![Annuities Explained The Ultimate Guide for Retirees [2025]](https://insureaustin.com/wp-content/uploads/emplibot/Annuities-Explained-The-Ultimate-Guide-for-Retirees-_2025__1760663225-1030x589.jpeg)

Annuities Explained The Ultimate Guide for Retirees [2025]

Retirement planning becomes more complex when you need guaranteed income that lasts your entire lifetime. Traditional savings accounts and investment portfolios can’t promise the security that many retirees desperately need.

We at Heaton Bennett Insurance believe understanding annuity basics is the first step toward building a rock-solid retirement income strategy. This comprehensive guide breaks down everything you need to know about annuities in 2025.

How Do Annuities Actually Work

An annuity creates a contract between you and an insurance company where you pay a lump sum or series of payments in exchange for guaranteed income payments later. The insurance company invests your money and promises to pay you back with interest according to your contract terms. This arrangement produces a predictable income stream that can last for a specific period or your entire lifetime.

The Three Main Annuity Categories

Fixed annuities guarantee a specific interest rate, typically from 2% to 4% annually in 2025. Your principal stays protected, and you know exactly how much income you’ll receive each month. Variable annuities tie your returns to market performance through investment subaccounts, which offer higher growth potential but provide no guarantees on returns.

Fixed indexed annuities link returns to market indexes like the S&P 500 while they protect your principal from losses. According to LIMRA, nearly 70% of annuity buyers prioritize lifetime income guarantees over growth potential when they make their purchase decisions.

Payment Calculation Methods

Insurance companies calculate your payments based on your age, gender, current interest rates, and your chosen payout option. A 65-year-old man who invests $100,000 in an immediate annuity might receive approximately $500-600 monthly for life in today’s interest rate environment. Women typically receive slightly lower payments due to longer life expectancy statistics.

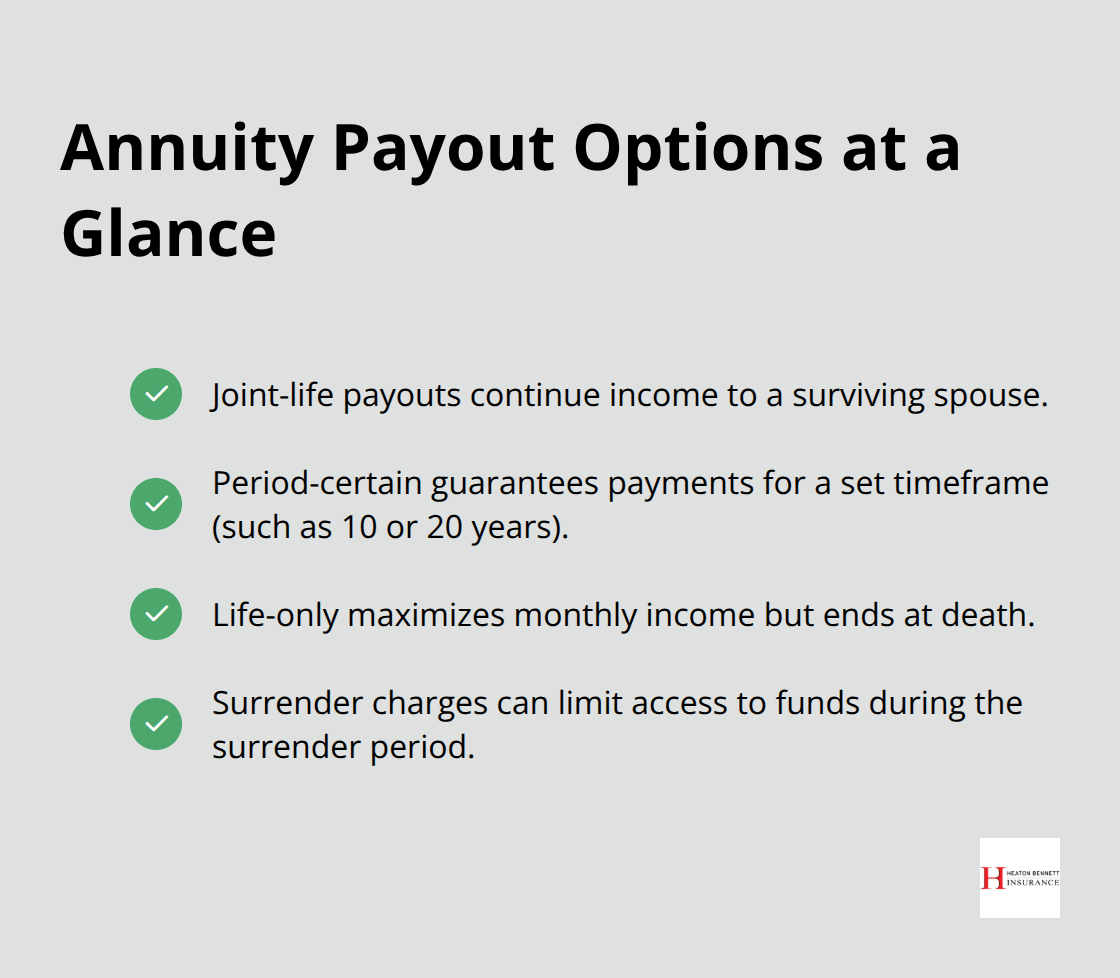

Distribution Options Available

You can choose joint-life payouts that continue payments to your spouse after your death, or select period-certain options that guarantee payments for a specific timeframe (such as 10 or 20 years). Life-only payments maximize your monthly income but stop completely at death, which makes them suitable for single retirees without heirs to consider.

Surrender charges typically range from 5% to 10% in the first year and decline annually until they disappear after 7-10 years. These fees protect insurance companies from early withdrawals that could disrupt their investment strategies, but they also limit your access to funds during the surrender period.

Now that you understand how annuities function mechanically, you need to weigh their specific advantages against potential drawbacks for your retirement strategy.

Should You Buy an Annuity for Retirement

Annuities deliver the strongest advantage that most retirement products cannot match: guaranteed lifetime income that eliminates the fear of outliving your money. The Employee Benefit Research Institute found that retirees with annuities report significantly higher levels of financial security compared to those who rely solely on traditional investment portfolios.

Fixed annuities currently offer guaranteed returns of 2% to 4% annually, which beats savings account rates while they protect your principal from market crashes. Variable annuities provide tax-deferred growth that compounds without annual tax consequences until withdrawal, which allows your retirement funds to grow faster than taxable investments.

The Income Security Advantage

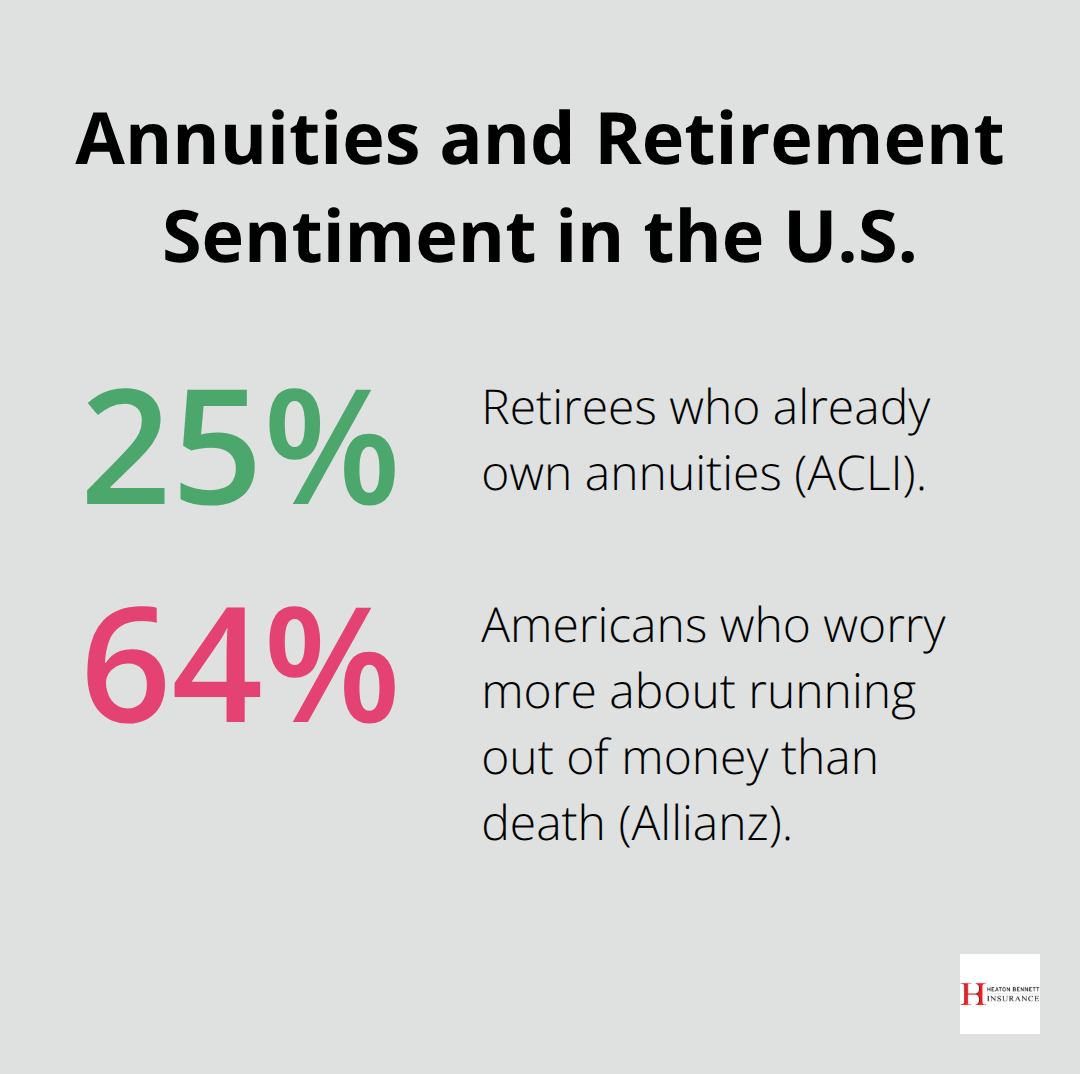

According to the American Council of Life Insurers, 25% of retirees already own annuities, and this percentage continues to climb as people recognize their income stability benefits. Nearly 64% of Americans worry more about running out of money in retirement than about death (according to Allianz research), which makes the guaranteed income feature particularly valuable.

Variable annuities allow you to participate in market gains while they provide a safety net through minimum income guarantees. This combination appeals to retirees who want growth potential without complete market exposure.

The Hidden Cost Problem

Annuities carry substantial fees that can destroy your returns over time. Variable annuities typically charge 2% to 3% in annual fees, which include management expenses, mortality charges, and administrative costs. These fees compound annually and can reduce your account value by 30% to 40% over a 20-year retirement period.

Surrender charges present another major liquidity concern, as they range from 5% to 10% in early years and last up to a decade. Most annuities only allow 10% annual withdrawals without penalties, which severely limits access to your own money during emergencies.

Tax Implications You Must Consider

Non-qualified annuities offer tax deferral but create ordinary income tax rates on all growth when withdrawn, even if the underlying investments would qualify for capital gains treatment. This tax treatment can cost high earners an additional 15% to 20% compared to direct investment taxation.

Qualified annuities funded with IRA or 401k money provide no additional tax benefits since those accounts already grow tax-deferred. The Tax Cuts and Jobs Act maintains these tax structures through 2025, which makes current annuity tax planning strategies reliable for near-term retirement decisions.

When Market Conditions Matter

The current interest rate environment influences annuity returns significantly, with higher rates providing a larger safety cushion for insurance companies. Low interest rates may force insurers to take on more risk to achieve adequate returns, which impacts the safety margin of annuities.

Inflation presents a long-term threat to annuity safety, as fixed payments can lose purchasing power over time. Annuities with inflation protection or cost-of-living adjustments may provide better long-term value, even if they start with lower initial payments.

These factors make the selection process more complex than simply choosing between annuity types, which leads us to examine the specific criteria you should evaluate when choosing the right annuity for your situation.

How Do You Choose the Right Annuity

Your financial advisor’s credentials matter more than their sales pitch when you select annuities. Work only with advisors who hold proper insurance licenses and can demonstrate experience with multiple annuity providers. The National Association of Insurance Commissioners reports that consumers who compare offers from at least three different insurers secure better terms and lower fees. Request specific fee breakdowns in written form, which should include surrender charges, annual management fees, and any rider costs before you make decisions.

Financial Strength Ratings Determine Safety

Insurance company ratings from AM Best, Moody’s, and Standard & Poor’s directly impact your annuity’s safety over decades. Never purchase from companies rated below A- by AM Best, as lower-rated insurers face higher bankruptcy risks that could jeopardize your retirement income. State guarantee associations provide limited protection (typically capping coverage at $250,000 to $300,000 per person per company). You can reduce concentration risk while you maintain maximum protection when you spread large investments across multiple highly-rated insurers. Verify current ratings before you finalize any annuity purchase, as ratings can change based on market conditions.

Questions That Reveal Hidden Costs

Ask your provider to explain all fees in plain language, not industry jargon. Variable annuities often hide mortality and expense charges that exceed 1.5% annually on top of management fees. Request a complete illustration that shows how fees will impact your account value over 10, 15, and 20 years. Many providers quote attractive teaser rates that reset to lower levels after the first year, so demand details about rate guarantees and renewal terms.

Avoid These Purchase Mistakes

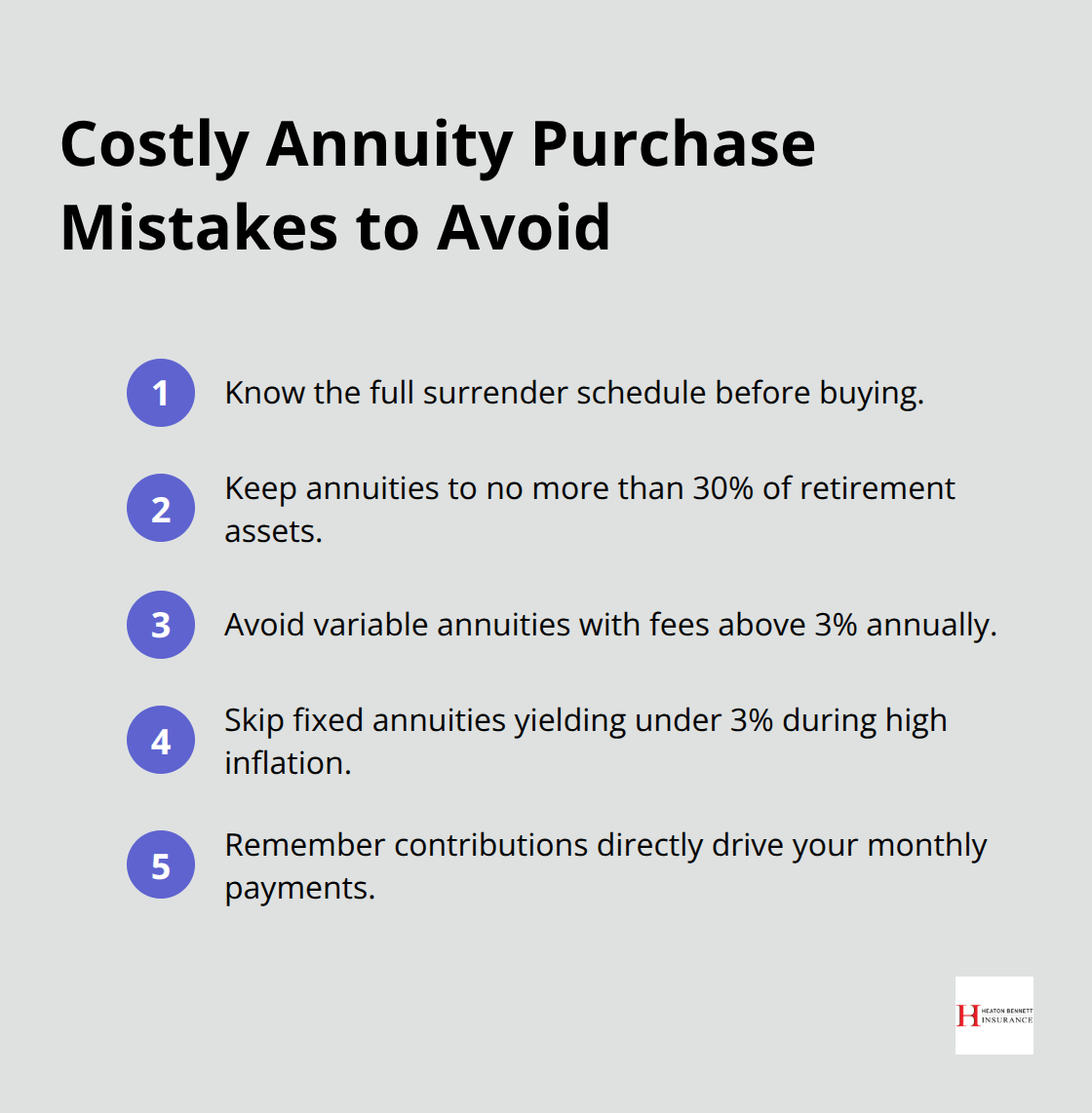

The biggest mistake retirees make involves purchasing annuities without they understand surrender periods and withdrawal restrictions. Most contracts lock your money for 7-10 years with penalties that range from 5% to 10% for early access. Calculate your emergency fund needs before you commit, as annuities should represent no more than 30% of your total retirement assets.

High-fee variable annuities destroy wealth through annual charges that exceed 3%, which compound over time and reduce your account value significantly. Fixed annuities currently offering rates below 3% fail to keep pace with inflation and should be avoided in favor of higher-yielding alternatives (especially when inflation runs above 3% annually). Remember that how much you contribute directly determines your monthly payments from the insurance company.

Final Thoughts

Annuity basics show these products work best for retirees who value guaranteed income over maximum growth potential. The 64% of Americans who fear they will outlive their money more than death find real value in lifetime income guarantees that annuities provide. Fixed annuities currently offer 3% to 4% guaranteed returns that beat savings accounts while they protect principal from market volatility.

Variable annuities suit retirees who feel comfortable with market exposure and want tax-deferred growth combined with income guarantees. However, their 2% to 3% annual fees can reduce long-term returns significantly. You should avoid annuities if you need frequent access to your money or cannot afford to lock funds away for 7-10 years due to surrender charges (especially if high-fee products exceed 3% annually).

Start your annuity research when you compare offers from at least three A-rated insurance companies. Focus on companies that AM Best rates A- or higher to protect against insurer bankruptcy risks. We at Heaton Bennett Insurance help Austin residents navigate complex insurance decisions through our independent agency that provides access to multiple carriers.