How to Get General Liability Insurance for Cleaning Business

One slip on a wet floor. One broken vase at a client’s home. One accident on the job site-and your cleaning business could face a lawsuit that wipes out your savings.

General liability insurance for cleaning businesses isn’t optional anymore. Most clients won’t hire you without it, and the financial risk of operating without coverage is simply too high. Here at Heaton Bennett Insurance, we’ve seen too many cleaning business owners learn this lesson the hard way.

This guide walks you through exactly what coverage you need and how to get it.

Why You Actually Need General Liability Insurance

A broken window at a client’s home costs $500 to replace. Your cleaning crew caused it while washing exterior glass. Without general liability insurance, you pay that $500 from your business account. Now multiply that by a slip-and-fall injury where a client’s medical bills reach $15,000, or a scenario where your equipment damages expensive flooring during a commercial job. These aren’t hypothetical situations-they happen to cleaning businesses regularly, and they destroy companies that lack proper coverage. According to Insureon data, general liability insurance for cleaning businesses averages just $48 per month, yet the average claim could easily exceed your annual premium by thousands of dollars. The math is simple: skipping this coverage isn’t saving money, it’s gambling with your business survival.

Property damage claims hit harder than you think

Cleaning businesses operate in client spaces filled with valuables. You work around furniture, artwork, hardwood floors, and personal belongings. One aggressive pressure washing session can strip paint from siding. One chemical mixture can bleach carpet. One misplaced equipment can crack tile or dent walls. These aren’t rare events-they’re part of the job risk. General liability coverage protects you when accidental damage occurs during your work, covering repair or replacement costs plus legal fees if the client sues. Without it, you remain personally liable for the full amount. Most cleaning business owners operate with minimal cash reserves, meaning a single property damage claim can force you to shut down temporarily or permanently. The coverage exists specifically because these incidents are predictable hazards in your industry, not freak accidents.

Client injuries create immediate legal exposure

A client slips on a wet floor you just mopped. They break their wrist and require surgery costing $20,000. They hire an attorney. Now you face a lawsuit regardless of whether you were actually negligent. General liability insurance covers medical expenses, legal defense costs, and settlement amounts up to your policy limits. According to data from the insurance industry, bodily injury claims from slip-and-fall incidents rank among the most common liability claims against service businesses. Without coverage, you pay an attorney out of pocket to defend yourself, even if you ultimately win the case. Court costs alone can reach $5,000 to $10,000. Most cleaning businesses can’t absorb those expenses while continuing operations. Additionally, many commercial clients require proof of coverage before they allow you on their property, meaning no insurance often means no high-value contracts.

Clients won’t hire you without it

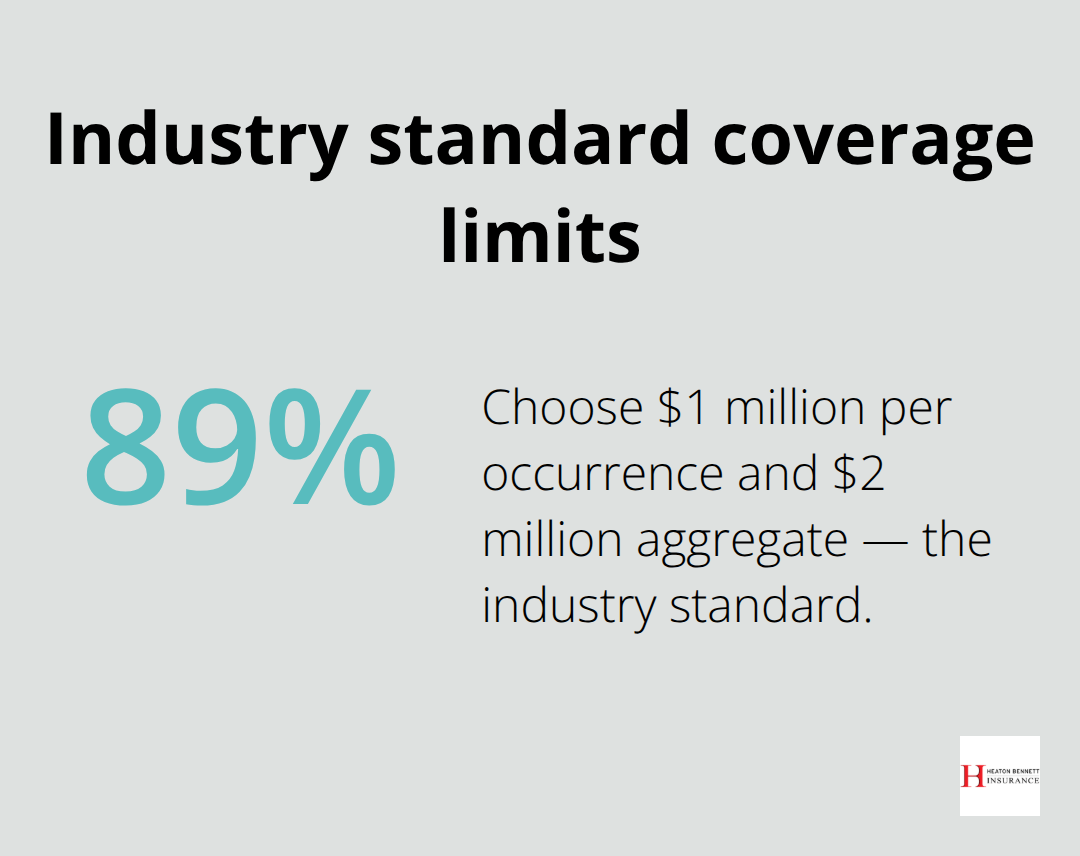

This isn’t speculation-it’s standard business practice. Commercial facilities, property management companies, and even many residential clients now request certificates of insurance before signing contracts. Insureon data shows that 89% of cleaning businesses purchase general liability insurance with $1 million per occurrence and $2 million aggregate limits, indicating this has become the industry standard.

When a potential client asks for your certificate of insurance and you don’t have one, you’ve lost that job. You can’t compete with other cleaning companies that carry coverage. Building a cleaning business means taking on larger commercial contracts as you grow, and those contracts almost always require proof of liability coverage. The businesses you want to work with-property management companies, corporate offices, multi-unit residential buildings-won’t even review your proposal without it. This isn’t just about protecting yourself from financial ruin; it’s about accessing the market opportunities that actually pay well.

Understanding what coverage you need is one thing. Actually obtaining it requires knowing which types of policies protect your business and which ones are optional versus mandatory.

What Coverage Protects Your Cleaning Business

General liability insurance forms your foundation, but it’s not your only protection. Many cleaning business owners assume general liability covers everything, then face denied claims because they lacked the right additional policies.

The reality is that different coverage types protect against different risks, and mixing them up costs you money or leaves you exposed.

General Liability Covers Third-Party Claims

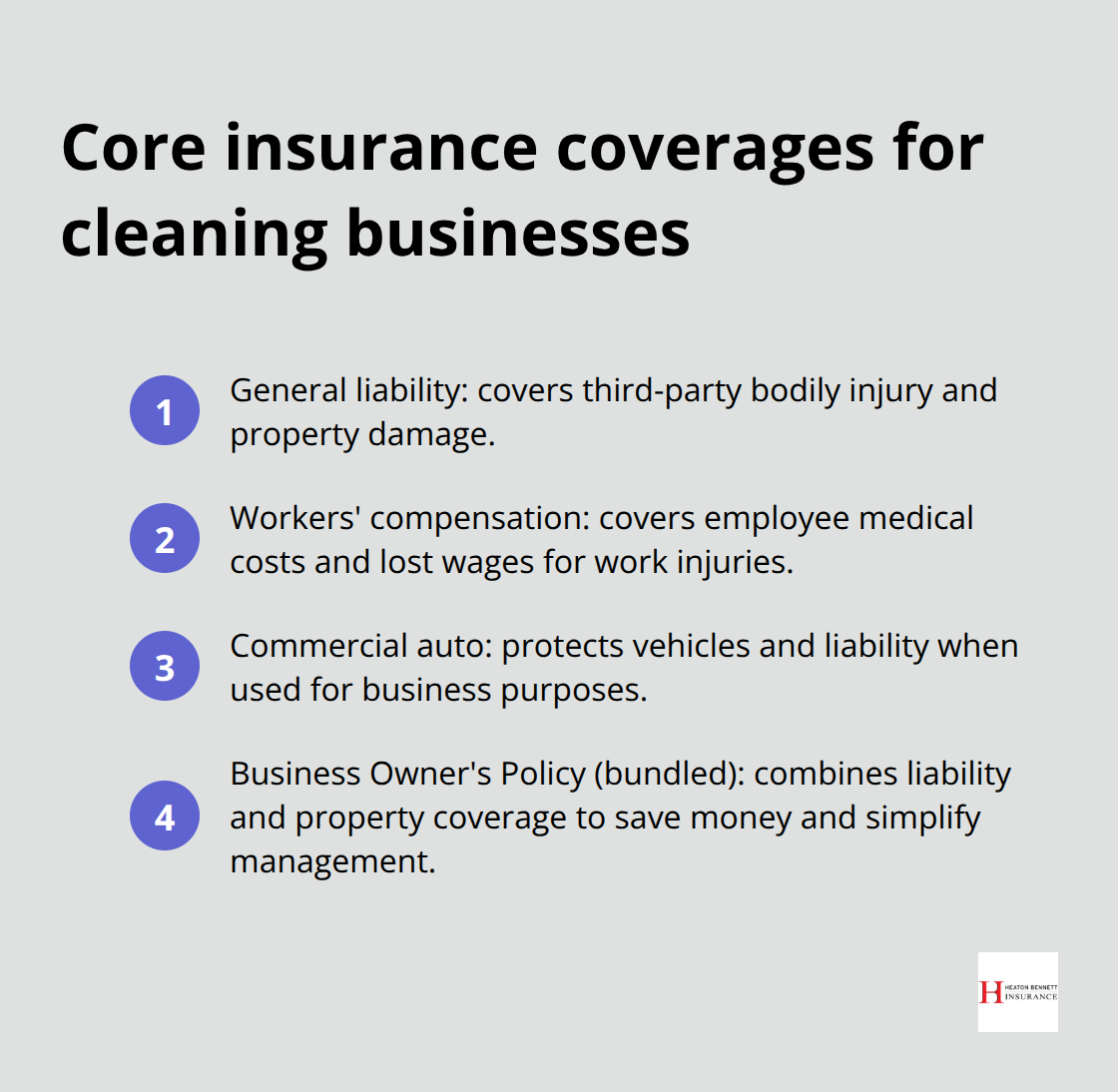

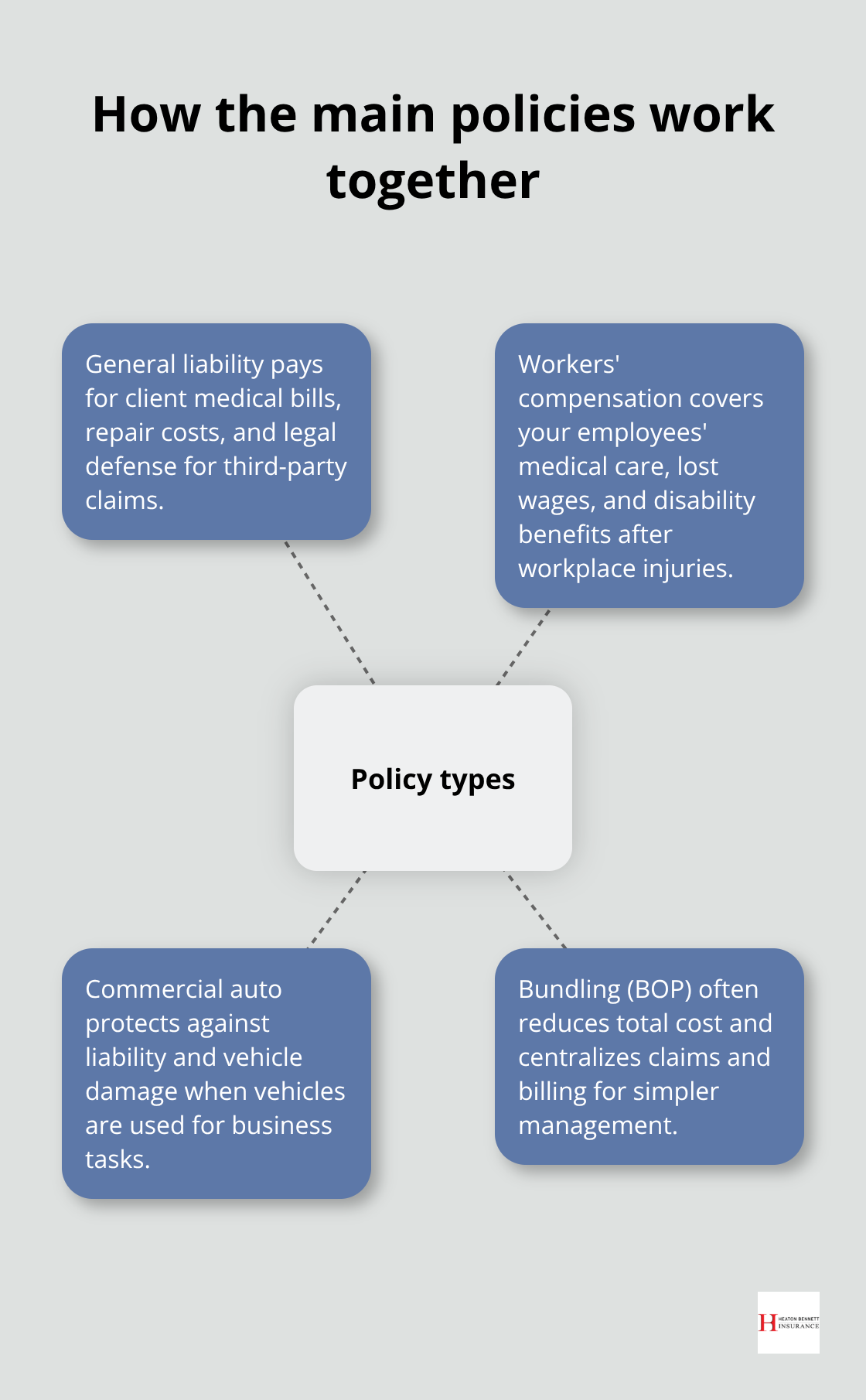

General liability specifically protects you against third-party bodily injury and property damage-meaning injuries or damage that happen to clients or their property, not your employees or your own equipment. When a client slips on a freshly mopped floor or you accidentally damage their hardwood while stripping wax, general liability pays for medical bills, repairs, and legal defense. This coverage addresses the most common risks you face in daily operations. However, general liability won’t cover your employees if they get injured on the job. That’s where workers’ compensation enters the picture.

Workers’ Compensation Protects Your Team

Workers’ compensation is legally required in 49 of 50 states if you have employees, and it covers medical expenses, lost wages, and disability benefits for work-related injuries. According to Insureon data, workers’ compensation for cleaning businesses averages $136 per month, with 67% of cleaning businesses with employees paying less than $200 monthly. The cost depends on your payroll, the number of employees, and your state’s rates. This coverage protects your team and shields you from personal liability when an employee gets hurt performing their job duties.

Commercial Auto Insurance Protects Your Vehicles

If you operate vehicles for your business-whether company-owned vans for transporting supplies or personal cars you use to travel between job sites-commercial auto insurance is mandatory in most states. Personal auto insurance explicitly excludes business use, meaning you remain uninsured if you get into an accident while driving to a client’s home. Commercial auto insurance averages $173 per month according to Insureon, and it protects you against liability claims and vehicle damage when you use vehicles for work purposes.

Bundling Coverage Saves Money and Simplifies Management

These three coverage types work together to create a complete protection strategy. General liability handles third-party claims, workers’ compensation covers your team, and commercial auto protects your vehicles and the people in them.

Bundling general liability with commercial property coverage into a Business Owner’s Policy costs approximately $76 per month according to Insureon data, which is often cheaper than buying them separately. Many cleaning businesses start with general liability and workers’ compensation, then add commercial auto once they have company vehicles or regularly drive personal vehicles to client locations.

Match Your Coverage to Your Operations

The key is matching your coverage to your actual operations. A solo cleaner working from home needs different coverage than a five-person team with service vehicles. A pressure washing operation carries different risks than residential house cleaning. Commercial clients like property management companies or corporate offices often specify minimum coverage requirements in their contracts-typically $1 million per occurrence and $2 million aggregate for general liability. Knowing these industry standards before you request quotes helps you compare apples to apples and ensures you can meet client demands without overpaying for excessive coverage limits. Understanding what you need is only half the battle; the next step involves actually gathering the information insurers require to provide accurate quotes.

Getting Your General Liability Quote in Three Steps

Compile Your Business Details First

Obtaining general liability insurance requires you to submit accurate business information to insurers so they can calculate your premium. Start by compiling your business details: your cleaning service type (residential house cleaning, pressure washing, commercial janitorial, carpet cleaning, or a combination), the number of employees you currently have or plan to hire, your annual revenue or projected revenue, your location, and whether you own or lease business vehicles. Insurers use these specifics to assess your risk profile. A solo residential house cleaner presents different risk than a five-person team performing commercial floor waxing at multiple locations daily.

According to Insureon data, general liability premiums vary significantly by service type-pressure washing averages around $75 per month while house cleaning averages $44 per month. This variation exists because pressure washing carries higher property damage risk than basic house cleaning. When you request quotes, insurers will ask about your claims history, any previous incidents, and the specific equipment you use. Have this information ready before contacting providers; vague answers delay quotes and often result in higher estimates since insurers assume worst-case scenarios when details are missing.

Request Quotes from Multiple Carriers

Comparing quotes from multiple carriers is non-negotiable because premium differences between insurers for identical coverage can exceed 50 percent. Request quotes from at least three providers and ensure each quote specifies the same coverage limits-typically $1 million per occurrence and $2 million aggregate, which Insureon data shows 89 percent of cleaning businesses select. Don’t assume the lowest quote is your best option; examine what each policy actually covers, the deductible amounts, and any exclusions specific to your service type.

Some insurers exclude certain cleaning methods or won’t cover high-risk services like biohazard cleanup. Work with an independent agent who represents multiple carriers rather than captive agents tied to single insurers. Independent agents can access multiple carriers and help you understand coverage differences so you select appropriate limits for your client base. If you regularly work with commercial clients requiring $2 million per occurrence limits, paying extra for that coverage makes sense; if you primarily service residential clients, standard limits may suffice.

Obtain Your Certificate of Insurance Immediately

Request your certificate of insurance immediately after purchasing-most insurers generate these within 24 hours, allowing you to share proof of coverage with clients right away and start bidding on contracts that require insurance documentation. This document demonstrates to potential clients that you carry legitimate protection, which accelerates your ability to win new business and meet contractual requirements.

Final Thoughts

General liability insurance for cleaning business operations protects you from the financial devastation that follows a single property damage claim or client injury. A broken window, a slip-and-fall accident, or damaged flooring can cost thousands in repairs and medical bills-expenses that force most uninsured cleaning businesses to shut down permanently. At just $48 per month on average, this coverage costs far less than the financial ruin you face without it.

Your coverage needs match your business structure and client base. A solo residential cleaner requires different protection than a five-person team handling commercial contracts, and commercial clients almost always demand proof of coverage before signing agreements. The industry standard of $1 million per occurrence and $2 million aggregate limits (which 89 percent of cleaning businesses carry) gives you a benchmark for comparing quotes and meeting client requirements without overpaying for unnecessary limits.

The process takes minimal time when you prepare properly. Compile your business details, request quotes from multiple carriers, and most insurers generate your certificate of insurance within 24 hours. Contact Heaton Bennett Insurance today to discuss your general liability insurance needs and receive a personalized quote tailored to your cleaning business.