have missed. One carrier might exclude equipment left unattended overnight while another includes it at no extra cost. A $3,000 annual premium difference over five years represents $15,000 in real money, yet contractors often accept the first quote they receive.

When comparing quotes, verify each one covers your specific project types, includes workers’ comp if you have employees, and schedules your most expensive tools. This transparency prevents surprises when claims happen and protects what matters most to your business.

Work with an Independent Agent for Customized Solutions

An independent agent who represents multiple companies can show you cost differences side-by-side and explain exactly what you gain or lose with each option. This approach prevents you from accepting a one-size-fits-all policy that leaves gaps in your protection. The agent identifies which carriers offer the best rates for your specific operation and trade, rather than forcing you into limited options.

Final Thoughts

Construction contractor insurance protects your business when claims happen, and the three coverage types we’ve covered-general liability, workers’ compensation, and tools and equipment protection-address the real financial threats your operation faces daily. Slip-and-fall accidents, property damage from negligence, and equipment theft represent the claims that actually drain contractor bank accounts, and the right policies stop that drain before it starts. You need to pull your past three years of project records, identify which ones created risk or generated claims, and use that information to guide your coverage decisions.

Request quotes from at least three different insurance carriers and compare what each one covers for your specific trade and project types. An independent agent who represents multiple carriers can show you cost differences side-by-side and explain exactly what you gain or lose with each option, preventing you from accepting a one-size-fits-all policy that leaves gaps in your protection. This approach ensures you pay for coverage you actually need rather than overpaying for unnecessary protection.

When you work with Heaton Bennett Insurance, you gain access to multiple carriers instead of being locked into one company’s limited options. Construction contractor insurance becomes a business investment that protects your ability to take on bigger projects, bid on commercial work that requires proof of coverage, and recover quickly when accidents occur. The contractors who thrive long-term treat insurance as essential protection, not an expense to minimize.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.