Restaurant Business Policy: Protecting Your Dining Operation

Running a restaurant means managing countless moving parts, from food safety to customer interactions to kitchen operations. At Heaton Bennett Insurance, we know that one accident or incident can threaten your entire business. A solid restaurant business policy protects you against the specific risks that come with operating a dining establishment. This guide walks you through the coverage types you need and how to choose the right protection for your operation.

What Coverage Types Your Restaurant Actually Needs

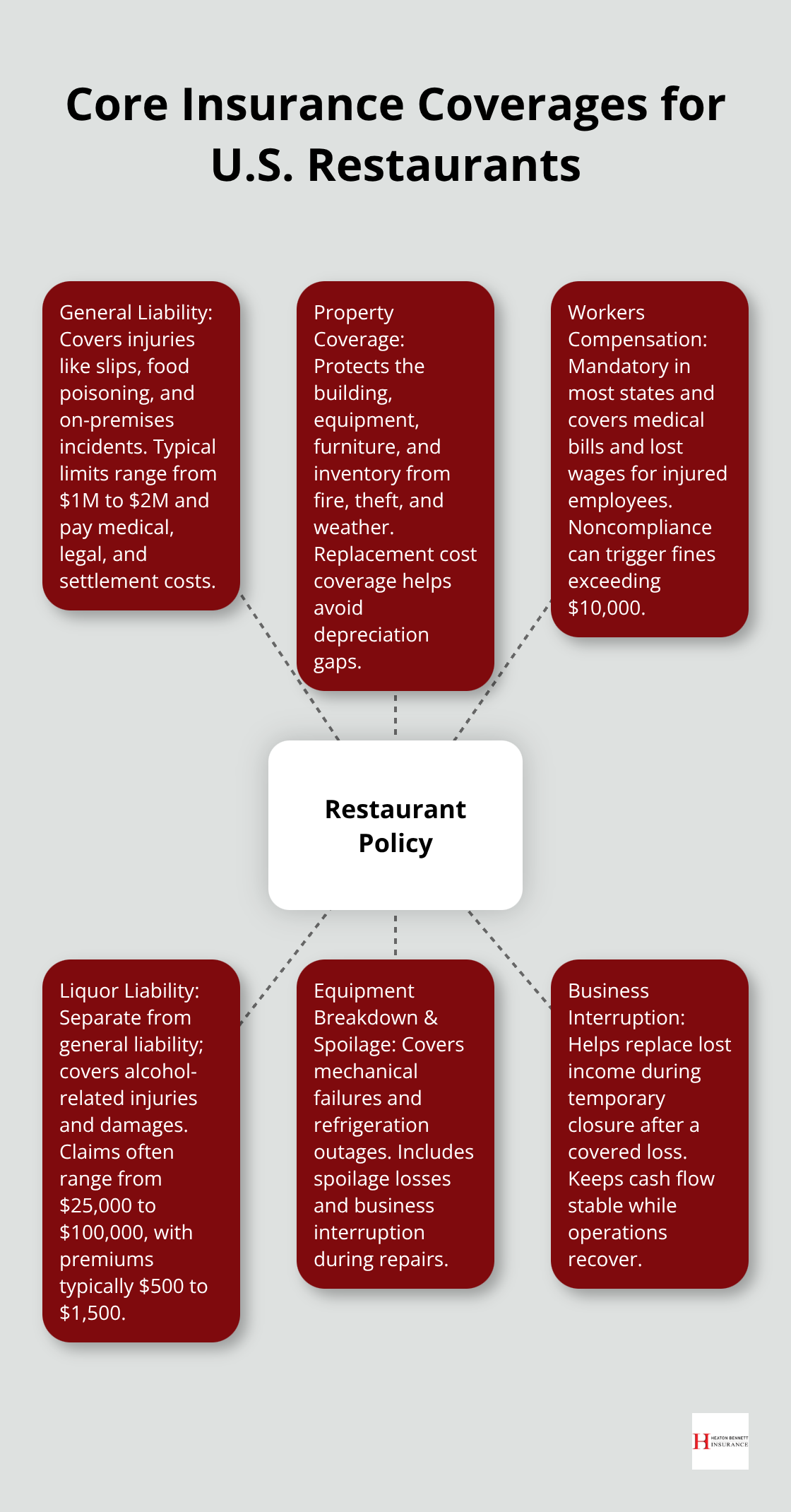

General liability coverage protects your restaurant when a customer slips on a wet floor, suffers food poisoning, or sustains an injury at your location. This coverage pays for medical expenses, legal fees, and settlements up to your policy limit. Most restaurants carry between $1 million and $2 million in general liability coverage. The cost varies based on your revenue, location, and claims history, but restaurants typically pay between $500 and $1,500 annually for basic coverage.

Property Coverage Shields Your Physical Assets

Property coverage protects your building, kitchen equipment, furniture, and inventory against fire, theft, weather damage, and other physical losses. A kitchen fire can cost $50,000 to $250,000 in equipment replacement and structural repairs, which makes property insurance non-negotiable. Your policy should cover replacement cost, not actual cash value, because depreciated equipment values won’t cover modern replacements. Without this protection, you absorb the full financial hit when disaster strikes.

Workers Compensation Covers Employee Injuries

Workers compensation insurance is mandatory in most states and covers medical bills and lost wages when an employee gets injured on the job. Restaurant kitchens have high injury rates-burns, cuts, and repetitive strain injuries occur regularly-and workers compensation protects both your employees and your business from liability. Most states require coverage if you have even one employee, and failing to carry it can result in fines exceeding $10,000. This coverage keeps your operation compliant and your team protected.

Kitchen Equipment Requires Specific Coverage Terms

Commercial kitchen equipment represents your largest asset and demands explicit coverage terms. Ovens, grills, fryers, and refrigeration units cost $30,000 to $100,000 to replace, and standard property policies sometimes exclude certain equipment or impose low limits. Your property policy should explicitly cover equipment breakdown, spoilage from refrigeration failure, and business interruption if equipment failure forces temporary closure. A walk-in freezer failure can destroy $5,000 to $15,000 in inventory, so ask your insurance provider whether your policy covers spoilage losses from such incidents.

Liquor Liability Protects Against Alcohol-Related Claims

If you serve alcohol, liquor liability insurance operates separately from general liability and covers injuries or damages caused by intoxicated guests. A customer who drinks at your bar and then causes a car accident can sue your restaurant under dram shop laws in most states. Liquor liability claims average $25,000 to $100,000, making this coverage essential if alcohol sales represent any portion of your revenue. The cost typically runs $500 to $1,500 annually depending on your alcohol volume and server training documentation. Understanding these coverage types positions you to make informed decisions about your specific operational needs.

Where Restaurant Accidents Actually Happen

Foodborne Illness Threatens Your Reputation and Revenue

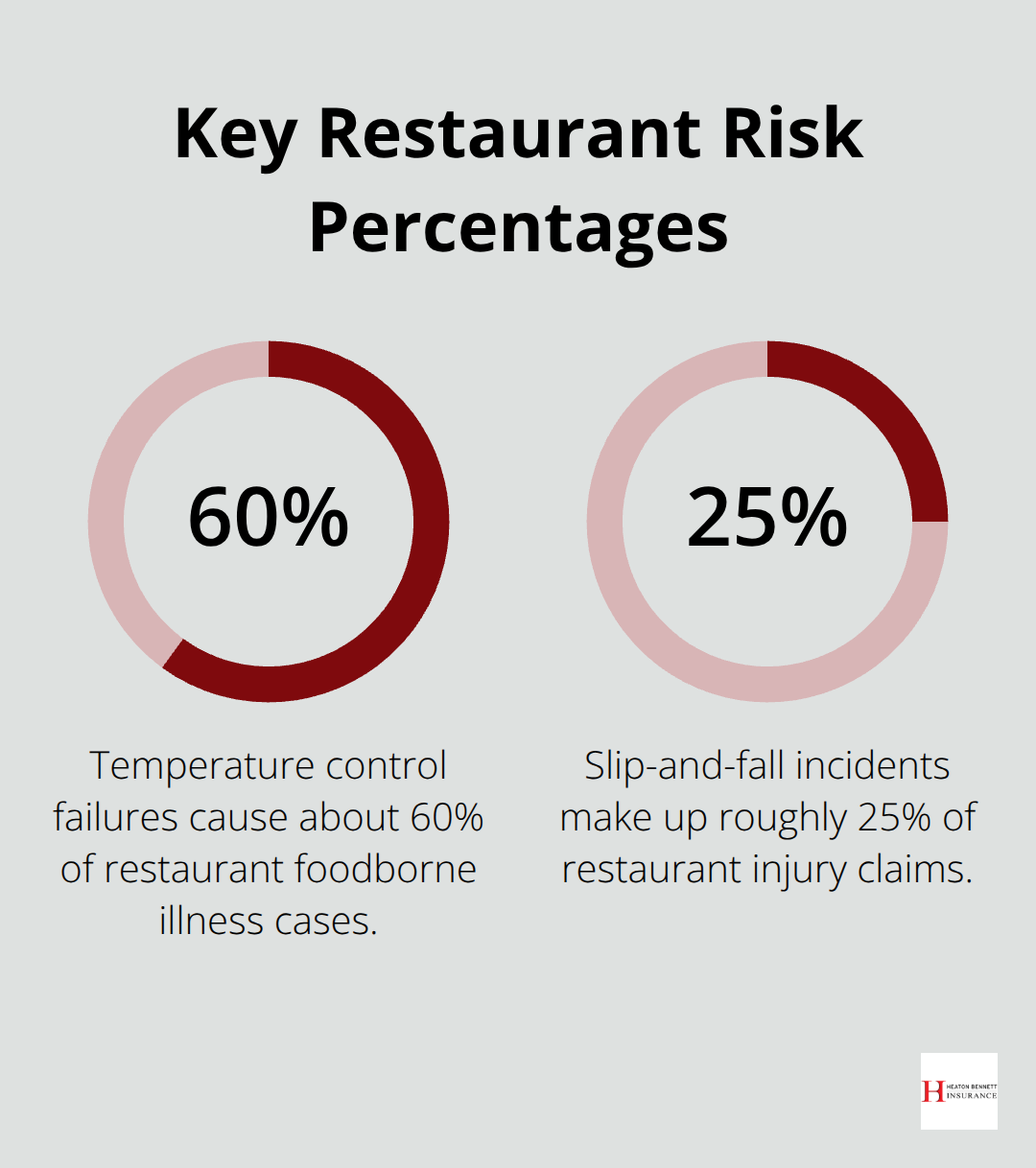

Foodborne illness claims cost restaurants an average of $25,000 to $75,000 in legal fees and settlements alone, before accounting for lost customers and reputation damage. The CDC links approximately 48 million foodborne illness cases annually in the United States to contaminated food, with restaurants responsible for a significant portion. One outbreak traced back to your kitchen spreads quickly on social media and destroys years of customer trust. Temperature control failures account for roughly 60% of foodborne illness cases in restaurants, making refrigeration monitoring non-negotiable.

Implement daily temperature logs with staff signatures for all cold storage units. Use color-coded cutting boards to prevent cross-contamination between raw proteins and vegetables, and designate separate prep areas for allergen-sensitive items. Laminated visual guides posted at each station reduce confusion during busy service. Quarterly food safety training keeps your team sharp on proper handling techniques.

Health Code Violations Create Cascading Costs

Health code violations follow foodborne illness as a major operational threat-a single violation from your local health department triggers fines between $500 and $5,000 per infraction, and repeated violations can force temporary closure. The real damage extends beyond fines: customers learn about violations through inspection reports and social media, and they take their business elsewhere. Your business liability insurance covers the financial fallout, but prevention stops the crisis before it starts.

Slip and Fall Accidents Generate the Highest Claims

Slip and fall accidents generate the highest number of general liability claims in restaurants-accounting for roughly 25% of all restaurant injury claims according to industry data. A customer who falls on a wet floor and fractures their hip can claim $50,000 to $150,000 in medical expenses and pain-and-suffering damages. Your kitchen floor presents even greater risk: grease accumulation, water spills, and food debris create hazardous conditions that injure staff regularly.

Non-slip flooring in kitchens and high-traffic dining areas costs $3,000 to $8,000 to install but eliminates a major liability source. Absorbent mats positioned at entry points and bar stations reduce moisture on walking surfaces. Immediate cleanup protocols for spills prevent accidents before they happen. Require slip-resistant shoes for all kitchen staff and enforce the rule consistently.

Kitchen Equipment Fires Destroy Assets and Operations

Kitchen equipment fires destroy equipment valued at $50,000 to $250,000 and can force weeks of closure while repairs happen. Fryer fires alone account for roughly 5,000 residential and commercial fires annually in the United States, making routine equipment maintenance absolutely critical. Schedule quarterly professional inspections of all cooking equipment and clean hood systems monthly to remove grease buildup. Train staff on fire suppression techniques specific to each equipment type. Your property insurance covers replacement costs, but the business interruption from closure often exceeds the equipment damage itself.

These accident categories represent your highest-risk exposure areas, and understanding them shapes how you structure your insurance coverage and operational safeguards. The next section examines how to assess your specific risks and select the right policy limits for your restaurant’s unique profile.

Sizing Your Coverage to Match Your Restaurant’s Reality

Your restaurant’s revenue, location, kitchen size, and service model determine which coverage limits actually protect you versus which ones waste your premium dollars. A 40-seat casual dining spot in a suburban strip mall faces different risks than a 150-seat fine-dining establishment downtown with a full bar and late-night service. Start by documenting your annual revenue, employee count, alcohol sales percentage, and equipment inventory value. This data becomes your baseline for conversations with insurance providers.

Match General Liability Limits to Your Operation Size

General liability limits of $1 million work for smaller operations, but restaurants with $2 million-plus annual revenue and high-traffic locations should carry $2 million minimum. If you serve alcohol, add liquor liability coverage matching your general liability limit rather than settling for the minimum $100,000 some carriers offer. Your location and customer volume directly influence the risk exposure that your policy limits must cover.

Account for Your Actual Replacement Costs

Property coverage must account for the full replacement value of everything inside your restaurant, not estimates from five years ago. Kitchen equipment depreciates slowly, so a fryer worth $8,000 new still costs $7,500 to replace today. Request a detailed inventory walkthrough with your insurance agent and photograph expensive items for documentation. This step prevents underinsurance when you file a claim.

Control Workers Compensation Through Loss Prevention

Workers compensation rates depend on your payroll and claims history, but you cannot negotiate coverage limits-the state mandates minimums. What you can control is loss prevention through training programs and safety protocols that reduce injury claims and lower your premiums over time. Documented safety initiatives directly impact your long-term costs.

Compare Policies Beyond Premium Price

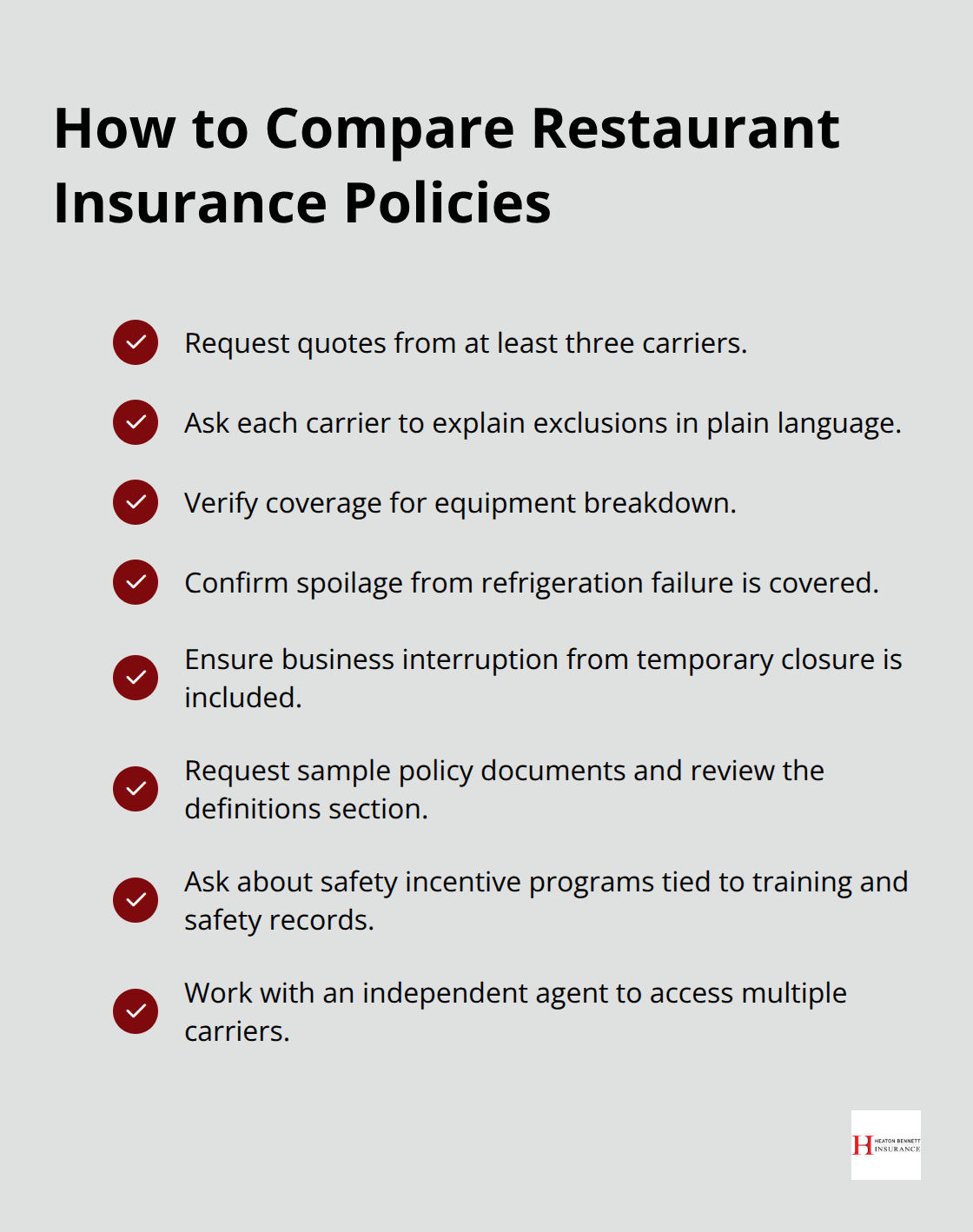

Comparing policies requires looking beyond premium price because cheap coverage with $250,000 property limits leaves you exposed when a kitchen fire hits. Request quotes from at least three carriers and ask each one to explain exclusions in plain language. Many restaurants miss critical gaps because they assume standard policies cover everything. Some carriers exclude flood damage unless you purchase separate coverage, exclude certain equipment types, or impose caps on spoilage losses.

Ask specifically whether your policy covers equipment breakdown, spoilage from refrigeration failure, and business interruption from temporary closure. Request sample policy documents and review the definitions section-terms like “direct physical loss” or “sudden and accidental” determine whether claims get paid. Industry data shows restaurants with documented safety programs and regular training receive 10-15% premium discounts, so ask carriers whether they offer safety incentive programs. An independent insurance agent can access multiple carriers and help you identify coverage gaps that matter for your specific operation.

Final Thoughts

Your restaurant’s survival depends on protecting against the specific risks that threaten your operation daily. General liability, property coverage, workers compensation, and liquor liability form the foundation of a solid restaurant business policy that keeps you compliant and financially secure when accidents happen. The cost of these coverages pales against the $50,000 to $250,000 that kitchen fires can destroy or the $25,000 to $75,000 that foodborne illness claims can cost.

Evaluating your coverage starts with honest assessment of your actual risks and the data that defines your operation. Document your annual revenue, employee count, equipment inventory, and alcohol sales percentage, then use this information to determine whether $1 million or $2 million in general liability limits fits your restaurant. Request detailed quotes from multiple carriers and ask each one to explain exclusions in plain language rather than accepting the cheapest option, and review sample policies to confirm that equipment breakdown, spoilage losses, and business interruption protection are explicitly included.

At Heaton Bennett Insurance, we understand that restaurant owners need coverage tailored to their specific operational challenges. Our team accesses multiple carriers to find protection that matches your actual risks rather than forcing you into one-size-fits-all policies, and we guide you through the coverage decisions that matter for your dining operation. Contact us to discuss your restaurant’s unique risk profile and build a comprehensive policy that lets you focus on running your business instead of worrying about what happens when disaster strikes.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.