What is the Average Cost of EPLI Insurance?

Employment Practices Liability Insurance protects businesses from costly lawsuits related to workplace discrimination, harassment, and wrongful termination. EPLI insurance cost varies significantly based on company size, industry, and location.

We at Heaton Bennett Insurance see businesses paying anywhere from $500 annually for small companies to over $15,000 for larger organizations. Understanding these pricing factors helps you budget effectively for this essential coverage.

How Much Does EPLI Insurance Actually Cost?

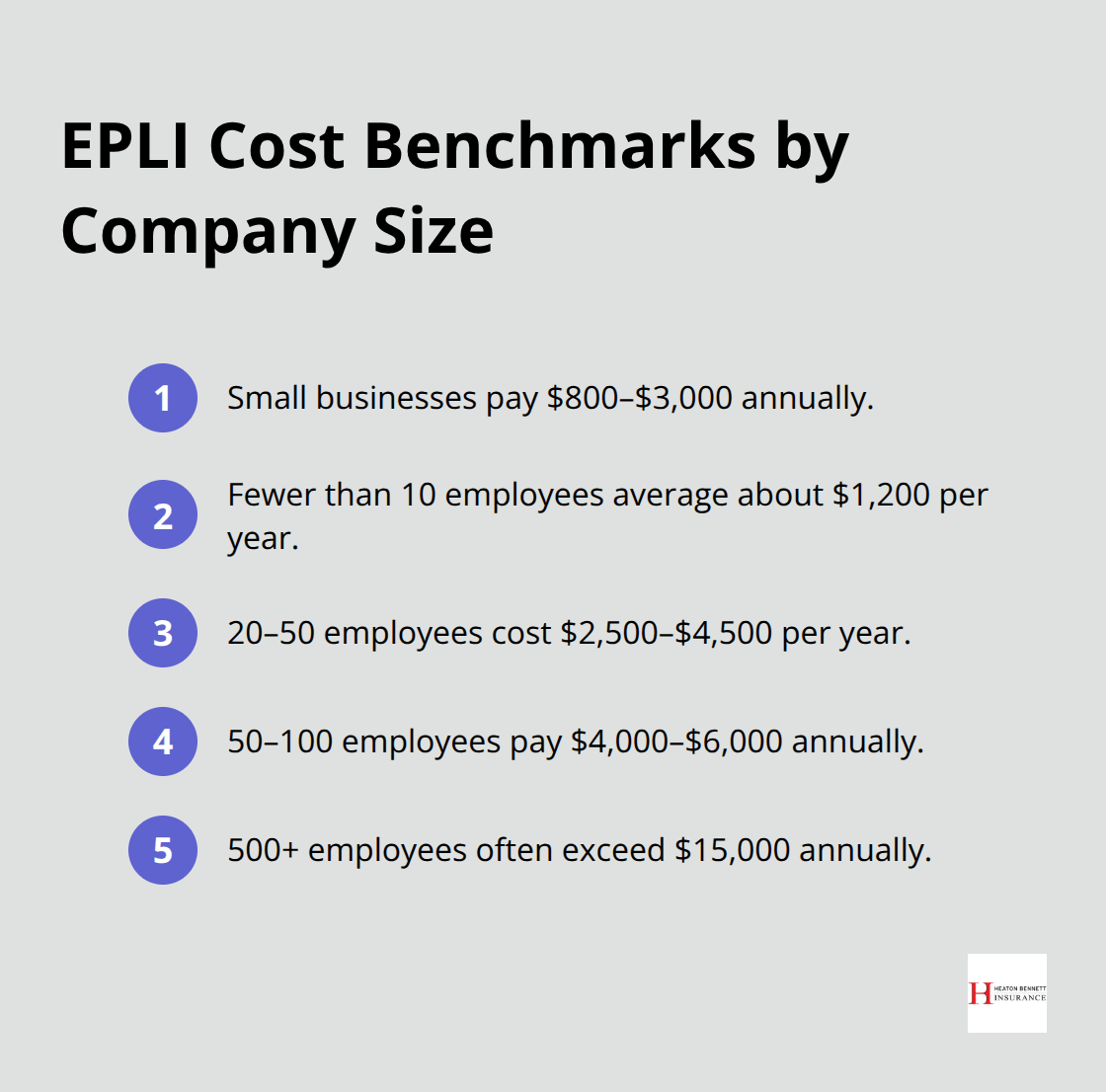

Small businesses typically pay between $800 and $3,000 annually for EPLI coverage, with the national average at $2,665 per year according to recent industry data. Companies with fewer than 10 employees often see premiums around $1,200 annually, while businesses with 20-50 employees face costs from $2,500 to $4,500. The calculation breaks down to approximately $50-150 per employee annually, though this varies dramatically based on your specific risk profile.

Premium Costs Scale With Employee Count

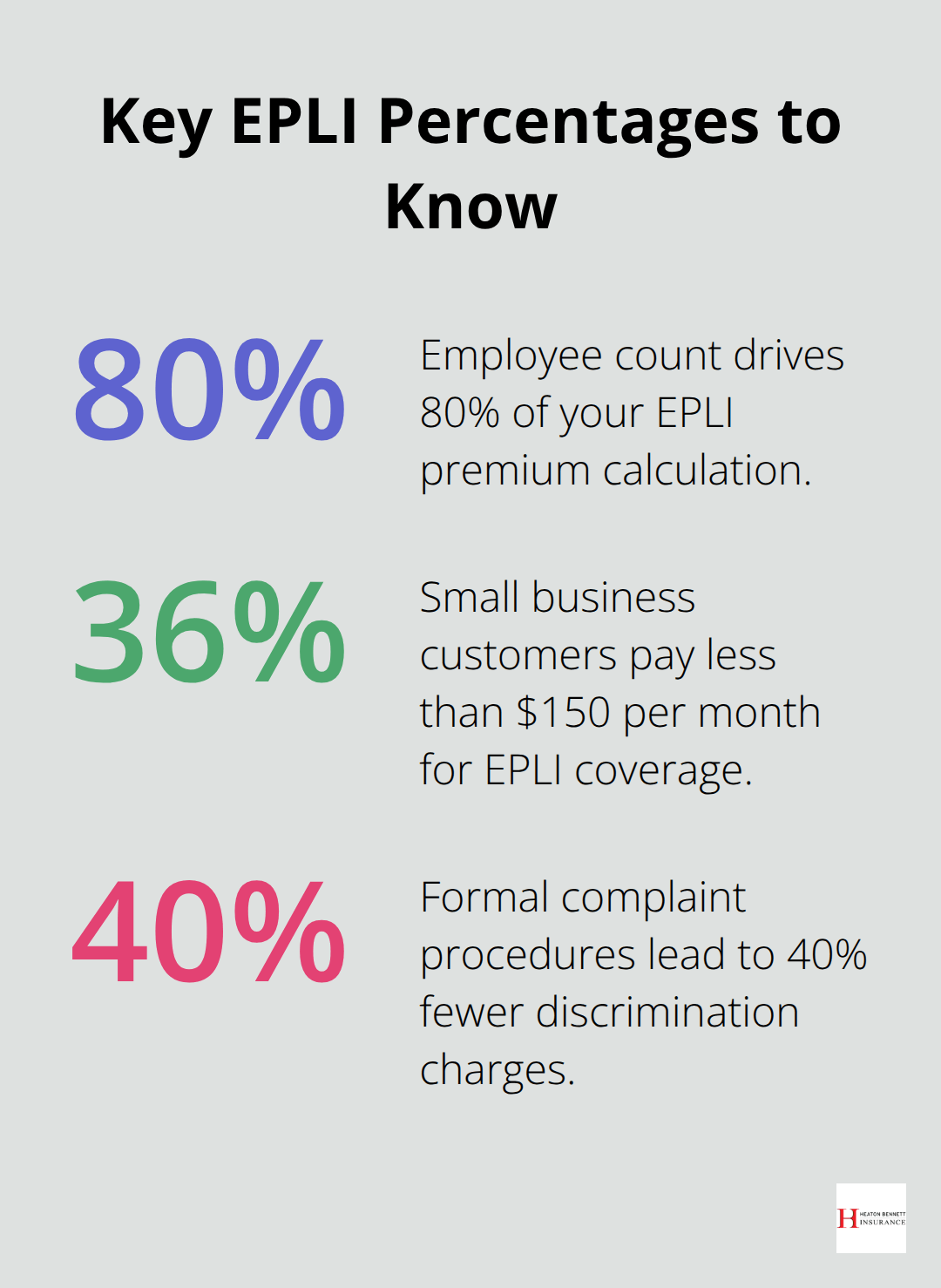

The number of employees drives 80% of your EPLI premium calculation. Businesses with 5-10 employees average $1,500 annually, while companies that employ 50-100 workers typically pay $4,000-6,000. Large organizations with 500+ employees often face premiums that exceed $15,000 annually. Healthcare companies pay the highest rates at $409 monthly on average, while firms in the consulting industry average $355 monthly. Nonprofits benefit from significantly lower premiums at just $92 monthly, which reflects their reduced litigation risk.

Geographic Location Creates Major Price Differences

California and New York command the highest EPLI premiums due to extensive labor laws and litigious environments. California businesses pay 25-40% more than the national average, while companies in states like Texas and Florida see more moderate rates. The average deductible selection stands at $10,000, though higher deductibles can reduce premiums by 15-20%. Coverage limits typically range from $100,000 to $1,000,000, with most businesses that select $500,000-1,000,000 in protection.

Monthly Payment Options Affect Total Costs

Most insurers offer monthly payment plans (though annual payments often provide discounts of 5-8%). Small businesses frequently choose monthly payments to manage cash flow, despite the slightly higher total cost. The monthly breakdown shows 36% of small business customers pay less than $150 per month for EPLI coverage, which translates to under $1,800 annually.

These baseline costs represent just the starting point for your EPLI investment. Several key factors can dramatically increase or decrease these premiums based on your company’s specific risk profile and operational characteristics.

What Drives Your EPLI Premium Higher or Lower

Industry Risk Classifications Shape Base Rates

Your industry classification determines the baseline risk assessment that insurers use to calculate premiums. Healthcare companies face the steepest rates at $409 monthly because patient interactions and high-stress environments generate more harassment and discrimination claims. Consulting firms average $355 monthly due to frequent client interactions and project-based hiring patterns that increase wrongful termination risks.

Manufacturing and construction companies pay elevated premiums because physical work environments create more opportunities for workplace disputes. Nonprofits enjoy the lowest rates at $92 monthly since their mission-driven culture and volunteer workforce reduce litigation frequency.

Claims History Directly Impacts Premium Calculations

Your claims history over the past three years directly impacts pricing. Companies that have filed previous EPLI claims face premium increases of 30-50%. Clean claims records often qualify for preferred rates that can reduce costs by 15-25%. Insurers view past claims as strong predictors of future risk exposure.

Revenue Size Creates Premium Multipliers

Annual revenue acts as a premium multiplier because higher-earning companies face larger settlement demands and jury awards. Businesses that generate over $5 million annually typically see base premiums increase by 25-40% compared to smaller companies with identical employee counts. This revenue factor explains why two companies with 20 employees can have drastically different EPLI costs.

Employee turnover rates above 20% annually signal higher risk to insurers and result in premium surcharges of 10-20%. Companies that demonstrate stable workforce management through documented retention strategies often qualify for preferred pricing tiers.

Coverage Limits and Deductibles Control Final Costs

Policy limits between $500,000 and $1,000,000 represent the sweet spot for most businesses, with coverage above $1,000,000 adding 40-60% to base premiums. Higher deductibles (from $2,500 to $25,000) can reduce annual premiums by 20-35%, though this increases your out-of-pocket exposure for smaller claims.

The median settlement value for EPL claims reaches $90,000 according to Jury Verdict Research, while court cases average $217,000 in damages. These figures help determine appropriate coverage limits that balance premium costs with adequate protection.

Smart businesses look beyond these baseline factors to find practical ways to reduce their EPLI costs through strategic risk management and policy decisions.

How Can You Cut EPLI Costs Without Sacrificing Protection

Strong HR Policies Deliver Immediate Premium Reductions

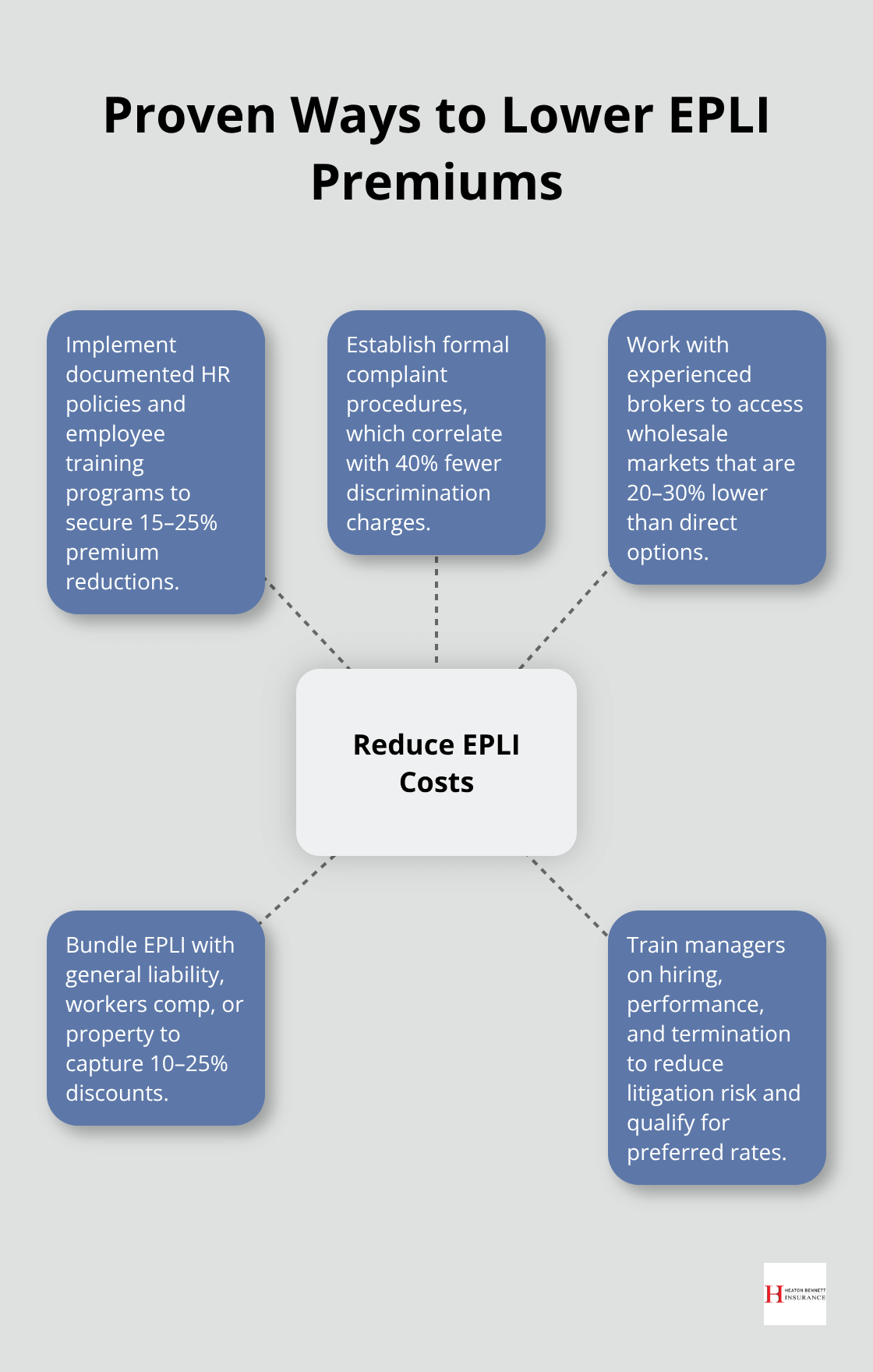

Companies that maintain documented HR policies and comprehensive employee training programs see EPLI premiums drop by 15-25% according to insurance underwriters. Businesses that implement harassment prevention training, maintain clear disciplinary procedures, and document all employee interactions show proactive risk management to insurers.

The Equal Employment Opportunity Commission reports that businesses with formal complaint procedures face 40% fewer discrimination charges. Written employee handbooks, regular performance reviews, and exit interview documentation create paper trails that protect against wrongful termination claims (while demonstrating organized management practices to underwriters).

Manager Training Reduces Litigation Risk

Training managers on proper hiring practices, performance management, and termination procedures significantly reduces litigation risk. Companies that invest in supervisor education programs demonstrate commitment to compliance and often qualify for preferred insurance rates. Regular training updates keep management current on employment law changes and best practices.

Professional Brokers Access Better Markets

Experienced insurance brokers access wholesale markets that offer 20-30% lower premiums than direct-to-consumer policies. Brokers leverage relationships with multiple carriers to compare coverage options and negotiate better terms. Independent agents provide access to carriers that offer specialized EPLI products for specific industries.

Professional brokers also identify coverage gaps and recommend appropriate limits based on actual risk exposure rather than generic industry standards. They understand which carriers offer the most competitive rates for different business profiles (and can often secure coverage that individual businesses cannot access directly).

Strategic Policy Bundling Creates Immediate Savings

Companies that bundle EPLI with general liability, workers compensation, or commercial property insurance generate discounts of 10-25% on total premiums. Business Owner Policies that include EPLI coverage often cost less than standalone policies. Multi-policy discounts increase with additional coverage types.

Carriers prefer bundled accounts because they reduce administrative costs and increase customer retention. These savings get passed to policyholders through lower premiums, making comprehensive business insurance packages more cost-effective than individual policies.

Final Thoughts

EPLI insurance cost spans from $800 annually for small businesses to over $15,000 for large organizations, with most companies that pay $2,665 per year on average. Your final premium depends on employee count, industry risk, claims history, and geographic location. Healthcare companies face the highest rates at $409 monthly, while nonprofits benefit from lower premiums at $92 monthly.

Multiple carrier quotes provide the most effective way to secure competitive rates. Premium differences between insurers can reach 30-40% for identical coverage, which makes thorough market comparison essential. Independent agents access wholesale markets that often provide better rates than direct-to-consumer policies.

We at Heaton Bennett Insurance help businesses navigate these complex factors through comprehensive market access and coverage analysis. Our independent agency approach connects you with multiple carriers to find optimal EPLI protection at competitive rates. Contact us today to receive customized quotes that match your specific risk profile and budget requirements.