EPLI Insurance Cost A Breakdown for Businesses

EPLI insurance cost varies dramatically depending on your business size, industry, and hiring practices. Most companies underestimate how much they’ll pay until they get their first quote.

We at Heaton Bennett Insurance help businesses understand what drives these costs and how to control them. This breakdown shows you exactly what to expect.

What Really Drives Your EPLI Insurance Price

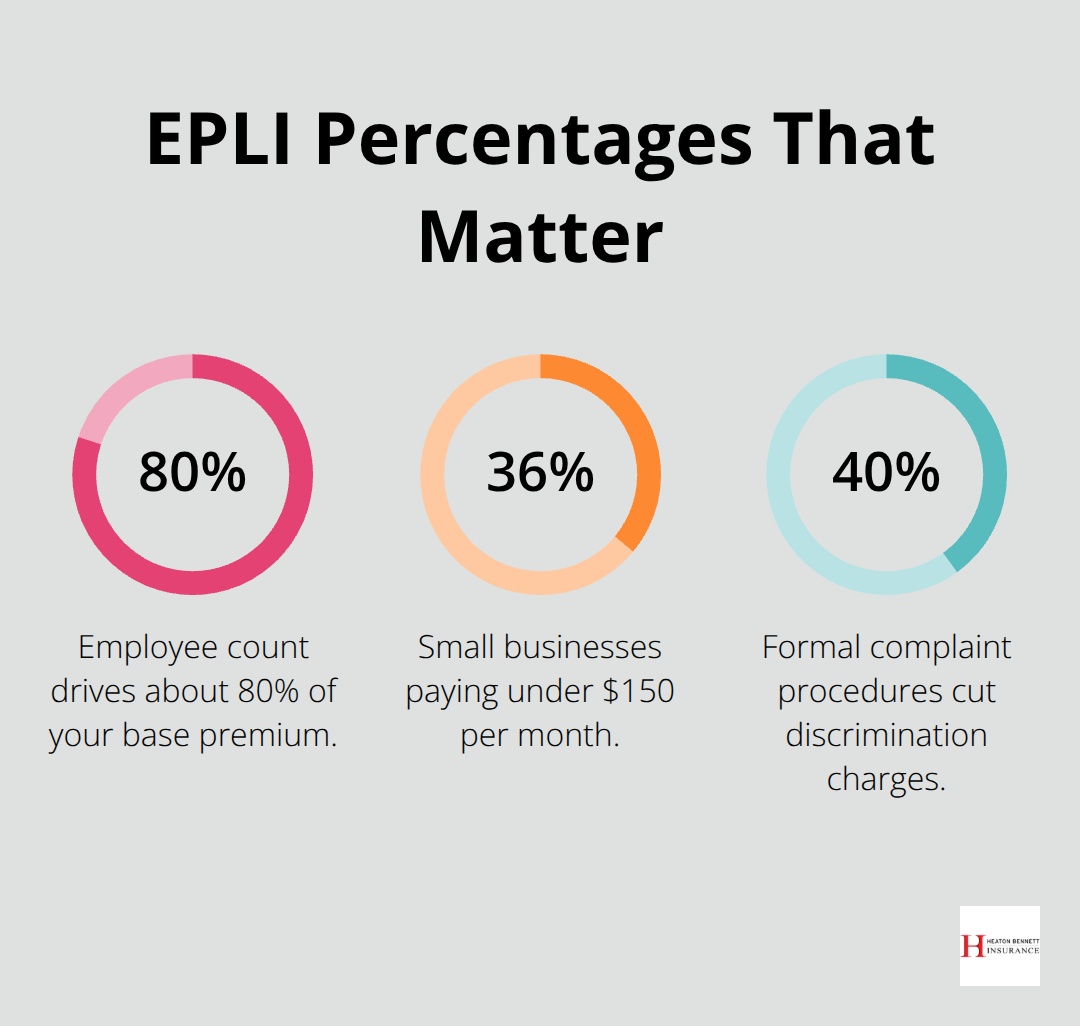

Employee count stands as the single most important factor in your EPLI premium, accounting for roughly 80% of your base cost. A business with 5 to 10 employees typically pays around $1,500 annually, while 50 to 100 employees averages $4,000 to $6,000. This scaling reflects a straightforward reality: more employees create more potential employment disputes. However, raw headcount tells only part of the story.

Industry Type Creates Massive Price Differences

Your industry matters significantly. Healthcare facilities pay roughly $409 per month according to Insureon’s data, while consulting firms average $355 per month and nonprofits just $92 per month. This variation reflects real differences in litigation risk. Healthcare settings face higher exposure to discrimination and harassment claims, while nonprofits operate in lower-risk environments. If you work in healthcare, construction, or manufacturing, you’ll pay substantially more than a nonprofit or professional services firm with identical employee counts.

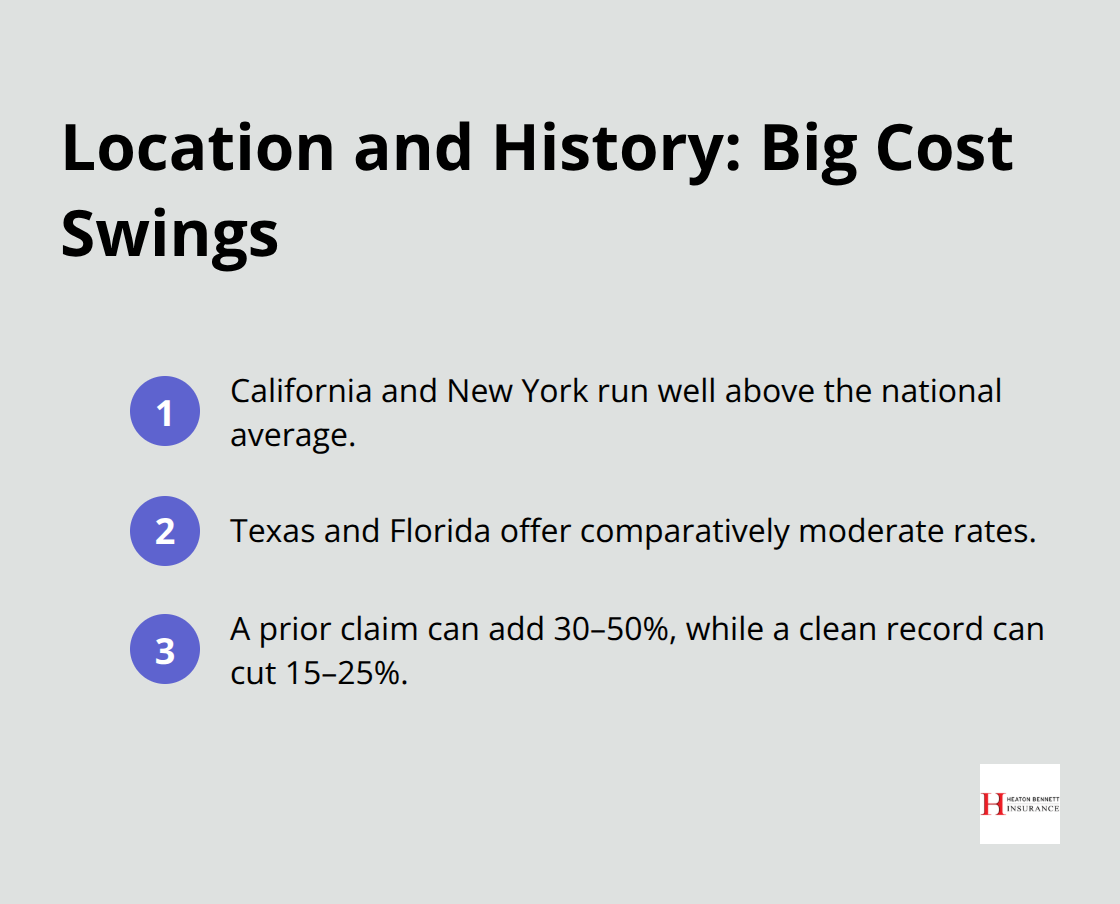

Location and Claims History Reshape Your Bottom Line

Geography is not a minor detail. California premiums run 25 to 40% above the national average due to aggressive employment laws, and New York sits similarly high. Texas and Florida offer comparatively moderate rates. A single past employment claim can increase your premium by 30 to 50%, while a clean claims history can reduce costs by 15 to 25%.

This means your hiring and termination practices directly affect what you pay today and for years to come.

State labor laws amplify this effect: California’s strict rules create higher baseline risk, so insurers charge accordingly. Your revenue size also influences pricing. Firms generating over $5 million annually face base premium increases of 25 to 40% compared with smaller companies at the same headcount.

How Your Hiring Practices Impact Costs

High employee turnover signals risk to insurers because it correlates with wrongful termination and wage disputes. Inconsistent hiring or termination practices push premiums upward, while documented, standardized procedures can lower them. Your business decisions around hiring, firing, and documentation directly shape your insurance costs-and understanding these connections helps you move toward the specific cost breakdowns that apply to your company size.

What You’ll Actually Pay by Company Size

Small Businesses Under 50 Employees

Small businesses with under 50 employees typically pay between $800 and $3,000 annually for EPLI coverage, with most clustering around $1,500 for a 5 to 10 person team. According to Insureon’s data, 36% of small business customers pay less than $150 per month, meaning roughly $1,800 annually. The $10,000 deductible represents the sweet spot for most small operations-high enough to keep premiums manageable but low enough to avoid catastrophic out-of-pocket expenses if a discrimination or wrongful termination claim surfaces.

A healthcare clinic with 8 employees might pay $3,264 annually at $272 per month, while a consulting firm of similar size averages around $2,840 yearly. The real cost driver for small businesses isn’t the per-employee rate; it’s industry risk and your state’s labor laws. A small firm in California faces 25 to 40% higher premiums than an identical business in Texas simply because California’s employment regulations create measurably higher litigation exposure.

Mid-Sized Companies with 50 to 500 Employees

Mid-sized companies operating with 50 to 500 employees see annual EPLI costs ranging from $4,000 to $15,000, with the 50 to 100 employee range averaging $4,000 to $6,000 per year. A consulting firm at 75 employees might pay $5,325 annually, while a healthcare provider at the same size could exceed $8,000. At this scale, your claims history becomes your most powerful cost lever-a single past employment lawsuit can spike your premium by 30 to 50%, while a completely clean record qualifies you for 15 to 25% discounts.

Large Enterprises Over 500 Employees

Large enterprises exceeding 500 employees frequently exceed $15,000 annually, with some paying substantially more depending on revenue and industry. A 500-person manufacturing operation in California could easily surpass $25,000 yearly. For businesses at any scale, annual prepayment saves 5 to 8% compared to monthly installments, and bundling EPLI with general liability or workers’ compensation typically yields 10 to 25% total premium reductions.

How to Control Your Costs Across All Business Sizes

The most expensive mistake mid-sized and large companies make is accepting the first quote without shopping-identical coverage routinely varies by 30 to 40% across carriers, making competitive bidding essential to controlling costs. Your next step involves understanding which specific cost factors apply to your business and how your hiring practices directly influence what you’ll pay.

How to Actually Reduce Your EPLI Premiums

Build Strong Documentation and Processes

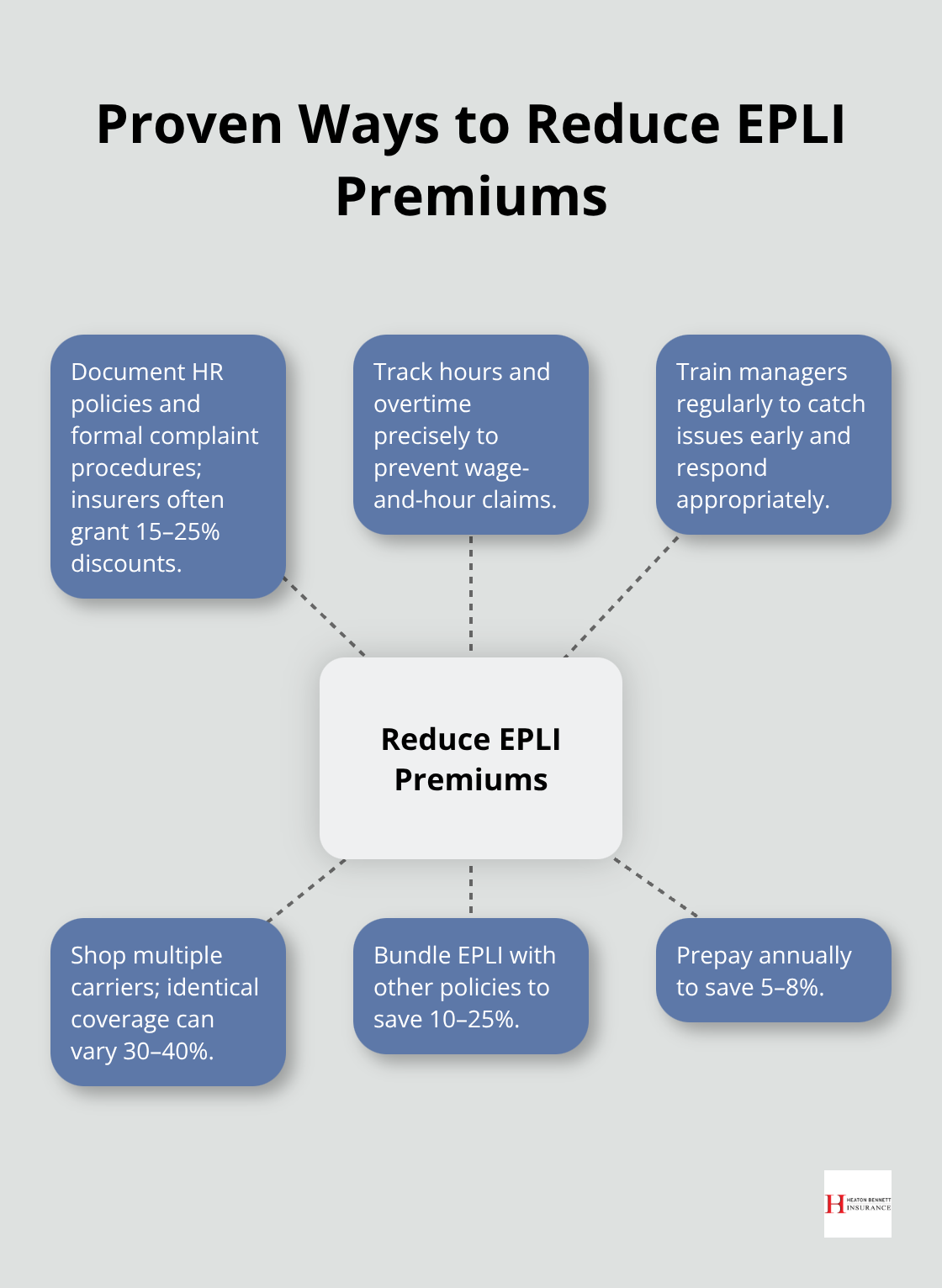

Documentation and consistent processes cut your EPLI costs without cutting coverage. Insurers reduce premiums by 15 to 25% for businesses with written HR policies, formal complaint procedures, and documented disciplinary practices because these elements measurably lower claim frequency. The EEOC reports that formal complaint procedures reduce discrimination charges by roughly 40%, which directly translates to fewer claims and lower premiums. Your hiring manual, termination checklist, and complaint log serve as legal protection and investments that pay back in reduced insurance costs year after year.

A healthcare facility with 20 employees that documents all disciplinary actions, maintains clear anti-harassment policies, and follows progressive discipline before termination pays substantially lower premiums than an identical facility operating without these safeguards. Timeliness matters most: all employee complaints require listening, investigation, decision, and follow-up within a documented timeframe. When complaints drag on unresolved, employees escalate to attorneys, turning a manageable internal dispute into a costly lawsuit.

Control Wage-and-Hour Disputes Through Precise Tracking

Wage-and-hour disputes represent a massive cost driver that documentation controls directly. Paying employees for hours worked, including training time and overtime, eliminates the most common category of EPLI claims. A manufacturing firm that implements precise time-tracking and ensures all overtime receives proper compensation removes one of the largest claim triggers from its risk profile. This single operational change addresses the root cause of preventable claims rather than simply hoping disputes don’t arise.

Invest in Manager Training and Employee Relations

Manager training and employee relations quality matter more than most businesses realize, yet they remain underutilized cost-reduction tools. Insurers increasingly offer preferred rates to companies that conduct regular harassment prevention and management training because trained managers catch problems early and respond appropriately rather than defensively. Your claims history-whether clean or blemished-drives premium variations of 15 to 50%, making every claim prevention effort compound over time. A consulting firm with zero employment-related claims over three years qualifies for discounts that offset training program costs in a single policy year.

Shop Aggressively Across Multiple Carriers

Identical coverage routinely varies by 30 to 40% across carriers, yet most businesses accept their first quote. An independent agent with access to multiple carriers identifies which insurers favor your specific industry and risk profile, often uncovering 20 to 30% savings compared to direct quotes. Bundling EPLI with general liability, workers’ compensation, or commercial property policies yields 10 to 25% total premium reductions because insurers reward consolidated relationships.

Optimize Your Payment Structure

Paying your annual premium upfront rather than monthly saves 5 to 8%, a straightforward reduction that requires no operational changes. This simple adjustment compounds with other cost-reduction strategies to create meaningful savings across your policy term.

Final Thoughts

Your EPLI insurance cost reflects both factors outside your control and decisions you make every day. Employee count, industry type, location, and claims history establish your baseline premium, while your hiring practices, documentation standards, and manager training directly shape what you actually pay. A business that maintains strong HR policies, tracks wages precisely, and handles complaints formally pays measurably less than a competitor of identical size operating without these safeguards.

Shopping across multiple carriers and bundling coverage with other business policies typically saves 10 to 40% compared to accepting a single quote. Your deductible, policy limits, and specific exclusions matter as much as your premium because they determine what you recover when a discrimination, harassment, or wrongful termination claim surfaces. Most businesses discover they’ve either over-insured or under-insured only after a claim hits, making the coverage decision critical before problems arise.

We at Heaton Bennett Insurance help you navigate EPLI options and identify coverage that matches your specific industry, employee count, and risk profile. Our team works with multiple carriers to find the right balance between protection and affordability, and we handle the competitive shopping that typically saves our clients thousands annually. Contact our Austin-based team at Heaton Bennett Insurance to discuss your EPLI insurance cost and get a personalized quote today.

![Vacation Rental Insurance for Owners [2025 Guide]](https://insureaustin.com/wp-content/uploads/emplibot/Vacation-Rental-Insurance-for-Owners-_2025-Guide__1766711421-80x80.jpeg)