How to Get Renters Insurance for Commercial Property

Renting commercial property comes with unique risks that require specialized insurance coverage. At Heaton Bennett Insurance, we understand the importance of protecting your business assets and operations.

Renters insurance for commercial property offers essential protection for businesses that don’t own their premises. This guide will walk you through the process of obtaining the right coverage to safeguard your company’s future.

What Is Commercial Renters Insurance?

Definition and Scope

Commercial renters insurance protects businesses operating in leased spaces. This specialized coverage addresses the unique risks faced by companies in rented commercial properties. Unlike residential renters insurance, which focuses on personal belongings, commercial policies encompass a broader range of protections for business assets and operations.

Key Differences from Residential Coverage

The scope of commercial renters insurance extends far beyond its residential counterpart. While residential policies typically cover personal property and liability, commercial policies include:

- Business equipment protection

- Inventory coverage

- Potential income loss compensation

For instance, if a fire damages your rented office space, a commercial policy could cover not only the damaged equipment but also the income lost while your business cannot operate.

Who Needs This Coverage?

Almost any business renting a commercial space should consider this insurance. This includes:

- Retail stores

- Restaurants

- Professional services firms

- Home-based businesses that see clients in rented spaces

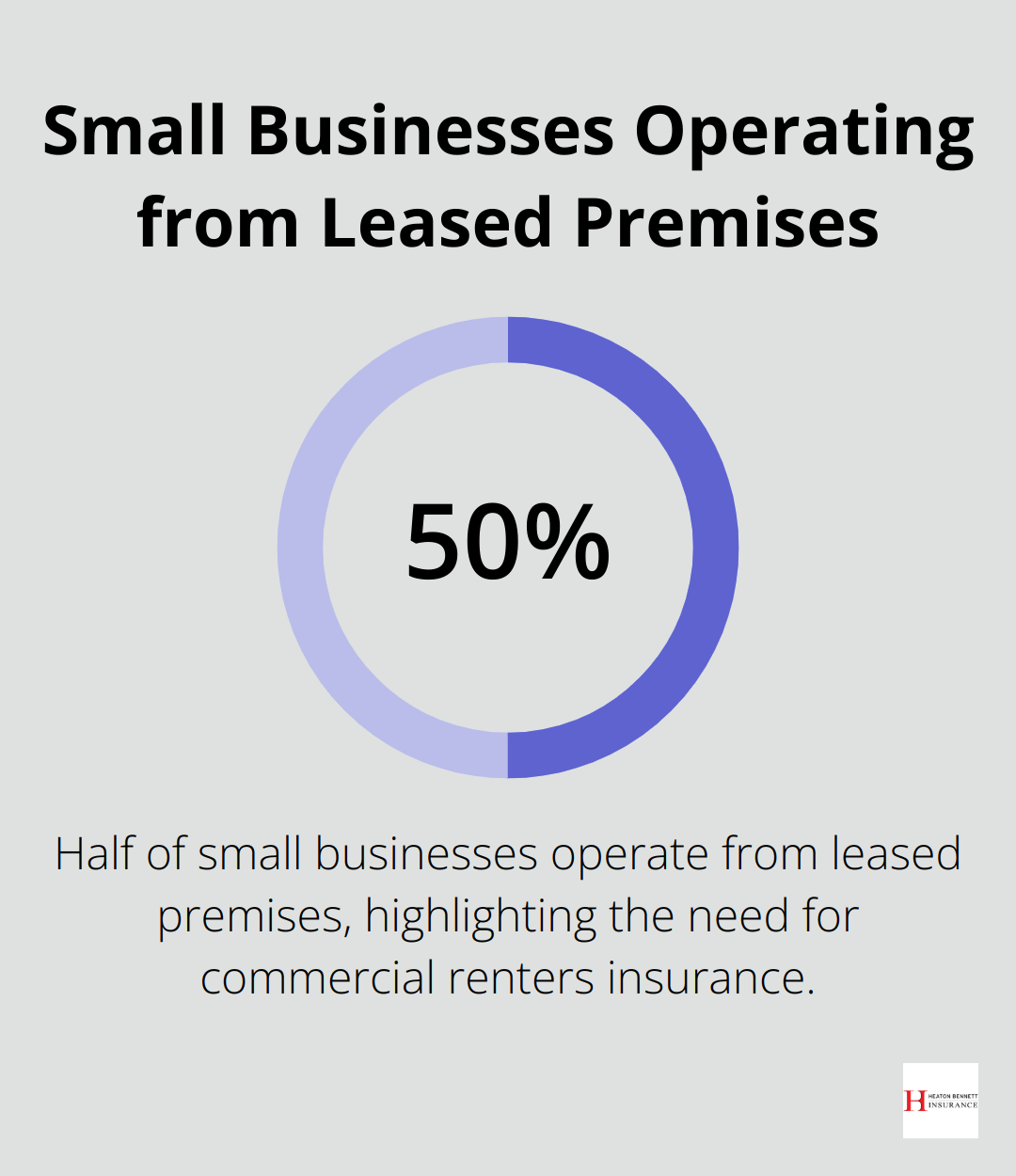

The Small Business Administration reports that approximately 50% of small businesses operate from leased premises, underscoring the widespread need for this coverage.

Tailoring Coverage to Your Business

Different businesses require varying levels of coverage. A restaurant might need higher liability limits due to the risk of food-related illnesses, while a consulting firm might prioritize coverage for expensive computer equipment.

The Cost of Operating Without Insurance

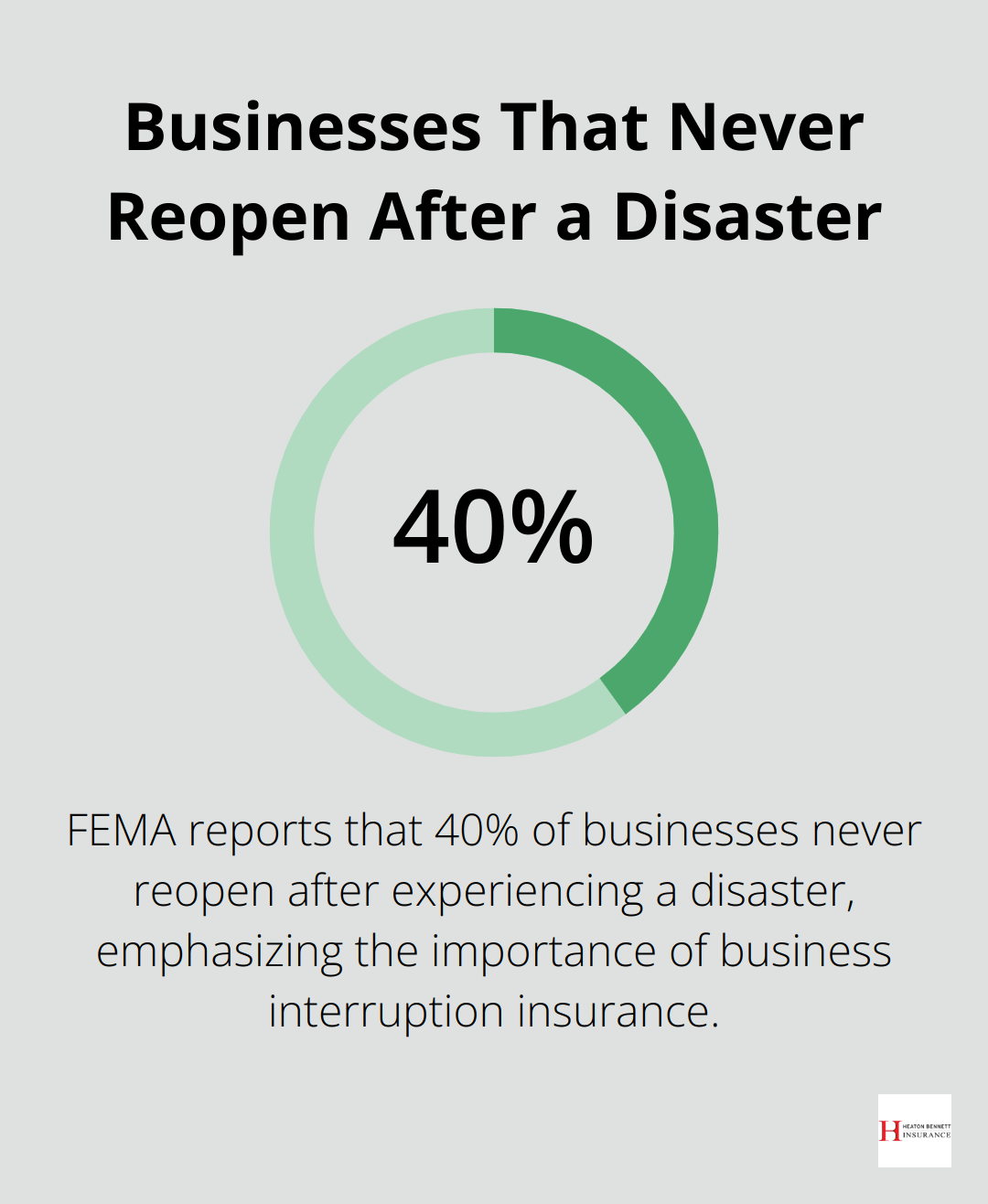

The financial implications of operating without proper insurance can be severe. The Insurance Information Institute reports that 40% of small businesses never reopen after a disaster. Proper commercial renters insurance can help your business avoid becoming part of this statistic.

It’s important to note that your landlord’s insurance typically doesn’t cover your business assets or liability. The responsibility for protecting your business operations and property falls on you. Securing comprehensive commercial renters insurance isn’t just about fulfilling a potential lease requirement – it’s an investment in your business’s longevity and resilience.

As we move forward, let’s explore the specific types of coverage provided by commercial renters insurance and how they can safeguard your business against various risks.

What Does Commercial Renters Insurance Cover?

Commercial renters insurance provides a comprehensive shield for businesses operating in leased spaces. This insurance type safeguards business assets, protects against liability claims, and helps maintain operations during unforeseen disruptions.

Property Protection: A Shield for Business Assets

Property protection forms the foundation of commercial renters insurance. This coverage extends to business equipment, inventory, and furnishings. The Insurance Information Institute reports that 75% of businesses are underinsured, which leaves them vulnerable to significant losses. A robust policy ensures that assets receive full protection against risks such as fire, theft, and vandalism.

For example, if a burst pipe damages expensive computer equipment, the policy would cover the replacement costs. This protection proves vital, as the National Fire Protection Association reports that U.S. fire departments respond to an average of 3,340 office property fires each year.

Liability Coverage: Legal Protection for Businesses

Liability coverage constitutes another essential component of commercial renters insurance. This protects businesses if a client or visitor sustains an injury on the premises. The U.S. Bureau of Labor Statistics reports that slips, trips, and falls account for 27% of nonfatal occupational injuries. A comprehensive policy covers medical expenses and potential legal costs if someone sues the business for such an incident.

Business Interruption Insurance: Continuity in Crisis

Business interruption insurance often flies under the radar but can serve as a lifesaver. If a covered event forces a business to temporarily close, this coverage helps replace lost income and covers ongoing expenses (like rent and payroll). The Federal Emergency Management Agency (FEMA) states that 40% of businesses never reopen after a disaster. With proper coverage, a business can weather such storms and emerge stronger.

Tailored Coverage Options: Meeting Unique Needs

Every business faces unique risks, and insurance should reflect that reality. Additional coverage options address specific needs. These might include data breach protection, equipment breakdown coverage, or professional liability insurance for service-based businesses.

A restaurant, for instance, might benefit from food spoilage coverage, while a consulting firm might need professional liability insurance to protect against claims of negligence or errors in professional services.

The right coverage can mean the difference between a minor setback and a major financial disaster for a business. As we move forward, we’ll explore the steps to obtain the most suitable commercial renters insurance for your specific business needs.

How to Secure the Right Commercial Renters Insurance

Evaluate Your Business Risks

The first step to obtain appropriate coverage is a thorough risk assessment. This involves the identification of potential threats to your business operations, assets, and liability exposure. The Insurance Information Institute reports that 75% of businesses are underinsured, often due to inadequate risk evaluation.

Start by creating a catalog of your business assets, including equipment, inventory, and furnishings. Consider your business operations next. A restaurant faces different risks than a consulting firm. The National Restaurant Association states that 60% of restaurants fail within the first three years (often due to inadequate insurance coverage).

Navigate the Insurance Marketplace

After you assess your risks, explore insurance options. The insurance marketplace can be complex, with numerous providers offering varying levels of coverage. The National Association of Insurance Commissioners (NAIC) recommends you obtain quotes from at least three different insurers to ensure competitive pricing and comprehensive coverage.

When you research providers, look beyond just price. Consider factors such as financial stability, customer service ratings, and claim processing efficiency. A.M. Best, a credit rating agency focused on the insurance industry, provides financial strength ratings for insurers that can guide your decision.

Decode Policy Terms and Coverage Limits

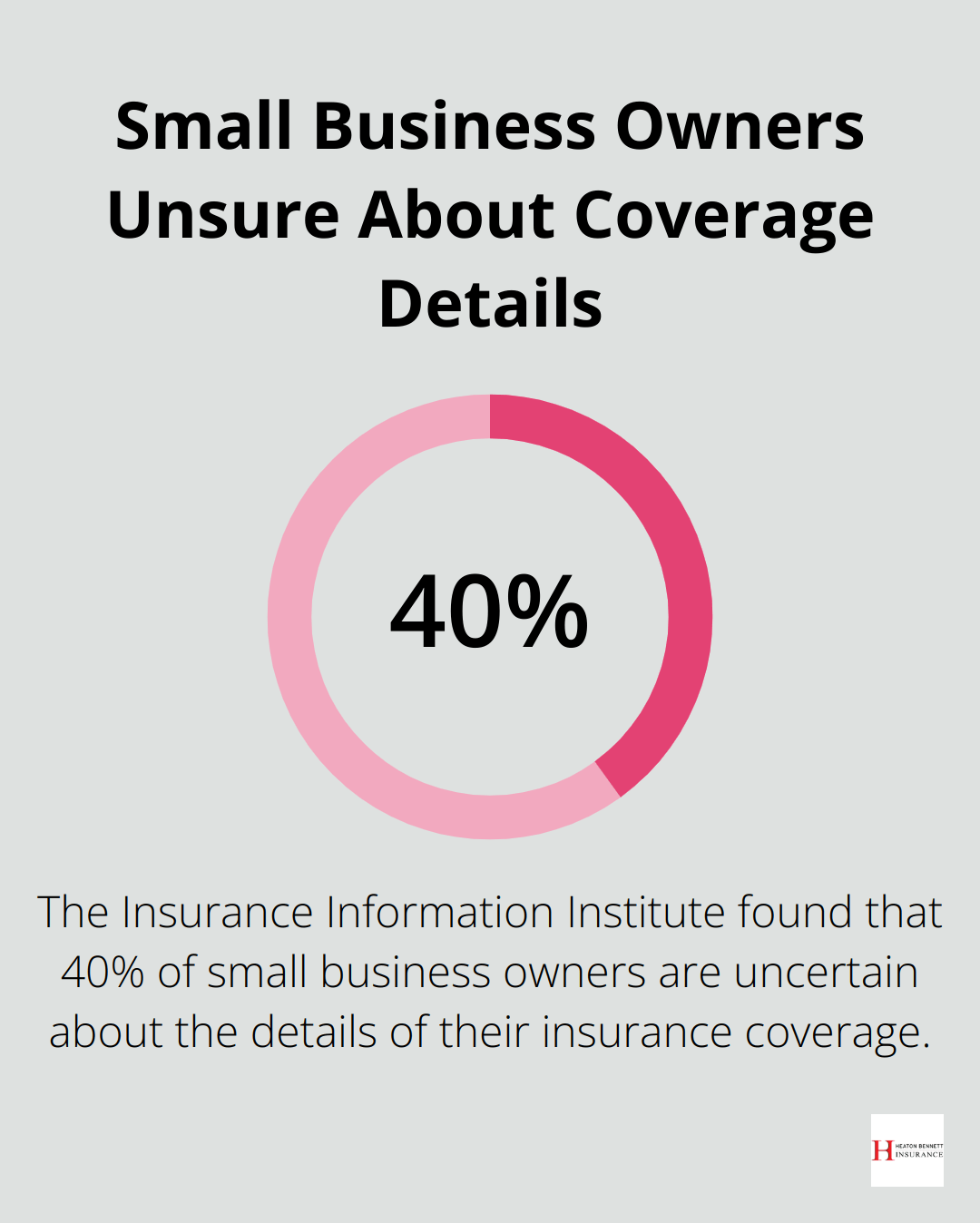

Insurance policies often contain complex language and terms. It’s important to understand what’s covered, what’s excluded, and the limits of your coverage. The Insurance Information Institute found that 40% of small business owners are unsure about their coverage details.

Pay close attention to coverage limits. These should align with the value of your business assets and potential liability risks. For instance, if you have $500,000 worth of equipment but only $250,000 in property coverage, you’re significantly underinsured.

Also, consider your deductible. A higher deductible can lower your premiums, but ensure it’s an amount your business can comfortably pay if you need to file a claim.

Work with Experienced Professionals

The goal isn’t just to get insurance-it’s to secure the right coverage that provides peace of mind and financial protection for your business. Work with experienced professionals who can guide you through the complexities of commercial renters insurance.

At Heaton Bennett Insurance, we use our “Security Snapshot” process to help businesses navigate these complexities. This approach ensures that you understand your policy details and that your coverage aligns perfectly with your business needs.

Review and Update Regularly

Your business needs may change over time. Try to review your commercial renters insurance policy annually (or whenever significant changes occur in your business). This practice helps ensure your coverage remains adequate and relevant to your current business situation.

Final Thoughts

Commercial renters insurance protects businesses in leased spaces from property damage, liability claims, and interruptions. We at Heaton Bennett Insurance understand the complexities of renters insurance for commercial property. Our team uses a unique “Security Snapshot” process to guide businesses through insurance selection, identifying risks and evaluating coverage needs.

We offer flexible solutions that adapt to the unique requirements of each business, with access to a wide range of insurance products and carriers. Our approach provides peace of mind by ensuring businesses have comprehensive coverage tailored to their specific needs. We don’t just sell insurance; we help safeguard your business’s future.

Don’t leave your business vulnerable to potential risks. Take the first step towards comprehensive protection by visiting our website to learn more about how Heaton Bennett Insurance can help protect your business. Securing the right commercial renters insurance allows you to focus on what matters most – running and growing your business.