How to Choose Dental Insurance for Small Businesses?

Small business owners face mounting pressure to attract and retain quality employees in today’s competitive job market. Dental insurance for small business has become a key differentiator that can make or break hiring decisions.

At Heaton Bennett Insurance, we see firsthand how the right dental coverage transforms employee satisfaction while managing costs effectively. The challenge lies in navigating dozens of plan options without overspending or under-delivering on benefits.

Which Dental Plan Type Works Best for Small Businesses

Small businesses have three main dental insurance options, and the choice dramatically impacts both costs and employee satisfaction. Preferred Provider Organization plans offer the most flexibility and allow employees to visit any dentist while they provide maximum savings with in-network providers. The National Association of Dental Plans reports that PPO plans dominate the market because they balance choice with cost control effectively. Health Maintenance Organization plans require employees to select a primary dentist from a restricted network and deliver premiums that run 40-60% lower than PPO options but limit provider choice significantly. Indemnity plans provide unlimited dentist selection but come with the highest premiums and complex reimbursement processes that frustrate both employers and employees.

Coverage Structures That Actually Matter

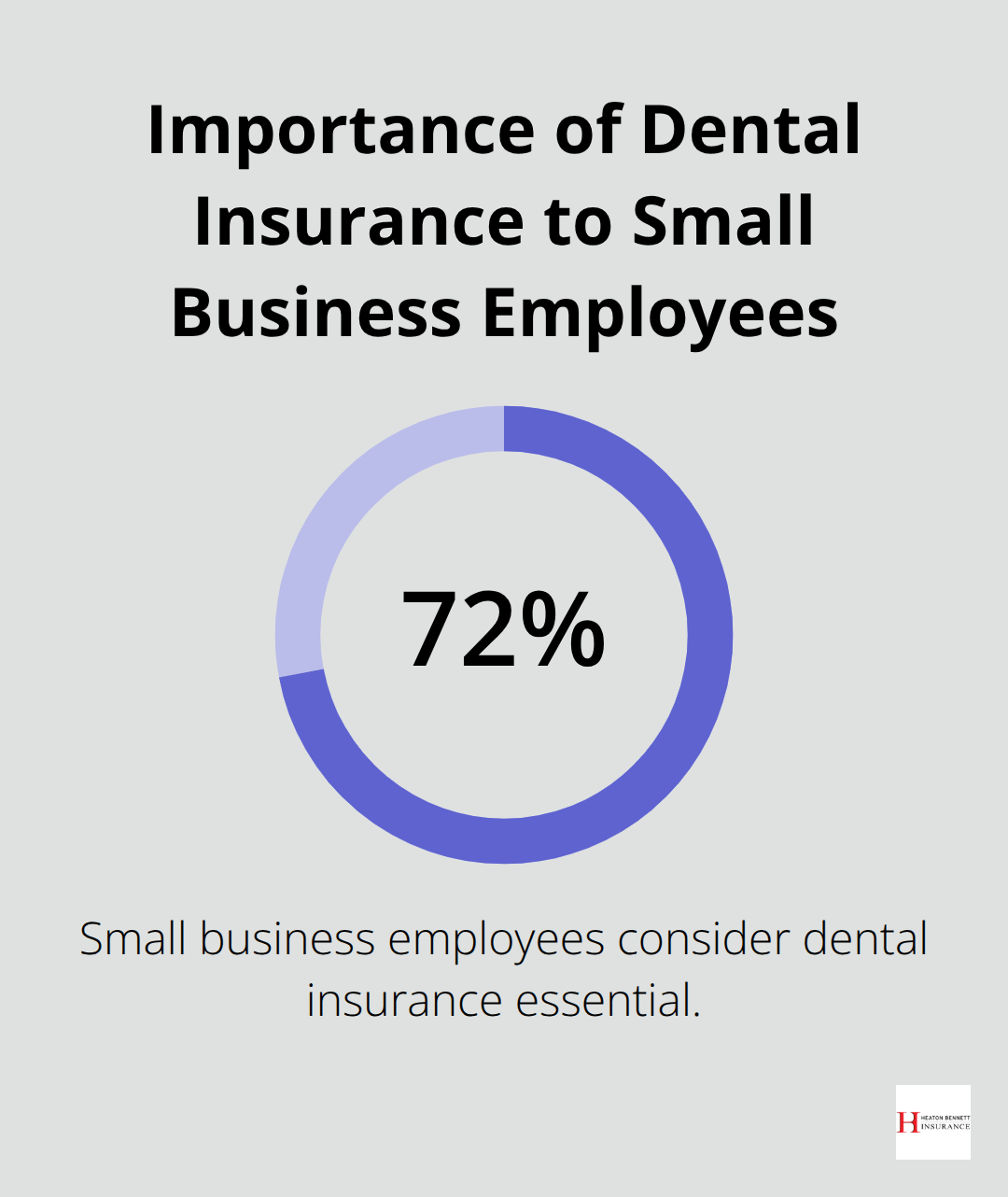

Most dental plans follow a standard coverage structure: preventive care at 100%, basic procedures like fillings at 80%, and major work such as crowns at 50%. Annual maximums typically range from $1,000 to $2,500 per employee, with MetLife’s Employee Benefit Trends Study showing that 72% of small business employees consider dental insurance essential. Smart employers focus on plans with robust preventive coverage since the American Dental Association reports that individuals with dental coverage visit dentists twice as often as those without coverage.

Coverage waiting periods vary significantly, with some plans that offer immediate preventive care while others impose 6-12 month delays for major procedures.

Network Decisions Drive Real Costs

Network strength determines actual employee costs more than premium prices do. Plans with extensive local networks reduce out-of-pocket expenses by 30-50% compared to limited networks. Verify that preferred local dentists participate in the network before you sign contracts, as network directories often contain outdated information. Out-of-network benefits typically reimburse at lower rates and require employees to pay providers directly before they seek reimbursement (which creates cash flow challenges that reduce plan satisfaction).

Premium Costs and Budget Reality

Small businesses typically pay between $8.94 to $13.90 monthly for group dental insurance per employee. Employers commonly cover 50-100% of employee-only premiums while employees pay for dependent coverage through payroll deductions. The average dental insurance premium reaches around $360 per year per employee according to the National Association of Dental Plans. These costs become tax-deductible business expenses that provide immediate financial advantages for small businesses.

Once you understand these fundamental plan structures and costs, the next step involves evaluating specific factors that will determine which option aligns best with your business goals and employee needs.

What Factors Actually Drive Your Dental Plan Decision

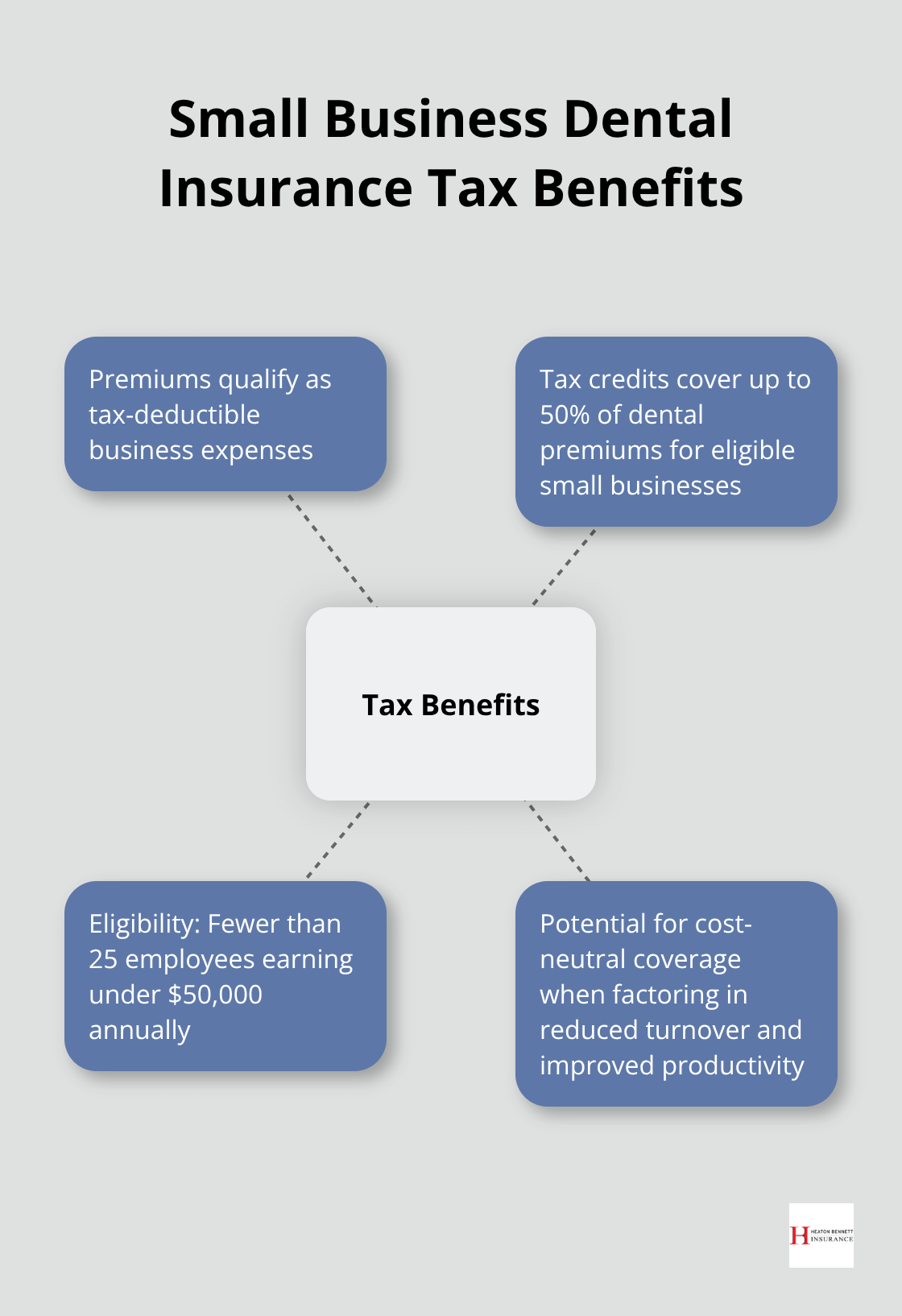

Budget realities demand brutal honesty about what your business can afford versus what employees expect. Small businesses with fewer than 25 employees who earn under $50,000 annually qualify for tax credits that cover up to 50% of dental premiums, which makes coverage significantly more affordable than most owners realize. The Harvard Business Review found that over 80% of employees prefer better benefits over pay raises, which means you invest $200-400 annually per employee in dental coverage and often deliver better retention results than equivalent salary increases.

Calculate total costs and include administrative time, as complex plans that require pre-authorizations and manual claims processing can consume 2-3 hours monthly of HR resources.

Employee Demographics Shape Plan Selection

Age and family status of your workforce determines which coverage elements matter most. Businesses with younger employees should prioritize orthodontic coverage since 25% of orthodontic patients are adults, while companies with older workers benefit from enhanced coverage for crowns and periodontal treatment. The National Institute of Dental and Craniofacial Research reports that adults lose over 164 million work hours annually due to dental diseases, which makes preventive coverage non-negotiable regardless of demographics. Survey employees directly about their current dental needs and preferred providers before you select plans, as assumptions about employee preferences prove wrong 60% of the time (according to LIMRA research).

Customization Options That Actually Matter

Voluntary dental benefits allow employees to purchase additional coverage through payroll deductions without employer contributions, which gives budget-conscious businesses flexibility while they meet diverse employee needs. Plans that offer multiple coverage tiers let employees choose between basic preventive-only options and comprehensive coverage that includes major procedures. Dual-choice strategies work exceptionally well, with companies that offer both HMO and PPO options and see 15-20% higher employee satisfaction rates than single-plan approaches. Administrative platforms that integrate with existing payroll systems reduce implementation headaches and ongoing management costs significantly.

Tax Benefits and Financial Advantages

Small businesses gain immediate tax advantages when they provide dental coverage as premiums qualify as tax-deductible business expenses. Companies with fewer than 25 full-time employees who earn less than $50,000 annually may qualify for additional tax credits that cover dental premiums (making the actual cost substantially lower than advertised rates). These financial incentives often make dental coverage cost-neutral when you factor in reduced turnover expenses and improved employee productivity.

With these key factors clearly defined, you need to evaluate specific providers and compare their offerings to find the plan that delivers the best value for your unique business situation.

How Do You Compare Dental Insurance Providers Effectively

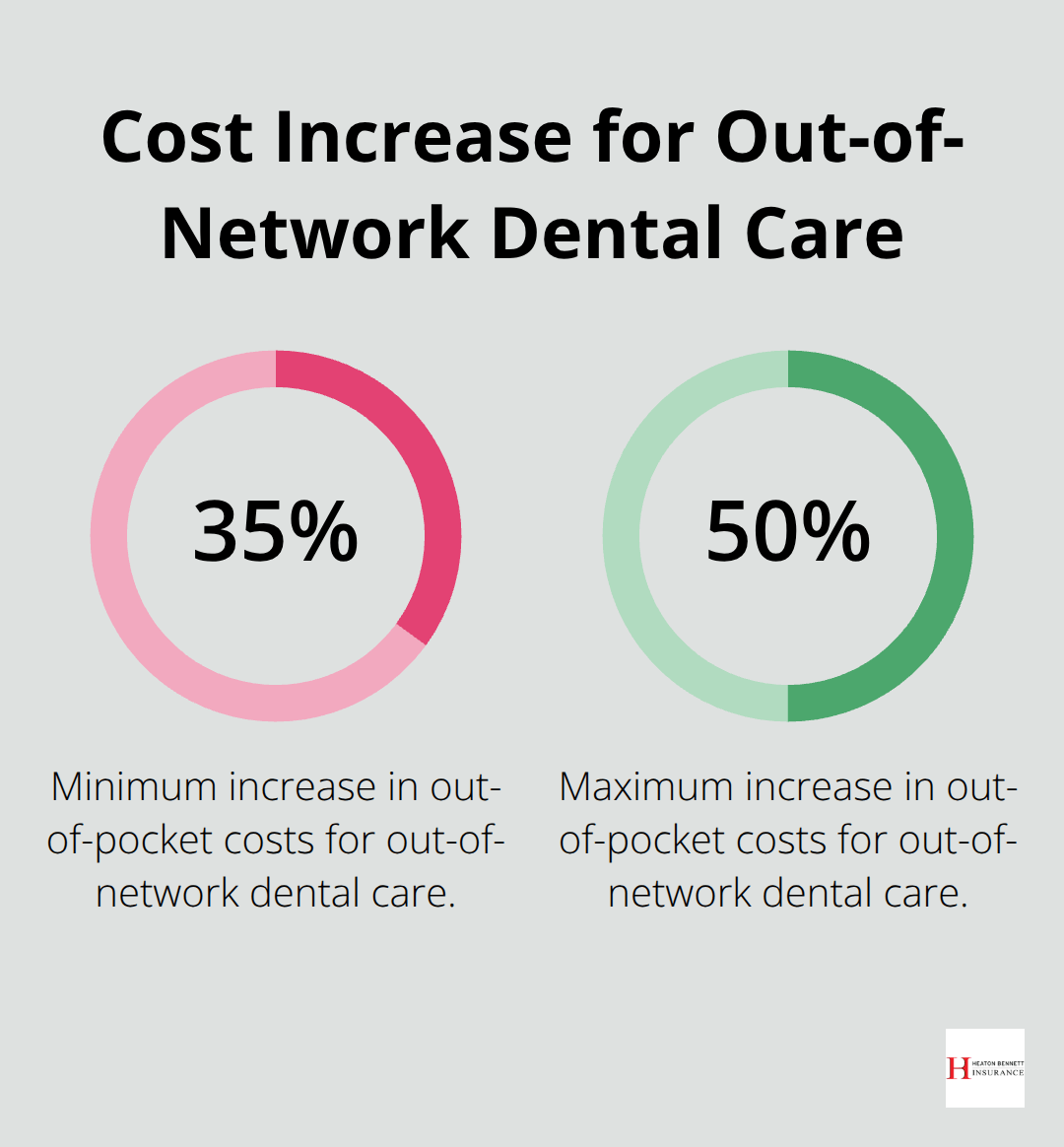

Provider network strength determines whether employees actually save money or face surprise bills at every dental visit. Delta Dental maintains the largest network with over 156,000 dentists nationwide, while regional carriers often provide better rates but limit provider choices to specific geographic areas. Request current provider directories directly from insurance companies rather than trust online searches, as network lists change monthly and outdated information leads to coverage disputes. Call three to five dental offices your employees currently visit to verify participation status and confirm whether they accept new patients under specific plans. The National Association of Dental Plans reports that employees who use out-of-network providers pay 35-50% more in out-of-pocket costs, which transforms affordable premiums into expensive reality.

Coverage Exclusions That Destroy Budgets

Standard exclusions include cosmetic procedures, implants, and pre-existing conditions, but hidden limitations cause the most financial damage. Many plans exclude coverage for procedures that start before the effective date, even if treatment continues for months after enrollment begins. Wait periods vary dramatically between providers, with some plans that cover cleanings immediately while others impose 12-month delays for major procedures like root canals and crowns. Maximum annual benefits cap at $1,000-$2,500 per person, but lifetime orthodontic maximums often reach only $1,500 for adults compared to $2,000 for children under most plans. Missing tooth clauses exclude coverage for teeth lost before enrollment (which affects 25% of adults over 35 according to American Dental Association data). Request detailed benefit summaries that specify exact wait periods, annual maximums, and exclusion lists before you make final decisions.

Deductible Structures That Actually Work

Family deductibles operate differently across providers and dramatically impact total costs. Some plans require each family member to meet individual deductibles before coverage begins, while others apply family maximums that activate after two or three members reach their limits. PPO plans typically impose $50-$100 individual deductibles for basic and major services, while HMO plans often eliminate deductibles entirely but restrict provider choices. Coinsurance percentages remain consistent at 80% for basic procedures and 50% for major work, but reimbursement calculations vary between usual and customary rates versus contracted fee schedules. Plans that use contracted fee schedules provide predictable costs, while usual and customary rate plans create variable expenses that employees cannot budget accurately.

Claims Processing Speed and Efficiency

Electronic claims submission reduces payment delays from 4-6 weeks to 7-10 business days for most procedures. Providers with integrated digital platforms allow dentists to verify benefits instantly and submit pre-treatment estimates that prevent surprise costs. Some carriers still require paper forms and manual processing (which creates frustration for both employees and dental offices). Check whether providers offer mobile apps that let employees track claims status and view benefit usage in real-time. Administrative burden varies significantly, with some plans that require pre-authorization for basic procedures while others streamline approval processes through automated systems. Request quotes from at least five carriers to generate maximum savings and compare processing efficiency across multiple providers.

Final Thoughts

Small businesses must balance network strength, coverage structure, and total costs when they select dental insurance. PPO plans provide flexibility while HMO options cut premiums by 40-60%. Verify that employees’ preferred dentists participate in the network before you sign any contracts.

Start implementation with employee surveys and request quotes from five carriers. Compare annual maximums, wait periods, and exclusion lists with precision. Electronic claims processing cuts payment delays from weeks to days and boosts employee satisfaction dramatically.

Companies with dental insurance small business coverage report 67% fewer sick days related to oral health issues (while employees with coverage visit dentists twice as often for preventive care). Tax deductible premiums and potential credits for qualifying small businesses create financial advantages. We at Heaton Bennett Insurance help Austin businesses navigate these complex decisions and provide access to multiple carriers that match your workforce needs with effective dental insurance solutions.

![Annuities Explained The Ultimate Guide for Retirees [2025]](https://insureaustin.com/wp-content/uploads/emplibot/Annuities-Explained-The-Ultimate-Guide-for-Retirees-_2025__1760663225-80x80.jpeg)