Understanding Different Types of Property Insurance Coverage

Property insurance coverage types can be complex, but understanding them is essential for protecting your assets.

At Heaton Bennett Insurance, we’ve seen firsthand how the right coverage can make all the difference when unexpected events occur.

This guide will break down the key components of homeowners, renters, and commercial property insurance, helping you make informed decisions about your coverage needs.

What Does Homeowners Insurance Cover?

Homeowners insurance serves as a vital shield for your most valuable asset. This type of coverage protects your home’s structure, personal belongings, and provides liability protection. Let’s examine these key components to give you a clear picture of what you’re getting.

Protection for Your Home’s Structure

The foundation of any homeowners policy is coverage for your home’s physical structure. This includes protection against perils like fire, wind damage, and theft. The Insurance Information Institute reports that the average claim for fire and lightning damage in 2022 was $83,991 (a staggering amount that highlights the importance of adequate coverage for your home’s structure).

It’s essential to reassess your home’s value regularly to ensure your coverage keeps pace with rising construction costs. You should insure your home not for what you paid, but for what it would cost to rebuild today.

Safeguarding Your Personal Property

Your policy also covers your personal belongings (furniture, clothing, electronics, and other possessions). Most policies cover 50% to 70% of the insurance on your dwelling for personal property. However, high-value items like jewelry or art often require additional coverage.

A practical tip: create a home inventory. This detailed list of your possessions, complete with photos and receipts, can prove invaluable if you need to file a claim. Many insurance companies now offer apps to simplify this process.

Liability Protection: Your Safety Net

Liability coverage, often overlooked, is a critical component. It protects you if someone sustains an injury on your property or if you accidentally damage someone else’s property. The Insurance Information Institute recommends a minimum of $300,000 in liability coverage for adequate protection.

This coverage can save you in unexpected situations. For instance, if your dog bites a neighbor or a delivery person slips on your icy sidewalk, your liability coverage can help cover medical expenses and potential legal costs.

Additional Living Expenses: When Disaster Strikes

If a covered disaster renders your home uninhabitable, additional living expenses (ALE) coverage activates. This pays for hotel bills, restaurant meals, and other costs you incur while your home undergoes repairs or rebuilding.

ALE coverage typically amounts to about 20% of your dwelling coverage. However, some insurers offer higher limits. If you live in a disaster-prone area, you should consider increasing this coverage to avoid out-of-pocket expenses for extended periods.

As we move forward, it’s important to understand that while homeowners insurance provides comprehensive coverage, it’s not the only type of property insurance available. Let’s explore another essential form of coverage: renters insurance.

What Does Renters Insurance Cover?

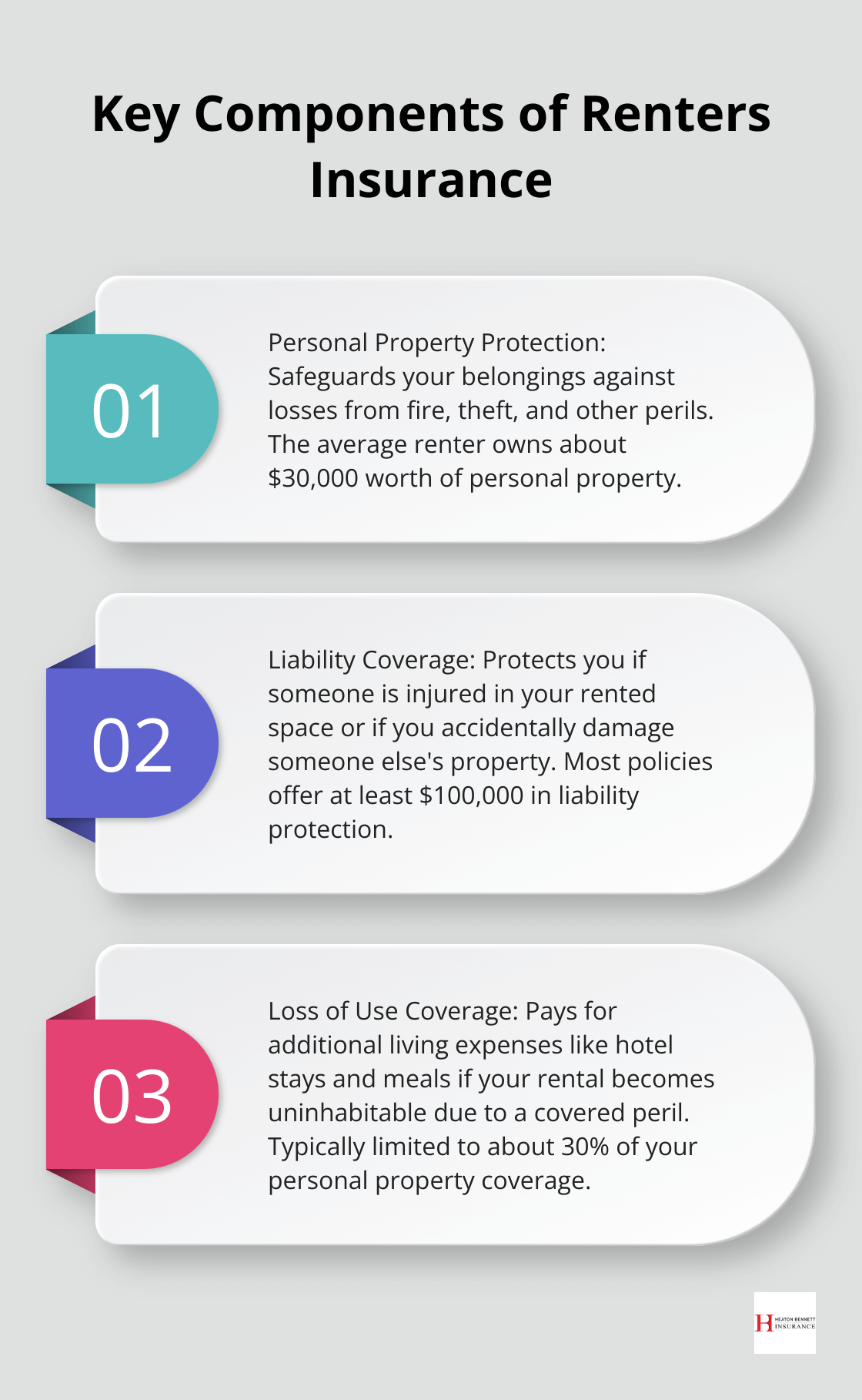

Personal Property Protection

Renters insurance primarily safeguards your belongings. While your landlord’s policy covers the building, it doesn’t extend to your personal items. A typical policy protects against losses from fire, theft, and other perils.

The Insurance Information Institute reports that the average renter owns about $30,000 worth of personal property. Many underestimate the value of their possessions. We recommend you create a detailed inventory of your belongings (including photos and approximate values). This not only helps you determine adequate coverage but also streamlines the claims process if needed.

Liability Coverage for Renters

Liability coverage is a key component of renters insurance that many overlook. This coverage protects you if someone injures themselves in your rented space or if you accidentally damage someone else’s property.

Most policies offer at least $100,000 in liability protection. We often recommend you increase this to $300,000 or more (especially if you frequently entertain guests or have pets). The cost difference is usually minimal for the added peace of mind.

Loss of Use Coverage

Loss of use coverage, also known as additional living expenses, addresses concerns when your apartment becomes uninhabitable due to a covered peril. This coverage typically pays for hotel stays, restaurant meals, and other necessary expenses while your rental undergoes repairs.

Most policies limit this to about 30% of your personal property coverage. For example, if you have $30,000 in personal property coverage, you’d have up to $9,000 for additional living expenses.

Customizing Your Coverage

Every renter’s situation is unique. Some valuable add-ons to consider include:

- Replacement cost coverage: This pays to replace your items at today’s prices, rather than their depreciated value.

- Scheduled personal property: For high-value items like jewelry or electronics that exceed standard policy limits.

- Water backup coverage: Protects against damage from sewer or drain backups, which standard policies often exclude.

- Identity theft protection: Offers support and coverage if you become a victim of identity theft.

The National Association of Insurance Commissioners reports that the average renters insurance premium in 2021 was $174 per year. This makes renters insurance an affordable way to protect yourself and your belongings.

As we shift our focus from personal to business property, it’s important to understand that commercial properties require a different type of coverage. Let’s explore the intricacies of commercial property insurance and how it protects businesses from potential risks.

How Commercial Property Insurance Protects Your Business

Commercial property insurance serves as a vital shield for businesses, safeguarding physical assets and financial stability. This coverage can make or break a company’s recovery after unexpected events.

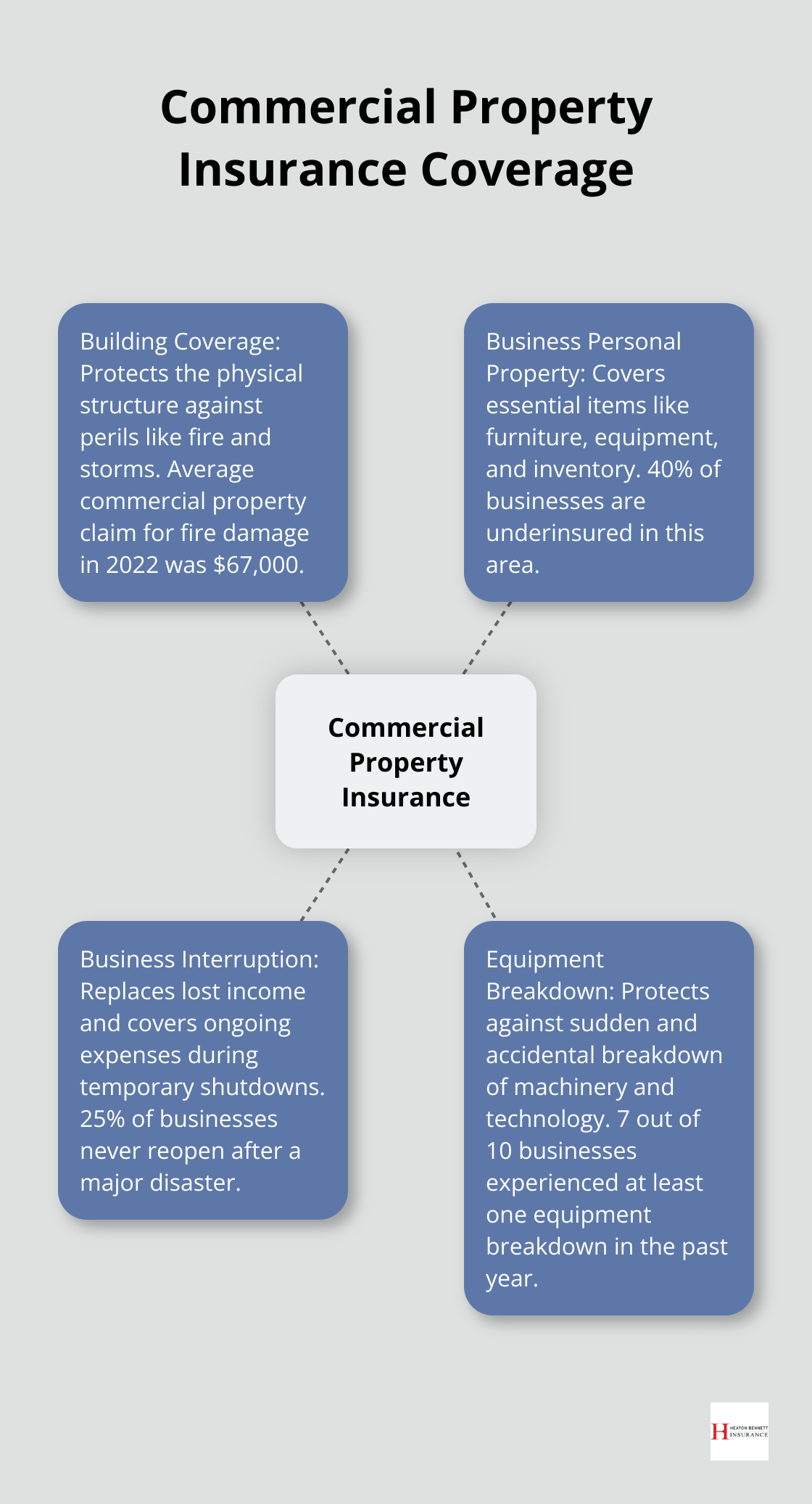

Building Coverage: The Foundation of Protection

Building coverage forms the cornerstone of commercial property insurance. It protects the physical structure of your business premises against perils like fire, storms, and vandalism. The Insurance Information Institute reports that the average commercial property claim for fire damage in 2022 was $67,000 (a figure that underscores the importance of adequate coverage).

When you determine building coverage, consider replacement cost rather than market value. Construction costs have risen significantly in recent years, so it’s important to reassess your coverage regularly. An annual review will help ensure your policy keeps pace with increasing building costs.

Business Personal Property Protection

Business personal property protection covers items essential to your operations, such as furniture, equipment, and inventory. A 2023 study by the National Association of Insurance Commissioners found that 40% of businesses are underinsured in this area, which risks significant out-of-pocket expenses if disaster strikes.

To avoid this pitfall, conduct a thorough inventory of your business assets annually. Include detailed descriptions, serial numbers, and purchase dates. This not only helps in determining adequate coverage but also speeds up the claims process if needed.

Business Interruption Insurance: A Financial Lifeline

Business interruption insurance often gets overlooked but can be a lifeline when disaster forces a temporary shutdown. This coverage helps replace lost income and covers ongoing expenses like rent and payroll during the recovery period.

The U.S. Small Business Administration reports that 25% of businesses never reopen after a major disaster. Business interruption insurance can be the difference between recovery and permanent closure. When you select this coverage, consider your business’s specific needs and potential downtime scenarios.

Equipment Breakdown Coverage

Equipment breakdown coverage is increasingly important in our technology-dependent business world. It protects against sudden and accidental breakdown of machinery, computers, and other vital equipment.

A 2022 Hartford Steam Boiler study revealed that 7 out of 10 businesses experienced at least one equipment breakdown in the past year, with an average cost of $35,000 per incident. This coverage isn’t just for manufacturing businesses; it’s essential for any company relying on equipment or technology.

Every business has unique risks and needs. A comprehensive commercial property insurance package should address your specific concerns. Working with an independent agency (like Heaton Bennett Insurance) allows you to leverage relationships with multiple carriers to find the best coverage at competitive rates, ensuring your business is well-protected without breaking the bank.

Final Thoughts

Property insurance coverage types protect your assets in various situations. Homeowners, renters, and business owners all need tailored solutions to address their unique risks. At Heaton Bennett Insurance, we offer customized insurance solutions to meet your specific needs and budget.

Independent agencies like ours provide access to multiple carriers, allowing us to compare options and find the best fit for you. Our team of experts guides you through the complex world of insurance, helping you understand different policies and coverage options. We use a “Security Snapshot” process to assess your individual needs and create a tailored insurance package.

We specialize in personal and business insurance, including niche types like motorcycle and vacant property coverage. Contact Heaton Bennett Insurance today to review your current coverage and explore how we can help safeguard your future with tailored insurance solutions. Don’t leave your assets vulnerable to unforeseen events.